Deja Vu for Amazon.com

Gather 'round, fair readers, for I have a tale to tell. 'Tis one full of twists and turns, of glee and anarchy, of soaring hopes and shattered dreams, and of forward-looking financial guidance that's leaving some wanting more.

'Twas a fiscal quarter long ago, when e-tail Goliath Amazon.com (NAS: AMZN) reported top-line revenue jumping by more than a third, while net income plunged by more than half. Free cash flow sank by about a sixth, while the company warned that the coming quarter could see an operating loss as high as $200 million, leading to a sell-off the following morn.

Can't shake this feeling

You may think I'm referring to Amazon's fourth-quarter results that were announced last night, but it turns out I'm actually speaking about its third-quarter figures (OK, it wasn't actually long ago). All of the above actually applies to both of the past two quarters, and the menacing rhetoric has been a unifying theme, leading to a distinct feeling of deja vu for this Foolish shareholder.

Last time around, revenue grew 44%, net income fell 73%, free cash flow shrank 17%, and operating income was forecast for -$200 million to $250 million.

This time around, revenue grew 35%, net income fell 58%, free cash flow shrank 17%, and operating income was forecast for -$200 million to $100 million.

It's no wonder shares are also seeing similar action, having lost 13% after the third-quarter release and currently down about 10% today as of this writing.

A flaming elephant

The clear elephant in the room was the Kindle Fire. Everyone wants to get their hands on some cold hard numbers when it comes to Kindle Fire unit shipments and naturally stack those digits up against Apple (NAS: AAPL) iPad units and fellow Google (NAS: GOOG) Android tablets, but Amazon has always played this one close to the chest.

Amazon is frustratingly vague on the topic, but it has given us some clues. It had previously said that throughout December, it sold "well over 1 million Kindle devices per week," so there's 4 million units to bank on from December alone, including the Fire. The Fire began shipping in mid-November, meaning it had about seven weeks in the quarter to move.

The only solid data point Amazon gave us is that the Kindle lineup saw unit sales soar 177%, including the Fire and e-readers. Analysts have pegged Fire shipments upward of 6 million in the quarter, but we're left to our own devices on this one.

Cause and effect

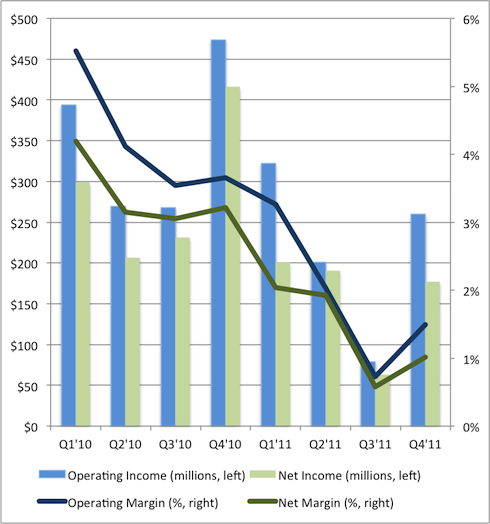

First-quarter guidance calls for revenue of $12 billion to $13.4 billion, the midpoint of which would represent a 29% increase over the prior year. The ominous prediction that Amazon may generate an operating loss upward of $200 million is rattling investors. Even though the warning echoes last quarter's guidance, Amazon just posted operating income of $260 million, slightly topping the upper-end $250 million it had predicted.

This is cause for concern among shareholders right now:

Source: SEC filings.

That big bad chart paints a scary-looking downtrend in operating and net income, but the most important thing to remember is that those figures aren't a result of Amazon's underlying business degrading, but are rather evidence that Amazon is continuing to invest in future growth.

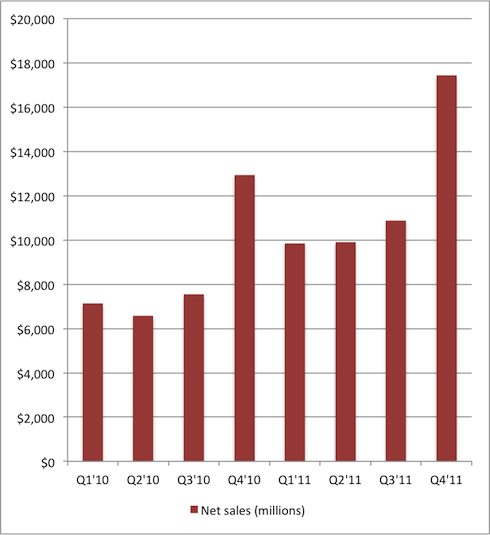

On the contrary, this is the effect of Amazon spending big bucks beefing up infrastructure:

Source: SEC filings.

Those investments are helping to drive top-line growth, and CFO Thomas Szkutak reaffirmed Amazon's stance on the conference call: "We're incredibly optimistic about the opportunity that we have, and that's why we have invested the way we have and why we're continuing to invest in the business. So we're very pleased to see it and very pleased to have the opportunities that we have in front of us."

Amazon's slim margins and high multiples may be a downside for some Fools, but I'll reiterate what I said last quarter: "Taking some short-term pain for long-term gain is simply the name of the game."

You promised me glee and anarchy

CEO Jeff Bezos is a visionary. At the tender age of 48, he still has plenty of years ahead of him. Those years will see him venture into and disrupt even more markets.

Amazon may be spinning off its online video streaming service, breaking it off from the current Prime bundle into a stand-alone service to challenge Netflix (NAS: NFLX) . Prime Video has expanded so aggressively, with Glee and Sons of Anarchy being just the most recent additions.

I like where Bezos is taking Amazon, selling Kindle Fires effectively at cost to grow an installed base that serves as a portal directly into wallets, while focusing on content offerings like subscription video streaming, its own Android Appstore, and the requisite e-books.

Anarchy may be the theme of today's sell-off, but I think glee will win out in the long haul.

At the time thisarticle was published Fool contributor Evan Niu owns shares of Apple and Amazon.com, but he holds no other position in any company mentioned. Click here to see his holdings and a short bio. The Motley Fool owns shares of Google, Amazon.com, and Apple. Motley Fool newsletter services have recommended buying shares of Google, Amazon.com, Apple, and Netflix. Motley Fool newsletter services have recommended creating a bull call spread position in Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.