1 Great Dividend You Can Buy Right Now

Dividend stocks are everywhere, but many just downright stink. In some cases, the business model is in serious jeopardy, or the dividend itself isn't sustainable. In others, the dividend is so low it's not even worth the paper your dividend check is printed on. Therefore, finding a solid dividend takes the right balance of growth, value, and sustainability.

Today, and one day each week for the rest of the year, we're going to take a look at one dividend-paying company that you can put in your portfolio for the long term without much concern. This isn't to say that these stocks don't share the same macro risks that other companies have, but they are a step above your common grade of dividend stock.

This week we're going to take a look at oil exploration and refining giant ConocoPhillips (NYS: COP) .

Some of you felt slighted that, in my recent argument in favor of buying natural gas, I left Conoco out of the equation -- this will hopefully remove the bad taste in your mouths.

Conoco has Wall Street abuzz over its plans to split its slower growth downstream operations (refining and marketing) from its faster-growing and high-margin upstream operations (oil exploration). If Marathon has served as any indication of what to expect, then shareholders may want to sit down. Marathon split its operations in the same manner last year. Prior to splitting its operations, Marathon was paying out $1 in annual dividends. Currently, Marathon Petroleum (NYS: MPC) , the company's downstream segment, pays out $1 in dividends annually while Marathon Oil (NYS: MRO) tacks on another $0.60. I'm no math wizard, but that's a 60% dividend hike in a year!

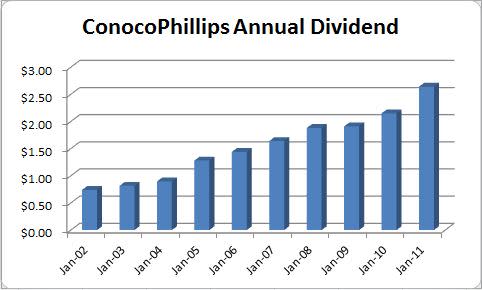

Conoco has already stated that the exploration side of its business plans to keep its already healthy dividend and the refining segment will almost assuredly pay a dividend as well. There's been no indication about the size of the refining dividend, but just take a look at Conoco's recent history of dividend payments:

Source: Dividata.

Conoco has raised its dividend for the past 11 years and boasts an annual growth rate of 13.6% on its dividend over the past decade. With oil prices hovering around $100 and the company readying to split into two, this figure is likely to move even higher.

These aren't just fringe numbers either -- there are solid results underlying these dividend gains. In fact, Conoco just reported fourth-quarter results on Wednesday that crushed Wall Street's expectations. Profits jumped 66% and the company announced the repurchase of another 3% of outstanding shares. Conoco also plans to curtail natural gas production in the U.S. with the hope, like other natural gas producers, of buoying the price of natural gas. Refining utilization rates also ended the year on a high note both domestically and internationally.

Relative to its Big Oil peers ExxonMobil (NYS: XOM) and Chevron (NYS: CVX) , Conoco is also cheaper based on nearly every metric below:

Company | Forward P/E | Price/Book | Price/Cash Flow | Dividend Yield |

|---|---|---|---|---|

ConocoPhillips | 8.5 | 1.4 | 4.9 | 3.8% |

ExxonMobil | 10.5 | 2.7 | 7.4 | 2.2% |

Chevron | 8.2 | 1.8 | 5.3 | 3.0% |

Source: Morningstar.

This isn't to say that Exxon and Chevron aren't solid buys, because I actually happen to like both quite a lot. Chevron is actually one of my "10 Large Caps to Rule Them All" and Exxon is one of my strongest recommendations for playing the eventual bounce in natural gas. These figures do present evidence though that Conoco is being undervalued by investors and could have the potential to outperform its peers once it splits its businesses up sometime in the first half of 2012.

Foolish roundup

Some of the healthiest dividends around can be found in the energy sector. Conoco represents the perfect balance of value, growth, and sustainability that I look for in an income-producing stock and appears to be a nice value relative to its peers. I'm planning on maintaining my CAPScall of outperform on Conoco throughout 2012. The question now is: Would you do the same?

If you're craving even more dividend ideas, I invite you to download a copy of our latest special report, "11 Rock-Solid Dividend Stocks," which is loaded with income-producing companies hand-selected by our top analysts. Best of all, this report is free, so don't miss out!

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any of the companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong. Motley Fool newsletter services have recommended buying shares of Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that always loves a free payout.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.