Is This Really the Best Telecom Stock?

There may be stormy weather ahead for the market. A long weekend didn't give investors much of a vacation, as ADP's employment numbers on Thursday presaged a worse report from the Bureau of Labor Statistics. In wobbly times like these, it becomes even more important to do some homework on the companies you own or have your eye on. Those that can outperform in the future often leave a trail of positive signals in the past. With that in mind, let's take a look at New Zealand Telecom (NYS: NZT) to find out if it fits the bill for future success.

Breaking down the numbers

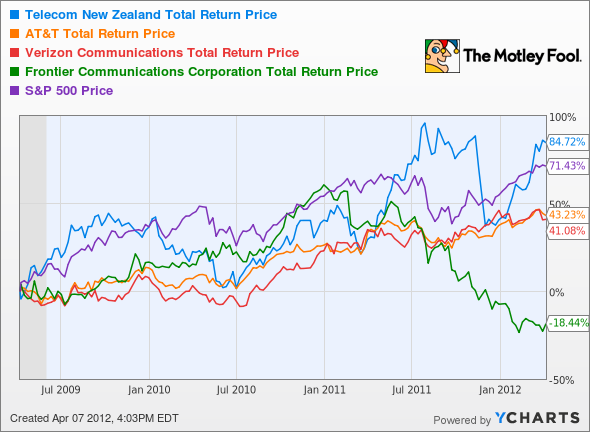

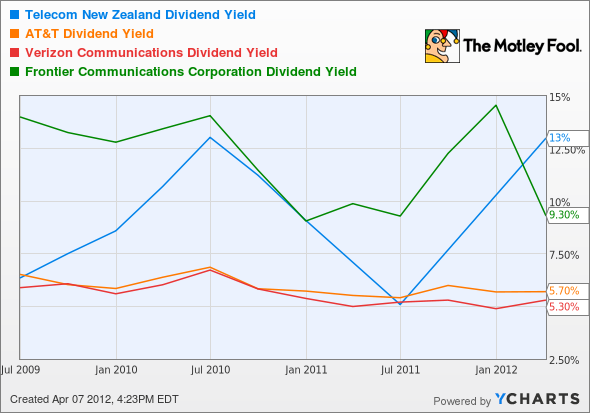

New Zealand Telecom has been perhaps the best telecom performer over the past year in spite of a big drop last November, as it's up nearly 30%, outpacing U.S. carriers AT&T (NYS: T) and Verizon (NYS: VZ) , which have both been flat. Its massive 13% dividend also easily trumps both carriers', and even leapfrogs high-payout telecom stalwart Frontier Communications (NYS: FTR) .

Metric | Trailing-12-Month (or most recent) Result |

|---|---|

Annual revenue | $4.93 billion |

Annual net income | $1.01 billion |

Profit margin | 20.4% |

Free cash flow | $507 million |

Dividend yield | 13% |

Market cap | $3.8 billion |

Price-to-earnings ratio | 4.6 |

12-month stock price growth | 27.3% |

Total customers | 1,065,000 |

Sources: Yahoo! Finance, Morningstar, Google Finance, and corporate annual report.

Steady as she goes?

You might be thinking "New Zealand? That can't be much of a growth market." Well, you'd be right. The company earned about $5.5 billion a decade ago, and its most recent trailing 12-month revenue was about $4.9 billion. Net income has fallen further over the decade as well, save for occasional jumps thanks to major divestitures -- the Yellow Pages directories in 2007 and a very recent de-merger of Chorus, its telecom utility unit. However, free cash flow has remained relatively stable over the past decade, and may be again on the upswing thanks to greater smartphone adoption (driven at least in part by iPhone sales that began last November), which often brings higher revenues per user.

Keeping it in perspective

Since it's silly to expect much growth out of a telecom operator on a rather small island, let's focus instead on the company's dividend. Fellow Fool Brian Stoffel cast a skeptical eye on both New Zealand Telecom and Frontier last year, finding that its free cash flow payout ratio was higher than Frontier's, though Frontier had a much higher normal payout ratio. Frontier also remains in the unenviable position of now owning a whole lot of Verizon's unwanted landline infrastructure, and has since cut its dividend to compensate for poor recent performance.

Telecom New Zealand, lacking the customer pools available to any American telecom, can't do much beyond tread water. That's far from a perfect stock. However, it's been a superior holding in the telecom space since the end of the recession:

NZT Total Return Price data by YCharts

Can New Zealand Telecom continue to grow at the same pace? Probably not. Its forward P/E is now projected to be 14.4, higher than either AT&T's or Verizon's. Considering the incredible gains many stocks made after the recession, none of these companies has been particularly impressive. Of course, only New Zealand Telecom has actually managed to outperform the S&P 500.

Don't focus on yield alone

Finding businesses with big dividends can be exciting, and the telecom sector certainly has its fair share of options. But there are also warning signs aplenty if you know where to look. Now, I don't think that New Zealand Telecom is about to implode -- far from it. I just recognize that its growth opportunities are limited on its native isle, and there's no promise that the yield will stay high. It's zigzagged mightily in recent years, unlike AT&T's and Verizon's, which have remained remarkably stable in comparison:

NZT Dividend Yield data by YCharts

I'm not really sold on the possibility of either the stock's trend of outperformance continuing or its dividend yield remaining this high. That's why I'm singling out New Zealand Telecom to underperform the market in The Motley Fool's CAPS, to track my call on a longer timeline. Once AT&T recovers from its recent stumbles, it may turn out to be a better telecom option.

Foolish final thoughts

There are plenty of great dividend-paying companies that offer strength and stability for a long-term portfolio. AT&T is one, but The Motley Fool's dug up a great list of eight others, and they're all included in our free report: "Secure Your Future With 9 Rock-Solid Dividend Stocks." Find out more about these great stock opportunities -- click here to claim your free copy now.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.