1 Great Dividend You Can Buy Right Now

Dividend stocks are everywhere, but many just downright stink. In some cases, the business model is in serious jeopardy, or the dividend itself isn't sustainable. In others, the dividend is so low it's not even worth the paper your dividend check is printed on. Therefore, finding a solid dividend takes the right balance of growth, value, and sustainability.

Today, and one day each week for the rest of the year, we're going to take a look at one dividend-paying company that you can put in your portfolio for the long term without much concern. This isn't to say that these stocks don't share the same macro risks that other companies have, but they are a step above your common grade of dividend stock.

This week we're going to take a look at farm and construction equipment manufacturer Deere (NYS: DE) .

Not everyone would be too excited about purchasing Deere considering that 2011 was the best year for farmers in decades. Commodity prices in some cases were the highest on record, and farmers, in turn, used those excess profits to reinvest in machinery from companies like Deere. But what many often fail to realize is that Deere's growth is stemming from all of its business segments, not just agriculture.

Deere's financial services operations contributed $615 million in revenue in the fourth quarter, a 14% increase over the year-ago period and 7% of total quarterly revenue. Profit in this segment increased by a healthy 41% and is benefiting from lower loss reserves and historically low lending rates.

The company's Construction & Forestry segment provided the strongest sales growth, with a 34% jump in year-over-year revenue and a 61% pop in profit. This segment saw higher price realizations and stronger volumes that more than negated higher raw material costs.

Of course, the main draw of Deere for many will be its Agriculture & Turf division, which recorded an 18% jump in sales in the fourth quarter to $6.3 billion, thanks to higher price realizations and better shipping volumes.

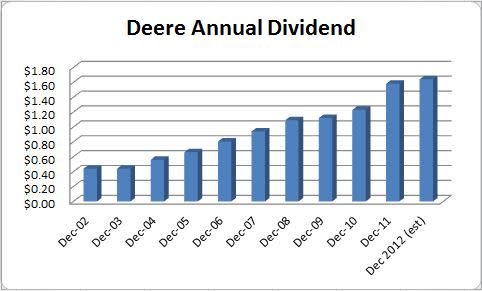

What often flies under the radar that investors should be taking note of is Deere's impressive dividend growth. Agricultural stocks aren't often known for their robust dividends -- and trust me, 10 years ago, Deere's dividend wasn't very impressive. Having grown that dividend in each year since 2003 at an annualized rate of 13.6% over the past decade, however, income-seeking investors would be (small-f) foolish to ignore the company's efforts to reward shareholders both through share repurchases and dividend increases:

Source: Dividata. 2012 payout is author's estimate based on $0.41 quarterly payout.

Despite the fact that Deere is trading within $11 of its all-time high of $99.80, on paper and relative to its peers, Deere is as cheap as it has been in years.

Company | Forward P/E | Price/Cash Flow | 5-Yr. Rev. CAGR % | Dividend Yield |

|---|---|---|---|---|

Deere | 10.4 | 15.9 | 7.6% | 1.9% |

Caterpillar (NYS: CAT) | 9.9 | 9.8 | 3.2% | 1.6% |

CNH Global (NYS: CNH) | 9.3 | 10.8 | 4.4% | 0 |

Komatsu (OTC: KMTUY) | 11.5 | 26.5 | 1.6% | 1.6% |

Terex (NYS: TEX) | 14.8 | N/M | (7.1%) | 0 |

Source: Morningstar, N/M = not meaningful.

Deere offers the best dividend yield and the strongest five-year annualized sales growth rate among its peers. Caterpillar, which I see more as a complement to owning Deere than as a line-in-the-sand choice between the two, offers a marginally better value relative to cash flow. Similarly, CNH offers the lowest forward P/E of the group, but its lack of a dividend makes it an easy pass for income seekers. Terex can also be eliminated for its lack of a dividend and its negative annualized sales growth over the past five years. Komatsu's growth rate and high price relative to cash flow also fail to impress me.

Foolish roundup

Deere has worldwide brand name recognition and the lion's share of the agricultural equipment market. Add in a growing world population that needs to eat, and I feel that bodes well for the company's long-term growth prospects. While not impervious to recessions, Deere offers the right balance of growth and value that dividend-seeking investors would love to have in their portfolio.

If you're craving even more dividend ideas, I invite you to download a copy of our latest special report, "11 Rock-Solid Dividend Stocks," which is loaded with income-producing companies hand-selected by our top analysts. Best of all, this report is free, so don't miss out!

Add Deere to my watchlist.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any of the companies mentioned in this article. He has yet to successfully take care of a plant without eventually killing it. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that always loves a free payout.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.