Is Netflix's Stock Growing Too Fast?

Few (if any) companies can ever be called a sure thing. When everything goes right, something can still go wrong, and a single misstep can undo years of gains. Netflix (NAS: NFLX) shareholders found this out the hard way in 2011. But 2012 has been good so far to the company behind the red envelope, as its stock has bounced big-time in just the first few trading days of the year. Was Netflix undervalued before the bump? Is it still undervalued now? Let's take a look.

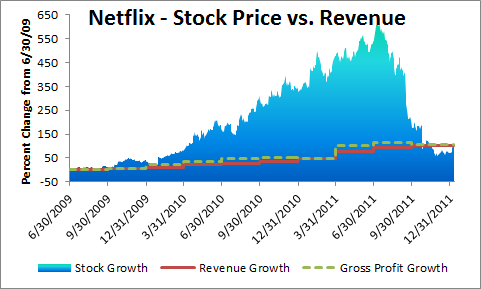

Graphing the growth

Netflix was a classic case of high-growth hype. Lofty expectations and extreme investor interest overwhelmed analysis of the fundamentals, which led to a bubble-like rise all but begging for a reason to pop. The company was growing subscriptions and revenue at a fantastic rate, but its stock was going even faster. Nothing lasts forever, unfortunately.

A company should be improving its profitability along with its revenue for investors to take it seriously. It's one thing to sacrifice profit for explosive growth, hoping to turn on the afterburners later. But Netflix, after a decade of operation, is quite profitable. Its current P/E, at just under 22, now has more in common with successful blue chips than with Amazon.com (NAS: AMZN) , one of its major streaming rivals (and still seen as a monster growth stock after more than a decade). But is it, again, growing too quickly? Take a peek at the divergence between Netflix's operating metrics and its share price.

Sources: Yahoo! Finance and Morningstar.

But what does it mean?

Netflix's stock took off at the end of 2009, rapidly outpacing its fast-growing revenue stream. The company had some significant stumbles as the bubble inflated, including share buybacks on the way up and a big stock sale close to the bottom. Shareholders had to endure a stomach-churning drop that followed a string of bad news, including price hikes, poor guidance, subscriber losses, and the ill-advised Qwikster fiasco.

With all that behind it, Netflix is now in a position it hasn't seen since 2009: Its stock price growth is now back in line with revenue and gross earnings. But if you'd jumped in during the summer of 2009, you'd be sporting better returns than the Dow. The long, strange trip back from the depths of 2008-2009 has seen the index rise about 48%, but Netflix is still up 130% since then. 2012's big bounce has helped a lot, but upcoming earnings (keep your eyes peeled) will do much to set the tone for the rest of Netflix's year. It's likely to be a wilder ride than an index fund, so strap in and hold on tight.

Foolish final thoughts

If you're a Netflix bull, things ought to look a bit more promising than they did on the way down. However, it pays to keep an eye on the company's expansion, particularly overseas, and its efforts to recapture customer love lost through multiple blunders last summer. Add Netflix to your Watchlist so you can keep informed of the "Red Envelope Recovery." If you're looking for other companies making waves internationally, take a look at this brand-new free report, just released by The Motley Fool, on three American companies that will soon dominate the world. Get your copy now -- just click here.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter for more news and insights. The Motley Fool owns shares of Amazon.com. Motley Fool newsletter services have recommended buying shares of Amazon.com and Netflix. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.