1 Great Dividend You Can Buy Right Now

Dividend stocks are everywhere, but many just downright stink. In some cases, the business model is in serious jeopardy, or the dividend itself isn't sustainable. In others, the dividend is so low it's not even worth the paper your dividend check is printed on. Therefore, finding a solid dividend takes the right balance of growth, value, and sustainability.

Today, and one day each week for the rest of the year, we're going to take a look at one dividend-paying company that you can put in your portfolio for the long term without much concern. This isn't to say that these stocks don't share the same macro risks that other companies have, but they are a step above your common grade of dividend stock.

This week we're going to take a look at property and casualty insurer Tower Group (NAS: TWGP) .

The first thing that needs to be noted about Tower, and any dividend stock in general for that matter, is that it doesn't need to be huge to pack a punch or be consistent. Just because I've highlighted large-cap stocks up until this point doesn't mean only large caps should be looked to for dividend income.

Tower underwrites property and casualty insurance predominantly in the northeastern United States. As with other insurers, Hurricane Irene put a licking on results this year. In fact, catastrophe losses related to Irene pushed Tower into its first quarterly loss since going public in 2004. But don't let a one-time Act of God deter you from a company that has consistently outperformed its peers while trading at a notable discount to most of its peers.

Company | 10-Year Book Value per Share CAGR % | Forward P/E | Dividend Yield |

|---|---|---|---|

Tower Group | 31.4%* | 8.5 | 3.2% |

Allstate (NYS: ALL) | 3.8% | 7.8 | 2.7% |

Travelers (NYS: TRV) | 9.3% | 9.7 | 2.8% |

Progressive (NYS: PGR) | 9.5% | 12.7 | 1.9% |

Loews (NYS: L) | 10.1% | 11.5 | 0.7% |

Source: Morningstar, author's calculations. *Nine-year CAGR.

Acquisitions do play a part in some of Tower Group's growth story, but its organic outperformance of its peers is unmistakable. This isn't to put down the insurance sector as a whole, because many are exceptional values right now, but merely to show why Tower is the best choice of the bunch.

Loews' divestiture of its ownership in Lorillard is responsible for its compounded annual drop in revenue, but that's little comfort to shareholders currently receiving a dividend of only 0.7%. Similar to Tower, Allstate recorded a $500 million insurance loss related to Hurricane Irene, but it has not been able to put together much organic growth over the past decade, as evidenced by its 0.9% revenue growth rate. Progressive is arguably the most expensive of the bunch at 13 times forward earnings. Insurance behemoth Travelers appears to be Tower's closest competitor on paper. But with Travelers valued at a cash flow premium to Tower despite a growth rate over the past 10 years that's less than one-quarter Tower's, I'd have to say Tower is the clear value of this group.

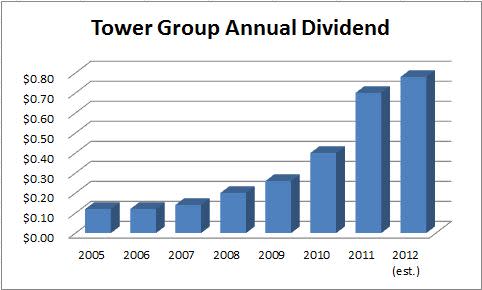

In fact, here's a quick snapshot of Tower's short, but nonetheless phenomenal, dividend history:

Source: Dividata.

The meat-and-potatoes of Tower is that despite its hurricane-related hiccup, its operations are headed in the right direction. For its catastrophe-laden third-quarter report, Tower noted a 16% increase in gross premiums written, a 7% jump in net investment income despite historically low interest rates, and an 80-basis-point drop in its net expense ratio. Not to mention that despite the quarterly loss, book value rose to $25.42 -- nearly $2 above where it's valued now. In addition to strong increases in its dividend, Tower also has a $100 million share repurchase program in place as of last year.

Foolish roundup

Insurers aren't the most exciting growth sector, but Tower has definitely broken from that mold. It has consistently outperformed its peers and it has given the market no indication that it can't continue to do so. Trust in Tower and the healthy dividend growth that it has thus far provided shareholders.

If you're craving even more dividend ideas, I invite you to download a copy of our latest special report, "11 Rock-Solid Dividend Stocks," which is loaded with income-producing companies hand-selected by our top analysts. Best of all, this report is free, so don't miss out!

Add Tower Group to my watchlist.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any of the companies mentioned in this article. He is an insurance company's worst nightmare. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that always loves a free payout.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.