Is Quest Diagnostics' Buyback Good for Investors?

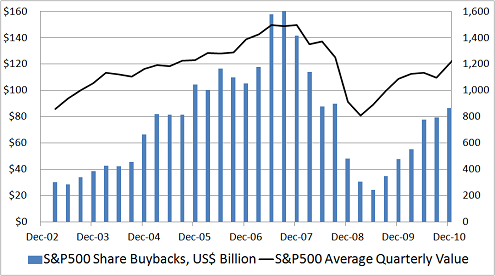

I'm highly skeptical about the economic value of most share repurchase programs. To see why, look at the following graph of the total buyback dollar amount for the companies in the S&P 500, compared to the average price of the index on a quarterly basis:

Source: Standard & Poor's.

Share buybacks for the S&P 500 accelerated in the second half of 2004, culminating in a sharp spike during the first two quarters of 2007 -- just as the stock market was peaking. Conversely, when stocks traded at bargain prices during the worst of the crisis, share buybacks dried up. Then, as stocks became more expensive during the rally that began in March 2009, companies were once more happy to step up the dollar amounts spent on share repurchases.

Still, not all buyback programs hurt shareholders. In order to ferret out the smart capital allocators and shame those who fritter away shareholder capital, I'm tracking newly announced share repurchase programs. Today, it's the turn of diagnostic-testing specialist Quest Diagnostics (NYS: DGX) .

How much, for how long?

Quest Diagnostics' new repurchase authorization adds $1 billion to the current program for a total of $1.1 billion, with no other restrictions on the program.

How cheap is the stock?

The buyback announcement contains no reference to price or intrinsic value. That's a red flag, because the relationship between price paid and intrinsic value is the only factor that determines whether the share repurchases are compounding or destroying shareholder wealth. How are we to know that Quest Diagnostics' management understands this -- or whether they care? Just how cheap (or expensive) are the shares right now? Based on price-to-earnings, Quest Diagnostics shares trade at the bottom of a group of four of its peers:

Company | Forward P/E |

|---|---|

Boston Scientific | 14.5 |

Laboratory Corp. of America | 14.2 |

Becton, Dickinson | 13.6 |

Omnicare | 13.2 |

Quest Diagnostics | 12.9 |

Source: S&P Capital IQ.

Is this a buy signal?

Quest Diagnostics' price-to-earnings multiple is in the bottom half relative to its own five-year history and its primary industry group, and right in the middle quintile relative to all S&P 500 stocks. At 14.5 times next twelve months' estimated earnings, the shares look like an acceptable -- but no better than acceptable -- use of shareholders' money.

Take a look at what Fool analysts believe is the next rule-breaking multibagger. Get the free report by clicking here.

At the time thisarticle was published Fool contributorAlex Dumortierholds no position in any company mentioned.Click hereto see his holdings and a short bio. You can follow himon Twitter.Motley Fool newsletter serviceshave recommended buying shares of Becton, Laboratory of America Holdings, and Quest Diagnostics. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.