How Well Could These Banks Handle the Carnage?

The stress tests are out. The results helped to send Bank of America (NYS: BAC) up 22%, JPMorgan Chase (NYS: JPM) up 9%, and the Dow Jones Industrials Average (INDEX: ^DJI) up 2% for the week.

JPMorgan received permission to increase its dividends and stock buybacks. Bank of America soared after it didn't fail the tests. Of course, the test parameters focused on the results of hypothetical economic conditions, rather than worst-case losses from its legal challenges.

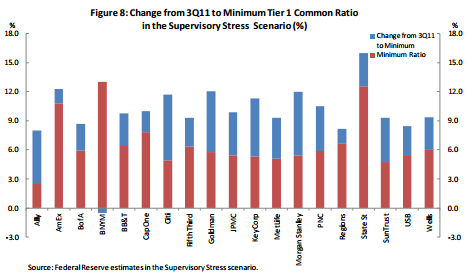

Of the 19 institutions tested, Citigroup (NYS: C) , SunTrust, MetLife, and Ally Financial were the four to fail at least one scenario.

Too-big-to-fails Wells Fargo (NYS: WFC) , Goldman Sachs (NYS: GS) , and Morgan Stanley managed to stay above the 5% Tier 1 common equity threshold.

Despite lobbying from the banks to keep details of the results secret, the Federal Reserve went ahead and released lots of useful information. Here's how the 19 fared:

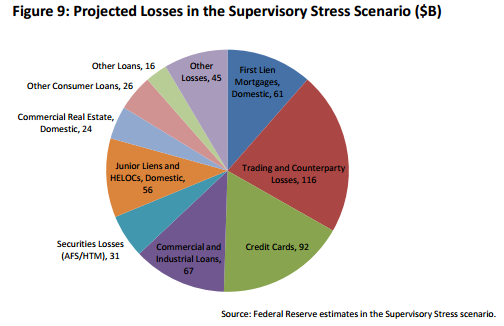

The blue amounts are losses under the test's scenario; red is how much capital would be left over after the carnage.

Although banks would take big losses on their mortgage, credit card, and commercial and industrial loans, the biggest source of losses would come result from trading and counterparties, which should remind us all that a strong Volcker Rule is so important.

Now, the test had its limitations. For one, the worst-case assumptions modeled a more severe recession than the one we just had -- mortgage losses, high unemployment, gross domestic product decline, and low interest rates. Kudos for using much more stressful assumptions than in the flimsy 2009 tests. And given the liquidity trap we're in, it makes sense that a hypothetical double-dip recession sometime over the next few years would be deflationary rather than inflationary, just like the last one. But hopefully in future tests we'll also get to see how well banks would cope with alternative kinds of financial crisis. At the very least, it would be nice to see what affect moderately rising rates would have.

More importantly, as FDIC Chair Sheila Bair recently pointed out last week, the test looked at risk-based capital levels. Future versions of the test should look at overall leverage, too, since "risk-based" can be a somewhat squishy metric.

Furthermore, the tests, which focused on solvency, aren't a guarantee that we won't see another financial panic, with a shadow banking run once again crashing the entire system.

It's encouraging to see banks performing decently under the tested scenarios, since solvency would decrease the odds that we'll have to undergo another financial crisis and possible bailout during the next recession. But we still have a long way to go to protect ourselves from the next crisis.

Looking for a simpler, safer bank than too-big-to-fail behemoths? My colleague Anand Chokkavelu highlights one name that looks like the kind of bank Warren Buffett might have bought in his earlier years in "The Stocks Only the Smartest Investors Are Buying." I invite you to download this special report for free.

At the time thisarticle was published Ilan Moscovitzdoesn't own shares of any company mentioned. You can follow him on Twitter, where he goes by@TMFDada. The Motley Fool owns shares of JPMorgan Chase, Bank of America, Wells Fargo, and Citigroup and has created a covered strangle position in Wells Fargo.Motley Fool newsletter serviceshave recommended buying shares of Goldman Sachs and Wells Fargo. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.