An Overblown Threat to Stocks

The S&P 500 finished Thursday near its highest close in four years. And why shouldn't it have? The economy is getting stronger. Unemployment is falling. Confidence is rising. Most important, corporate profits are booming, now easily at an all-time high.

But that last one is a red flag, some say: While the economy might be in the early stages of recovery, corporate profits could be in the final, dying days of their own rebound. They point to profit margins, or the ratio of net income to sales. Since 1947, corporate profits have averaged about 6% of gross domestic product. Today, they're 9.8% of GDP. And as my colleague Alex Dumortier has shown, margins tend to be mean-reverting. If current profit margins shrink back to their historical norm, it could whack corporate profits -- and stocks.

Fearing a decline in profit margins is a fair point that shouldn't be ignored. But I think it's overblown. The connection between profit margins and profit growth is probably smaller than most assume. And the connection between profit margins and actual stock returns is virtually nonexistent.

Of course, falling profit margins lead to falling profits -- if you assume all else is equal. But all else is equal only in textbooks and on chalkboards. In the real world, changes in profit margins occur at the same time as changes in economic growth, taxes, revenue, interest rates, and shifts in bargaining power between workers and business owners. That changes everything.

Since 1950, here's how real (inflation-adjusted) corporate profit growth stacks up against corporate profit margins:

Period | Real Corporate Profit Growth | Profit Margin at Beginning of Period |

|---|---|---|

1950-1960 | 1.8% | 9.8% |

1960-1970 | 2.1% | 5.5% |

1970-1980 | 6.9% | 4.2% |

1980-1990 | (1.9%) | 5.6% |

1990-2000 | 5% | 4.6% |

2000-2010 | 7.7% | 5.1% |

Current | -- | 9.8% |

Source: Federal Reserve, author's calculations.

There is a connection between profit growth and profit margins, but it's probably smaller than you think. Margins fell by nearly half between 1950 and 1960, yet earnings still grew at a nice clip -- 21% in real terms. Profit margins then stayed mostly flat between 1980 and 1990, and earnings sank. Margins stayed flat again throughout the 1990s, and earnings boomed. Any connection that does exist isn't strong enough to bet on.

Rather than fret over what happens if margins fall, a better question is: Why are today's margins so high?

I recently sat down with Wharton professor Jeremy Siegel. When I asked him about the impact falling profit margins could have on stocks, he shook his head, disagreeing with the idea that margins are bound to fall. "Profit margins are higher on foreign sales, and everyone knows the percentage of foreign sales has been going way up," he said. "It also has to do with technology, which is very big on our foreign sales, and has by far the highest margins of any of the industrial sectors. So especially when technology sales are expanding, that's a permanent increase, I think, in those profit margins."

A simple example shows what he means. When General Motors (NYS: GM) was one of the nation's largest and most dominant companies in the 1960s, it had a profit margin of about 7%. Apple (NAS: AAPL) , today's largest and arguably most important company, has a profit margin of 24%. High-margin technology-based industries have increased to 4.6% of GDP today from an immeasurable amount 50 years ago. Manufacturing, famous for razor-thin margins, has declined from 25% of GDP in 1960 to 11% in 2009. It should be no wonder that overall margins have risen over time.

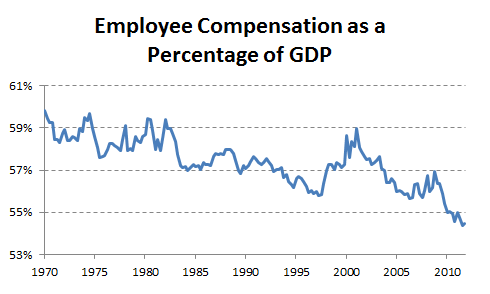

A more powerful cause of today's high margins is businesses' push to become lean and efficient. For the last 40 years, employee compensation as a share of GDP has been declining, but the trend went berserk around 2008 as businesses slashed overhead and squeezed work out of existing workers in order to keep profits intact as the economy sank:

Source: Federal Reserve, author's calculations.

To the extent this chart explains why profit margins are currently high, there's an important corollary. If profit margins are high because businesses are operating with low headcounts and paying low wages, then margins will fall only when businesses ramp up hiring and pay better wages.

Would that be bad for profits? It would not. Lower unemployment and stronger consumers would clearly be better for business. If profit margins fall but revenue rises, profits can still be superb. Indeed, this is what happened in the late 1990s -- margins fell from 6.5% in 1996 to 5.1% in 2000 as compensation expenses rose, but profits kept up nicely because revenue grew in lockstep. It's likely that we'll experience the same going forward: falling margins, but still-strong profits.

None of this, however, should really matter to investors. The most important set of numbers in this debate are these:

Period | S&P 500 Return | Change in Profit Margin |

|---|---|---|

1950-1960 | 210.5% | (4.3%) |

1960-1970 | 22.5% | (1.3%) |

1970-1980 | 7.5% | 1.4% |

1980-1990 | 214.8% | (1%) |

1990-2000 | 303.6% | 0.4% |

2000-2010 | (2.7%) | 4.7% |

Sources: S&P Capital IQ, Federal Reserve, author's calculations.

In a separate conversation last October, Professor Siegel made a telling comment in reference to stock valuations: "You don't need [earnings] growth to justify these numbers." If stocks are cheap, you don't need high earnings growth to get big returns. And if stocks are expensive, even huge earnings growth can leave investors underwater.

This is exactly what we've seen over history. Profit margins plunged in the 1950s and earnings growth slowed, but stocks boomed because they were cheap at the beginning of the period. Same in the 1980s. The 2000s saw a big jump in margins and the fastest profit growth in history, yet it was one of the worst decades for investors ever because stocks were so grossly overvalued in 2000.

The important question, then, is whether stocks are currently cheap or expensive. Alas, that debate offers no clear-cut answers. Opinions of equally smart investors currently range from "dirt cheap" to "way overvalued."

But the broader point remains. Whether margins are going to fall, or even whether earnings are going to decline, is not the end-all of importance. What matters is whether valuations anticipate those things happening. Being diagnosed with the flu can be spectacular news if you expected it to be cancer. Investing is similar. It's all relative.

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.

At the time thisarticle was published Fool contributorMorgan Houseldoesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel.The Motley Fool owns shares of Apple. Motley Fool newsletter services have recommended buying shares of Apple and General Motors. Motley Fool newsletter services have recommended creating a bull call spread position in Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.