Will This Iconic Brand Name Survive?

An easily identifiable brand name isn't enough to save companies from bankruptcy any longer. Eastman Kodak (OTC: EKDKQ.PK) fell victim to bankruptcy earlier this year after failing to turn around its struggling film business for nearly a decade, while General Motors caved into bankruptcy in 2009 under the weight of an incredible amount of debt.

Classic dilemma

While not of the same caliber as these two former juggernauts, tennis-shoe maker K-Swiss (NAS: KSWS) could be tempting the bankruptcy gods if it doesn't do something with its ailing business - and fast.

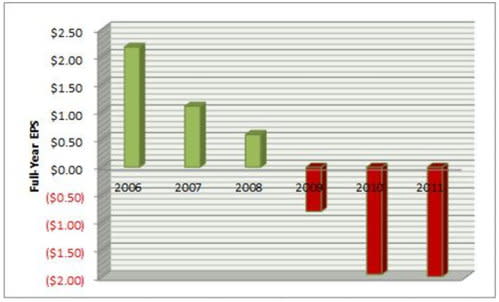

The company on Friday reported fourth-quarter and year-end results that widely missed Wall Street's estimates. For the quarter K-Swiss lost $0.71 per share, a clean $0.29 worse than analysts had predicted, while revenue rose 18% over the year-ago period. What's even more disconcerting is that K-Swiss' fiscal 2011 loss of $1.98 marked the fifth consecutive year of declining earnings.

Sources: Morningstar, K-Swiss.

Thankfully, the company's five-year revenue decline came to an end in 2011. That, however, might be the only positive that I can pull out of this earnings report.

For fiscal 2012, K-Swiss noted that worldwide future orders through June 2012 dipped 21.3% while domestic future orders plunged by 51.6%. Can anything be done to save this brand?

Back to its roots

K-Swiss' problems began when it moved away from its Classic tennis-shoe business and tried to go toe-to-toe with Nike (NYS: NKE) , Adidas (OTC: ADDYY.PK), and Skechers (NYS: SKX) for the action-sport and younger audiences. In 2010, K-Swiss purchased then seven-month-old FORM Athletics to get its foot in the door on the mixed-martial-arts audience. Fast-forward two years later, and FORM is bankrupt, with K-Swiss discontinuing its operations.

Nike in particular has been able to use the branding power of its paid athlete ambassadors to help drive sales. When was the last time K-Swiss had a sales-driving ambassador? Sorry, Jillian Michaels, you just don't have the same "buy me" appeal that Jeremy Lin has!

K-Swiss' abandoning of its bread-and-butter classic tennis-shoe business is particularly disturbing given how long the company has tried to angle the company toward the sportier side of the market and failed. It's been more than four years now, and in that time the company has burned through a good portion of its cash. In the past six years, it has lost nearly 60% of its revenue.

Management stated that its focus in 2012 will be on cost-cutting and bringing inventory levels back into historical norms -- which, as we all know, means margins could be affected as deep discounts are introduced to move older merchandise. Management also said it will continue to build out its performance/Triathlon line of products.

Go ahead and shake your head, because I'm doing the same thing. If K-Swiss has any chance of surviving, it had better return to its roots quickly. Otherwise, its tread, and investors' patience, will wear off for good.

What's your take on K-Swiss -- brand name to buy or die? Share your thoughts in the comments section below, and consider adding K-Swiss to your free and personalized watchlist.

If you want to avoid the same pitfalls that K-Swiss has endured, then I invite you to get your copy of our latest special report, "The Motley Fool's Top Stock for 2012." Find out which company our chief investment officer has dubbed the "Costco of Latin America," and best of all, you can do so for free for a limited time!

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. Shoe shopping actually bores him to death. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.Motley Fool newsletter serviceshave recommended buying shares of Nike, Skechers, and General Motors, as well as creating a diagonal call position in Nike. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policythat always rolls with its laces out.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.