Alcoa's Earnings Preview

Another earnings season is upon us, and it is make-or-break time for most publicly held companies. If the company exceeds Wall Street's expectations for revenue and earnings, the stock price could be off to the races. On the other hand, any shortfall could spell disaster.

Today we will look at Alcoa (NYS: AA) , which reports after the market closes today. Alcoa produces and manages primary aluminum, fabricated aluminum, and alumina. Analysts expect Alcoa to report $5.77 billion in revenue and -$0.04 in EPS. EPS was less than the $0.28 reported last year and suggests an economy that is still recovering from the Great Recession. The company is one of the first major companies to report each quarter and used to be viewed as somewhat of a harbinger for what to expect from other companies during earnings season. However, Alcoa's results no longer carry as much weight.

Alcoa competes directly or indirectly with more than 150 other companies in the industrials and materials sectors, including Kaiser Aluminum (NAS: KALU) , Reliance Steel and Aluminum (NYS: RS) , Century Aluminum (NAS: CENX) , and AK Steel Holding (NYS: AKS) . Kaiser and Century both report April 25. Analysts are looking for $352.9 million in revenue and $0.75 in EPS from Kaiser, and Century is expected to report $324.2 million in revenue and -$0.17 EPS. AK Steel reports April 24, and analysts estimate $1.51 billion in revenue and -$0.11 EPS. Reliance reports April 26, and Wall Street expects $2.14 billion in revenue and $1.29 EPS.

When looking at earnings quality, we at The Motley Fool have two databases -- EQ Scan and EQ Score -- that help us to uncover cash flow and revenue recognition issues. Smart financial officers can use several techniques to manipulate financial results, and manipulation of any of the three financial statements usually affects the other two. But a critical eye on these statements can often uncover trends that could be important for investors to understand to help protect against them losing their hard-earned money.

The EQ Score database assigns an index rank to the company from one, for the lowest quality, to five, for the highest. As the company's financial status changes over time, the database adjusts its rank and illuminates trends that will affect earnings quality going forward.

Let's see how the earnings quality of Alcoa stacks up. The EQ Score model ranks Alcoa as a five.

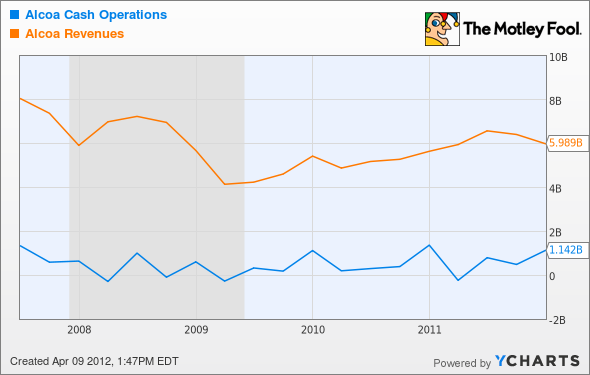

AA Cash Operations data by YCharts

The first chart shows that over the past five years Alcoa's revenue trend is down, and the effects of the recession on revenue are immediately apparent. Since the recession's end point in 2009, however, Alcoa's revenues have been growing slightly and operating cash flow is stable but with some seasonal variation, notably in the first quarter of each year. While this is a good sign, indications are that Alcoa, like the U.S. economy, has struggled with its recovery efforts.

Average operating cash flow margins have been stable at 9%. This metric is a measure of the money a company generates from its core operations per dollar of sales and is an indication of how efficient the company is at converting sales to cash. This is one of the reasons why Alcoa scores highly for earnings quality.

AA Accounts Receivable data by YCharts

The second chart shows inventories and accounts receivable both trending down over the past five years. Lower inventory levels mean improved gross margins because inventory is the major component of the cost of goods sold on the income statement. We saw that Alcoa's revenue shows an upward trend, and because of this and because there are fewer receivables, it likely means customers are paying promptly. Sure enough, days sales outstanding is trending down to a manageable 24 days, and A/R is down 1% YOY and as a percentage of revenue down 2% YOY. The improvement in DSO translates to a lower cash conversion cycle, which is down from 33 days in 2009 to 28 days in 2011. These are all positive signs that Alcoa is recovering, albeit slowly.

Unfortunately, the company is expected to report negative EPS this quarter. In the hierarchy of metrics that affect earnings quality, revenue is at the top of the chart and cash flow is more important than net income. In other words, Wall Street tends to focus on the wrong metric. Like many other companies in the materials sector, Alcoa was hit hard by the recession but shows improving revenue trends along with stable cash flows due to responsible inventory and cash management. As always, prudent Fools should make investment decisions based on consideration of earnings quality.

At the time thisarticle was published Fool contributorJohn Del Vecchiois co-advisor to Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.