The Upside to a Downshifting China

Chinese premier Wen Jiabao raised eyebrows last week in a speech at the National People's Congress, the annual meeting of China's legislature. In opening remarks, Wen signaled his country's decision to lower its targeted economic growth rate to 7.5% after maintaining an 8% goal for the last seven years. While the announcement sent tremors through Wall Street, for the reasons I discuss below, the concern is not only misplaced, but outright wrong.

Why the concern is misplaced

Even assuming that China's output is beginning to moderate, it shouldn't come as a surprise to anybody. Put simply, China is no longer an emerging economy. It has emerged and now boasts the second-largest economic engine in the world. With this in mind, a 7.5% growth rate doesn't seem so bad. The last time the United States even approached that was 1984, when we recorded an annual GDP growth rate of 7.19%. Nowadays, we're lucky to hit 3%.

And the story is the same with Japan and Germany, the next largest economies in terms of output. In the last 40 years, Japan's growth rate hasn't passed 7.5%, and Germany hasn't come close. Its highest rate over this time period was a nonetheless impressive 5.26%, which it recorded in 1990. Indeed, even a bona fide emerging economy like Brazil is hard-pressed to achieve such a notable target. The last time it did so was in the mid-1980s.

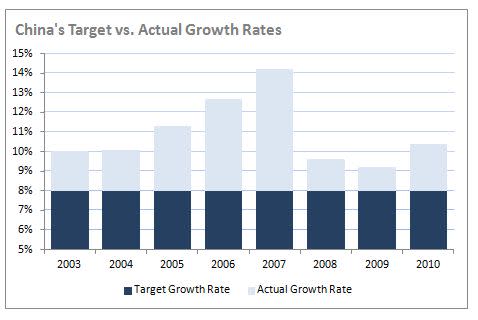

Source: Google Public Data, China's GDP growth rate: 1961-2010.

Not to mention, all this is assuming that premier Wen's economic forecast will turn out to be accurate. To test the likelihood of this, we need only look back over the last eight years during which the benchmark growth rate was 8%. And as you can see in the figure above, the actual growth rate exceeded the benchmark in all eight of the pertinent years. Even in the depth of the Great Recession, in fact, China still managed to eke out 9.2% growth. Mind you, as I mentioned previously, this is 2 percentage points higher than the United States' fastest growth rate in the last 40 years. Thus, while I'm not trying to minimize the potential consequences of a dramatically downshifting China, as that would be a disaster for the world economy, I am trying to say that Premier Wen's speech shouldn't be taken as such.

Why the concern is outright wrong

At the same time that the mainstream media obsessed over the nominal decrease in China's targeted growth rate, they almost entirely overlooked the most important part of Wen's remarks -- namely, that the decreased rate is only one part of a much broader shift in the Chinese economy, away from exports and toward greater domestic consumption. For reasons I've discussed before, this news couldn't come at a better time for Western economies.

One of the main issues plaguing the global economy right now is the historically unprecedented trade imbalance between export-oriented countries like China and import-oriented countries like the United States. In the five years between and including 2006 and 2010, for example, China's average annual current account balance exceeded $300 billion -- the current account is a proxy for trade. Over the same time period, the United States' balance was negative $600 billion. In short, this amounts to an enormous transfer of wealth between the two countries. And the net result is that we have more than $14 trillion in national debt, whereas China has over $3 trillion in foreign currency reserves.

While this imbalance was initially caused by an abundance of cheap labor in China, it's been maintained by a policy of currency manipulation. By keeping the yuan artificially cheap relative to other currencies, China has effectively subsidized its export industry -- much to the detriment and consternation of other countries. The announced shift in favor of domestic consumption, in turn, portends a shift in this policy as well. To maximize its constituents' buying power, in other words, it will now be in China's interest to allow the value of the yuan to appreciate -- which the country has begun to do in the last few years.

Thus, at the end of the day, the issue isn't so much about what the world will lose if China's growth rate decreases by half a percentage point, but rather what it will gain when over a billion new consumers come online. According to the CEO of Yum! Brands (NYS: YUM) , for example, "China is the biggest retail opportunity in the 21st century." Its competitor McDonald's (NYS: MCD) plans on opening a staggering 700 more outlets in China by 2013. And Starbucks' (NAS: SBUX) 500 Chinese locations are already more profitable per outlet than in the United States.

Foolish bottom line

For the investor, the important thing to note here is that the market's initial reaction to the news from China should not be interpreted as the beginning of an ominous turn in the world economy. Indeed, if anything, it only lends credibility to the optimistic opinions of those like Warren Buffett who believe that our best days are still ahead.

If you're on the hunt for more companies positioned to benefit from these trends, check out are recently released free report, "3 American Companies Set to Dominate the World." To access your free copy while it's still available, click here now.

At the time thisarticle was published Fool contributor John Maxfield does not own shares in any of the companies mentioned above. The Motley Fool owns shares of Starbucks.Motley Fool newsletter serviceshave recommended buying shares of McDonald's, Starbucks, and Yum! Brands.Motley Fool newsletter serviceshave recommended writing covered calls on Starbucks. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.