Is Domino's Pizza a Buffett Stock?

As the world's third-richest person and most celebrated investor, Warren Buffett attracts a lot of attention. Thousands try to glean what they can from his thinking processes and track his investments.

We can't know for sure whether Buffett is about to buy Domino's Pizza (NYS: DPZ) -- he hasn't specifically mentioned anything about it to me -- but we can discover whether it's the sort of stock that might interest him. Answering that question could also reveal whether it's a stock that should interest us. In this series, we do just that.

Writing in a recent 10-K, Buffett lays out the qualities he looks for in an investment. In addition to adequate size, proven management, and a reasonable valuation, he demands:

Consistent earnings power.

Good returns on equity with limited or no debt.

Management in place.

Simple, non-techno-mumbo-jumbo businesses.

Although the company may be too small for Buffett to literally buy shares of it, does Domino's meet Buffett's standards?

1. Earnings power

Buffett is famous for betting on a sure thing. For that reason, he likes to see companies with demonstrated earnings stability.

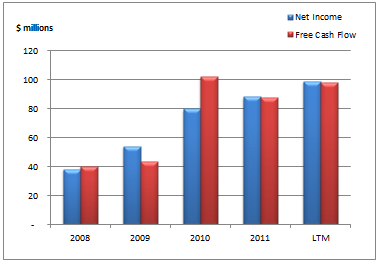

Let's examine Domino's earnings and free cash flow history:

Source: S&P Capital IQ.

Domino's has grown its earnings and free cash flow substantially over the past few years as it's turned itself around from the 2007-2008 portion of the economic downturn, but earnings seem to go through cycles every few years.

2. Return on equity and debt

Return on equity is a great metric for measuring both management's effectiveness and the strength of a company's competitive advantage or disadvantage -- a classic Buffett consideration. When considering return on equity, it's important to make sure a company doesn't have an enormous debt burden, because that will skew your calculations and make the company look much more efficient than it is.

Domino's doesn't have a return on equity because its liabilities have exceeded its assets for about a decade. That's generally -- but not necessarily -- a bad sign. Its operating margin beats Papa John's and is almost tied with Pizza Hut/KFC/Taco Bell-owner Yum! Brands', though its net margin lags the latter's.

3. Management

CEO Patrick Doyle has been at the job since only last March. Prior to that, he was at the company in various other roles for about two decades.

4. Business

Pizzas aren't particularly susceptible to wholesale technological disruption.

The Foolish conclusion

So is Domino's a Buffett stock? It's a mixed picture. Although the company operates in a technologically straightforward business and earnings are returning to form, it doesn't particularly exhibit several quintessential characteristics of a Buffett investment: consistent earnings and high returns on equity with limited debt. However, if you're interested in a retailer that our top analysts and chief investment officer picked to beat the market, you can check out The Motley Fool's Top Stock for 2012. I invite you to download this special report for a limited time by clicking here -- it's free.

At the time thisarticle was published Ilan Moscovitz doesn't own shares of any companies mentioned. The Motley Fool owns shares of Domino's Pizza. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.