RIM Keeps On Keepin' On As Execs Abandon Ship

Research In Motion (NAS: RIMM) is at it again. Disappointing, that is.

The BlackBerry maker put up fourth-quarter and full-year results this week, and after the next opening bell, shares opened higher and marched to gains of upwards of 5%. That doesn't sound as though investors are disappointed. What gives?

First, the facts

Revenue in the fourth quarter added up to $4.2 billion, about a quarter less than it was a year ago, with adjusted net income of $418 million, or $0.80 per share. Software and services have been trending up as a percentage of revenue, coming in at 32% this quarter. When you look at the figures on a GAAP basis, though, RIM actually lost $125 million, or $0.24 per share.

Where does that difference of $543 million come from? The majority of it was a $346 million goodwill impairment that the company recorded as a non-cash charge. The remaining $197 million was an inventory provision related to the valuation of BlackBerry 7 products that are sitting on the balance sheet. I told you inventory is evil.

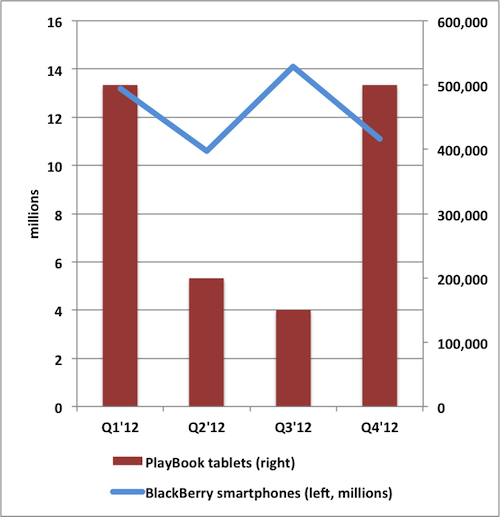

Don't forget that the company already ate an even bigger inventory charge last quarter on its glut of PlayBooks sitting around collecting dust. Speaking of PlayBooks, RIM shipped more tablets than I was expecting. The company moved "over" 500,000 PlayBooks in the quarter, which is about as many as it moved when the tablet launched in the first quarter.

Source: RIM Investor Relations.

That brings the cumulative total up to 1.35 million over the year -- more than the million tablets that Motorola Mobility (NYS: MMI) shipped over the same timeframe. On the surface, it would seem that the new, updated PlayBook OS 2.0 that was released last month is helping spur some shipments, but that's questionable, since the fiscal quarter closed less than two weeks later.

Maybe the updated PlayBook isn't as irrelevant as I thought it was. On second thought, it probably still is when you remember that Apple (NAS: AAPL) just sold 3 million iPads in a weekend -- more than twice what RIM shipped all year.

On the smartphone side, RIM shipped 11.1 million BlackBerrys, which was on the low end of the 11 million to 12 million guidance it had previously given us. That figure also shrivels next to the 37 million iPhones that Cupertino sold last quarter.

Now you see me, now you don't

Speaking of guidance, RIM has opted to "discontinue providing specific quantitative guidance," which I can only imagine means that the numbers are too embarrassing to share with the rest of the world. The pain is going to get worse before it gets better, and the company "expects continued pressure on revenue and earnings" for the next fiscal year.

RIM says it wants to focus on the longer-term business, which is why it won't be giving investors any forecasts from here on out. The company also cited "ongoing weakness" in its U.S. smartphone business as a contributing factor.

Even rats abandon a sinking ship

Ex-co-CEO and ex-co-Chairman Jim Balsillie has decided to resign from the company's board and is leaving the company that he co-founded. It was just two months ago that Balsillie and longtime BFF Mike Laziridis turned in their keys.

After 20 long years, Balsillie is calling it quits. He's not the only one, as a couple of other C-suite execs are also abandoning RIM's sinking ship. CTO of software David Yach is leaving after 13 years with the company, and COO of global operations Jim Rowan is also out to "pursue other interests."

Set the controls for the heart of the sun

Freshly minted CEO Thorsten Heins is going to have a tough time turning this thing around. Heins said the company's upcoming BlackBerry 10 OS will be RIM's platform for the next decade. He also said that the company is reviewing its strategic opportunities, which include the possibility of licensing.

Along with Balsillie's resignation, this might be what's cheering up shareholders, even though it's old news, since Samsung and RIM have reportedly been making eyes with each other. Google's (NAS: GOOG) upcoming acquisition of Motorola Mobility is expectedly causing some tensions with other Android OEMs such as Samsung, giving RIM an opportunity to cut in with an OS licensing deal. It also gives other OS makers, such as Microsoft (NAS: MSFT) , the same chance. And even though RIM's (shrinking) market share is nearly 5 times that of Windows Phone currently, I believe WP has a better chance in the long run.

Any potential turnaround for RIM is going to take time, and there's little evidence to suggest that Heins has a shot at pulling one off. David Einhorn might think it's a value buy, but I still think it's a value trap.

There are better ways to play the mobile revolution, starting from the inside. Get this report on 3 Hidden Winners of the iPhone, iPad, and Android Revolution for a list of critical component suppliers that are much more promising than RIM. It's totally free.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Apple, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Motley Fool owns shares of Google, Apple, and Microsoft.Motley Fool newsletter serviceshave recommended buying shares of Google, Microsoft, and Apple and creating bull call spread positions in Apple and Microsoft. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.