My 5 Worst Stocks in the S&P 500

I can think of a million things to do on a Friday night -- apparently one of those things is to run stock screens on companies that comprise the S&P 500 index.

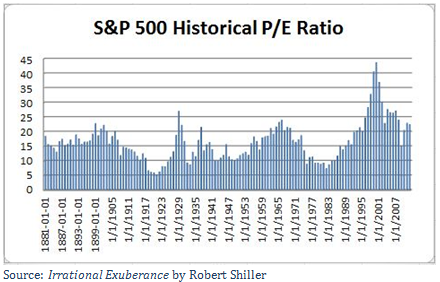

With the stock market in rally mode and the S&P 500 hitting levels it hasn't seen in three-and-a-half years, I'd be lying if I said I wasn't concerned about stock valuations getting ahead of themselves. Certain sectors are still so far from their highs (e.g. financials) that a rally seems reasonable. But make no mistake about it -- the S&P 500 is in no way, form, or shape, cheap.

With an average P/E ratio over the last 131 years of 15.8, the current P/E of 22.5 still sits well ahead of the norm. In fact, the S&P 500 hasn't been below the mean in 21 years!

Clearly there are factors that have driven the S&P 500 higher over time. The technological revolution over the past two decades has completely transformed the way we do business. In addition, accessibility to information for the layman has gone from reading a newspaper to point-and-click convenience in just 20 years.

If anything though, the above chart gives an undeniable visualization that allows you to see where the greatest valuation bubbles through history have occurred.

It's with this in mind that I set out to find the weakest links in the S&P 500. I singled out five stocks that I feel simply don't have what it takes to stand the test of time. If the S&P 500 continues to trade higher (and trust me, despite being a realist, you'll get no complaints from me if that keeps happening) I would expect investors to become increasingly skeptical of these five companies.

Sears Holdings (NAS: SHLD)

Sears could very well be the worst company in the S&P 500 and is one of the few whose survival is actually in question.

Late last year, the once-iconic retail chain outlined a plan to close up to 120 Sears and Kmart locations as it struggles to control costs and return to profitability. It has seen its debt balloon from $3.5 billion to $4.6 billion in just one year, while its cash balance has dropped by more than half to just $632 million. With sales falling a mind-numbing 19 consecutive quarters, Sears has failed to control its inventory and drive interest in the few remaining brand names that matter (e.g. Craftsman and Kenmore). It could just be a matter of time before Sears finds itself in the same company as Eastman Kodak and American Airlines.

Gap (NYS: GPS)

If same-store sales declines were fashionable, then Gap would be a trendsetter. The clothing company lost its pizzazz more than a decade ago and simply hasn't been able to rekindle the spark that made it one of the best performers of the 1990s.

Primary to Gap's downfall has been easier access to cheaper and potential chicer clothing choices. Gap's inventory has either been not what customers want or it has simply been too expensive relative to what consumers can get at Target, Wal-Mart, or numerous mall-based retailers. Gap's management team has also been slow to respond to consumers' changing demands for better values and different styles. Stubbornness from the top is driving this trendsetter into the ground and I'd highly recommend parting ways with Gap before it splits at the seam.

Capital One Financial (NYS: COF)

I've picked on Capital One a lot over the past year, but with good reason. Capital One, more than any other bank, has very large ties to the credit market. More than 80% of the company's revenue is derived from its credit card business which I feel places it at significant risk if delinquencies begin rising.

Unfortunately for Capital One shareholders there isn't just one end-all reason why delinquency rates would rise. As I see it, the myriad possible causes for rising delinquency rates include falling housing prices, high unemployment rates, alt-a mortgage resets, and European macroeconomic uncertainty. I'm sure there are other reasons I haven't even considered, but the primary takeaway is that Capital One is far too levered to the credit markets and that could wind up coming back to bite it in the behind sooner rather than later.

First Solar (NAS: FSLR)

Solar does appear in the cards for the future, but the stark reality as of now is there's simply too much supply and not enough demand to justify many of these solar companies' valuations even with many of them down more than 80% off their highs.

First Solar significantly reduced its revenue guidance in late December and the sector still hasn't shown any signs of solar panel prices stabilizing. It could easily take years before the oversupply in this sector is sorted out and it's quite possible that solar's biggest proponents up until now -- Germany and Italy -- could be down for the count after austerity measures are firmly in place and these countries fight just to stay out of a prolonged recession. I cautioned investors in December that heavy insider selling coupled with rapidly falling earnings estimates were a tell-tale sign to sell and I'm sticking by that assertion.

Altria (NYS: MO)

Much like Budweiser has been replaced as the King of Beers by light beers, I feel Altria is fighting a losing battle against the trend toward a healthier consumer.

Altria has already felt the pangs of this trend by laying off about 15% of its workforce in response to slowing sales of its flagship Marlboro brand and increased competition from discount cigarette brands Maverick and Pall Mall. The legal prospects for Altria also look grim. The U.S. is arguably the most stringent country to operate a business in, and with no diversification outside of the U.S. in terms of cigarette production it could see its business slowly crushed by lawsuits. The addition of large health warning labels on cigarette packaging this year is not bound to help its cause either. Even with investments in SABMiller, I don't see a bright future for Altria and think shareholders investing now are getting just the butt.

Foolish roundup

With 500 companies in the S&P 500 there are bound to be losers. These five represent my choices for the worst investments in the S&P 500 and shareholders in these stocks should be cautious moving forward, especially if investors like me continue to grow skeptical of the S&P 500's rising P/E ratio.

What's your pick for the worst company in the S&P 500? Share it in the comment section below and consider adding these five stocks to your free and personalized watchlist.

Also, to avoid the pitfalls of poor investments, consider downloading your copy of our latest special report, "11 Rock-Solid Dividend Stocks," in which our analysts handpick a handful of companies that should do well regardless of whether the economy is booming or in a recession. Best of all, this report is completely free for a limited time!

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. He's always looking for the proverbial needle in the haystack . You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool owns shares of Apple, Gap, Wal-Mart Stores, Altria Group, and First Solar.Motley Fool newsletter serviceshave recommended buying shares of Apple, Wal-Mart Stores, and First Solar, as well as creating a bull call spread position in Apple and a diagonal call position in Wal-Mart Stores. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policythat'll always be best of breed.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.