Why This Apple Bear Is Still Dead Wrong

This Wednesday at 12:45 PM ET/9:45 AM PT, The Motley Fool's top analysts will be hosting a live blog breaking down what Apple's iPad 3 press conference means for investors. The best part? They'll also be taking any questions you have about the tablet and about Apple as an investment. Make sure toset a reminderto come back to Fool.com this Wednesday for all your iPad 3 news and analysis!

We've been talking about ACI Research analyst and CEO Edward Zabitsky and his long-standing bearishness on Mac maker Apple (NAS: AAPL) .

So far, Zabitsky has been absolutely wrong with his call and investors who took his advice would have missed out on some market-thumping gains. That's the best-case scenario, since he's even actively recommended shorting the stock over the past several years, in which case sitting on the sidelines would look like an envious position in comparison. If you missed the previous article, check it out by clicking here.

In the past couple years, Zabitsky has somewhat changed his tune. He remains committed to his "sell" rating on the stock, but the underlying thesis to his rating has changed somewhat. Without further ado, let's get back up to speed.

2011

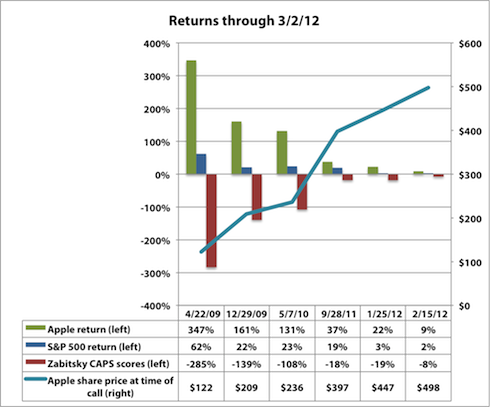

Apple shares are $397 in September as Zabitsky tells Reuters that "the platform is commoditizing," which is poised upon a belief that HTML5 will herald a new phase of Web apps that are hardware agnostic and the open Web will trump Apple's closed ecosystem. He said, "The only thing that could make me change my call is really if people stopped using browsers and carriers stopped investing in their networks."

2012

Zabitsky kicks off the year in January with a research note the morning after Apple's blowout quarter, once again harping on his view that open-content platforms will win, and complete with a $270 price target and sell-short recommendation. Shares close out the day near $447 after the results. A couple of tidbits:

"Content is king again. It is available everywhere -- not just from Apple. If we learn one thing from Netflix's (NAS: NFLX) fall from grace, it is that aggregating content is no longer a viable business model."

"Speaking of open ecosystems, what will Apple do when carriers introduce network-based video calling?"

"We maintain our Sell Short rating on Apple. The Internet is the great equalizer. It saved Apple during the rise of the wired broadband Internet. It will level the playing field for other vendors with the rise of the true mobile broadband Internet."

Just last month with shares at $498, he told Bloomberg, "I should have waited for there to be more adoption, but intellectually, I feel good about the call," adding that competition from Google's (NAS: GOOG) Android and Microsoft's (NAS: MSFT) Windows Phone should bring iPhone gross margins down from 50% to just 25%.

In reality, the iPhone 4S actually carries a gross margin near 70%.

Last Friday, Zabitsky told CNBC that he specializes in "ecosystem research," and believes we're in the midst of a "tremendous inflection point." He talked extensively about Web apps again, and how Windows 8 and Facebook bank on them.

Desperate measures

In case you haven't caught it yet, his main thesis nowadays is that open-Web apps will disrupt Apple's closed ecosystem, thus the end is (again) nigh.

His previous thesis was based on competition and carrier tensions, which had sound reasoning but just didn't pan out. Now his stance is disconnected from Apple's actual business in what I view as a move of desperation.

Relating Apple's success to apps and content services like Netflix is meaningless. Netflix is purely a content-service provider, while Apple makes its dollars on hardware. Apps are a nice selling point for iDevices and the 30% cut Cupertino garners, but ultimately even if Zabitsky is 100% correct (which he's probably not) that mobile users will migrate to Web apps and cut out the iOS App Store, that doesn't change the need for Apple's hardware as the portal to said Web apps.

Can you spare some change?

Think of it this way. Apple just disclosed that it's paid out a cumulative total of $4 billion to app developers since the App Store opened its digital doors in 2008. Developers keep 70%, while Apple takes the rest, which implies that Apple has brought in about $1.7 billion revenue from app sales in less than four years.

That's an average of $425 million per year to Apple, although app sales have accelerated in recent years, with $700 million of the developer payout -- 17.5% of the total -- in the December quarter alone. That's chump change to a company as stupid rich as Apple.

iPhone and iPad hardware sales alone over the past four quarters has totaled $85.9 billion. Do you think Cupertino would even notice a missing $425 million per year? You could probably scrounge that up digging for change in iCouch cushions at Apple headquarters, assuming the couch isn't made out of cash itself (or anodized aluminum, stainless steel, and aluminosilicate glass, which would likely lead to the dreaded Couchgate scandal).

That sum is effectively a rounding error, since the company's results are measured in the tens of billions.

Timber?

Zabitsky's $270 price target represents a 50% drop from Friday's $545 close. Apple's market cap just topped half a trillion dollars, and his target would bring that figure down to about $250 billion -- less than Microsoft's current $263 billion. That would mean that Apple's current cash alone of $97.6 billion would be almost 40% of its market cap. And you thought Apple was cheap now, at 15 times earnings? At $270 and backing out cash, shares would be valued at 4.6 times trailing earnings.

At the end of the last article, I put together what CAPS scores Zabitsky would be sporting with his calls, so let's finish off the list. In addition to the (285), (139), and (108) from last time, his bearish calls at $397, $447, and $498 would earn him scores of (18), (19), and (8), respectively, through last Friday.

Sorry, Zabitsky. You're still dead wrong.

Going long on Apple is just one way Zabitsky could have scored multibagger returns for those following him. Another way would be to look for the six signs of a Rule Breaker. If you want to Discover the Next Rule-Breaking Multibagger, look no further since The Motley Fool has just released a new special free report on one company that has all six signs of a Rule Breaker. Get the report now.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Apple, but he holds no other position in any company mentioned.Click hereto see his holdings and a short bio. The Motley Fool owns shares of Apple and Microsoft.Motley Fool newsletter serviceshave recommended buying shares of Apple, Netflix, and Microsoft; creating a bull call spread position in Apple; and creating a bull call spread position in Microsoft. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.