Pay No Attention to the Law of Big Numbers

Apple's (NAS: AAPL) announcement Monday that it would begin paying dividends and buying back shares capped off a dramatic run in its stock price to $600. Since the company reported quarterly earnings on Jan. 24, shares have climbed a remarkable 43%, with the vast majority of the growth coming in the weeks following the earnings release as investors digested the iPhone-maker's massive growth and anticipated the release of the new iPad and a plan to return cash to shareholders. During this rapid growth period, the company increased its market cap by $170 billion in two short months -- an unprecedented creation of shareholder value in such a brief span of time.

Still, after those two torrid months passed and the company's net income more than doubled last quarter, Apple trades at a P/E of just 17. Clearly investors don't believe the company can maintain anything like last quarter's increases of 118% in net income and 73% in revenue. Apple's growth rate has eclipsed 20% in every quarter but one since the end of 2003, yet analysts are predicting the tech titan's top line will jump just 17% from fiscal 2012 to fiscal 2013. This widespread refusal to believe large companies can sustain periods of rapid growth stems from one of the core tenets of finance -- an insidious belief that growth inevitably slows as size increases.

The law of large numbers

In math, the law of large numbers states that as a sample size grows, its mean should approach the population average. In other words, while flipping a coin three times could generate all heads or all tails, flipping it 100 times is much more likely to yield a result closer to half heads and half tails, the expected outcome. In finance, this principle has been distorted to mean that as a company grows, it becomes more difficult for it to maintain the same growth rate. Finance analysts and professors love to say that a company can't outgrow the world and therefore can't maintain a growth rate larger than the global economy's forever.

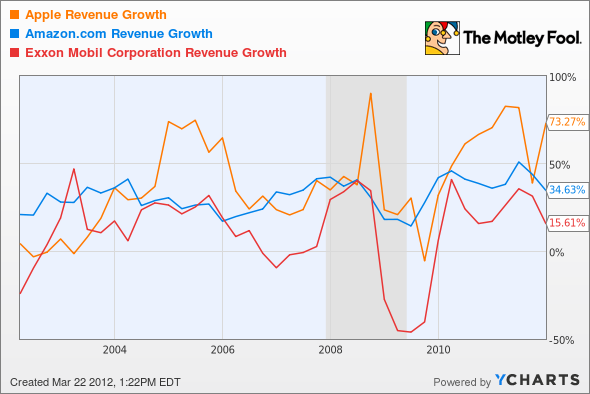

Valuation models, a huge factor in determining stock prices, almost always assume that a company's growth rate will predictably decline in the next five to 10 years before hitting a steady state of slow growth, and the models rarely allow for potential spikes in growth. A typical model, for instance, might assume that a given company will grow 10% for the next five years, 5% for the five years after that, and then 3% forever after. As Apple and many others have shown, growth can happen at any point in a company's life cycle; the model is just not realistic. The chart below shows the growth rates of Apple and ExxonMobil (NYS: XOM) , the two largest companies by market cap, as well as Amazon.com (NAS: AMZN) , the market's favorite large-growth company.

Source: Ycharts.

Based on the law of large numbers, you would expect the revenue growth rates to steadily decline over time. However, that has been far from the case. Growth has been erratic for all three companies, but it continues to trounce the S&P 500 historical average EPS growth rate of 3.8%. Cyclical factors appear to weigh much more heavily than simply time and size.

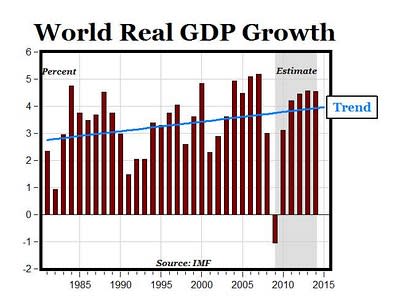

Extending the theory, one might think that the world's GDP growth rate should be gradually decreasing given its enormity, but that is not the case. As the trend line in the chart below shows, that rate has actually been increasing.

While that increase has largely come from developing countries, it underscores the point that potential growth opportunities are always out there.

Exposing the myth

The standard valuation models are deeply flawed. A company's growth rate doesn't simply descend to a certain resting rate as it expands. In a business, opportunities come and go, and the cyclical nature of economics means those growth rates are likely to be erratic. Unlike a coin flip, business results aren't random.

What really drives growth isn't a simple function of time and size, but of innovation. From the wheel to Wi-Fi, mankind's evolution has not come as a smooth curve but step by step, through discoveries that jolt society forward to a greater standard of living. We see these advancements raising the bar not just in business but in all facets of life. Countless innovations have revolutionized different sports, such as the Fosbury Flop in high jumping or Sabermetrics in baseball. In art, the invention of photography freed painters from rendering only the most realistic images, and new movements such as impressionism, cubism, and surrealism flourished as a result.

The most obvious business innovations may be technological ones, but we can also point to strategic concepts like the assembly line. These days, the mobile revolution that's led to Apple's dominance isn't the only disruptive force carving out new markets. Hydraulic fracturing has enabled a boom in natural gas production, creating new opportunities for companies like natural gas engine-makers Westport Innovations (NAS: WPRT) and Cheniere Energy (NAS: LNG) , which plans to build the U.S.'s first natural gas export terminal. Emerging markets like China have also brought new and unexpected opportunities to businesses across the world and should continue to do so.

Take another bite

The problem with the traditional valuation approach is that 10 years ago no Wall Street quant could have predicted the invention of the iPhone or the iPad, and just as certain, they cannot predict the innovations that will be changing the world 10 years from now. Companies like Apple and Google, another tech powerhouse seemingly punished for its size, will continue to push the envelope of modernity.

As for Apple's prospects, its huge profits don't actually come from dominating industries, but from creating the most sought-after, and therefore profitable, products in a given space. That model has served the Cupertino king particularly well in the smartphone market, as telecom companies have been willing to pay large amounts to subsidize the purchase of iPhones. Google, by comparison, makes little profit from its Android platform, even though it has a larger market share.

Of the nearly 6 billion mobile phone subscriptions worldwide, Apple holds just 5.6% of the market share but takes home more than half of the industry's profits. That alone is a huge opportunity, and with products like Apple TV expected this fall and who knows what else in the pipeline, it seems foolish to declare that the size alone of the world's largest company should be an obstacle to its continued growth.

Global GDP stands at $65 trillion and is growing by about $3 trillion a year. Even if Apple keeps up its incredible growth rate, it will still be decades before it outgrows the planet.

And who says we won't be on Mars by then?

At the time thisarticle was published Fool contributorJeremy Bowmanowns shares of Apple and Google but holds no other positions in the companies in this article. The Motley Fool owns shares of Apple, Google, and Amazon.com.Motley Fool newsletter serviceshave recommended buying shares of Google, Amazon.com, Westport Innovations, Apple, and ExxonMobil.Motley Fool newsletter serviceshave recommended creating a bull call spread position in Apple. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.