I Will Not Let 2012 Go by Without Paying Myself

It's safe to say that I made some pretty poor choices in 2011. I stubbornly ran headfirst into the China craze and chose to stand behind some companies with questionable business models. Not only did some of my predictions make me out to be a fool (with a small "f"), but my portfolio also felt a pinch due to my insistence on buying what I perceived to be undervalued Chinese small-cap stocks.

Thankfully, with each new year comes the opportunity to redeem oneself. While last year was a long cry from my best year ever, I was able to reflect on my mistakes, whether they be actions I took or should have taken, and enter the new year with a new resolve to be better.

My 2012 goal

I've therefore made it my goal that 2012 is going to be a year that I'm going to take the initiative and do something that I've been promising myself I'd do for years. This will be the year that I pay myself by investing in dividend-paying companies.

There aren't any valid reasons I should be avoiding dividend stocks, but the lure of higher growth rates and having witnessed small caps outperform large caps in nine of the past 11 years has been a temptation too strong to pass up. Now, well into my 13th year of investing, I've realized just how stupid it's been of me to turn down free money for all of those previous years. There were 1,953 reported dividend increases totaling $50.2 billion in 2011, a sizable increase over 2010, and I didn't take advantage of any of those increases.

Although I can't guarantee that every stock I buy this year will pay a dividend, fellow Fool Morgan Housel's series "The Extraordinary Power of Dividends," in which he looked at dozens of companies and chronicled their dividend-adjusted returns to investors, is enough motivation for me to get off my behind and get started on paying myself back!

The stocks that will help me achieve my goal

Here are a few names that I'm considering in 2012 to help me in my quest:

Annaly Capital Management (NYS: NLY)

It's not necessary to always go after the highest-yielding dividend companies to get the best results, but Annaly's double-digit yield is the exception to the rule. Annaly invests in U.S. government-backed mortgage-backed securities and turns a profit on the difference between the rate at which it borrows and the rate at which it lends. With the Federal Reserve promising to leave lending rates at historic lows through mid-2013, Annaly's dividend staying in double digits is a good bet. Annaly will provide my portfolio with a low-beta, high-yielding stock that could double my investment based on the dividend alone within just a couple of years if the proceeds are reinvested.

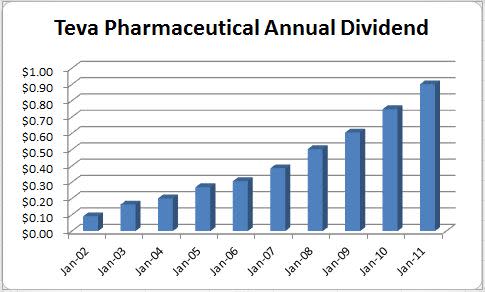

Teva Pharmaceutical (NAS: TEVA)

Sometimes it isn't just about the dividend. In the case of generic-drug giant Teva Pharmaceutical it's about the potential for that dividend to grow and the stability of the company's cash flow. Over the last decade, the compounded annual growth rate of Teva's dividend has been a staggering 29.9%.

Source: Dividata.

On top of this, the majority of Teva's sales are derived from its generic-drug portfolio of approximately 1,450 molecules. With countless applications still awaiting approval worldwide and a never-ending supply of drugs facing a patent cliff, Teva seems like a wonderful blend of growth and value that will also kick in a dividend north of 2%.

Silver Wheaton (NYS: SLW)

Just as was the case with Teva, Silver Wheaton's dividend may not be all that much to look at now, but its chances to grow look phenomenal. Having initiated a dividend last year, Silver Wheaton has benefited from the higher spot price of silver. The company resells silver and has long-term contracts in place that fix its costs to just above $4 per ounce. This means that anything over $4 on silver is almost pure profit for the company. While I wouldn't call silver a hedge metal against a weaker dollar, its practical uses are much more than that of its yellow counterpart, gold. I'm looking for Silver Wheaton's dividend to jump dramatically from its current 1.2% in the next few years.

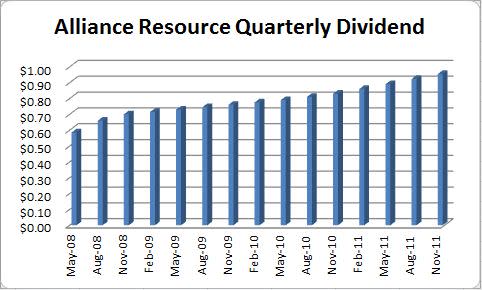

Alliance Resource Partners (NAS: ARLP)

I know I've beaten the dead horse and then some on Alliance Resource Partners over the past year, but the stock hasn't let me, or investors, down. Alliance Resource, which produces and markets coal to utilities for energy production, has recorded 11 straight years of record profits and has been no stranger to my quarterly Dividend Champions list. In fact, Alliance Resource has raised its dividend an unbelievable 14 consecutive quarters and has boosted its dividend annually by an average of 13.8% since 2006.

Source: Dividata.

Currently yielding 5.1%, this company will give me energy exposure as well as a rock-solid dividend and the chance for my stock to appreciate in value.

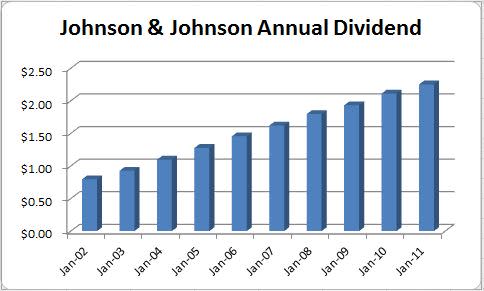

Johnson & Johnson (NYS: JNJ)

Go ahead and formulate an argument against owning a company that has grown its adjusted earnings for 27 consecutive years and has raised its dividend every year for the past 49 years... I dare you!

Source: Dividata.

Johnson & Johnson isn't going to provide the same earnings pop I often yearned for in small-cap companies, but its solid portfolio of health-care products is unparalleled. It's a name almost interchangeable with Procter & Gamble, but given J&J's slightly lower forward earnings multiple and marginally higher dividend yield of 3.5%, I'm more inclined to want J&J in my portfolio.

Foolish roundup

All that's left is to answer my own call to action. Within the next few weeks or months I will begin littering my portfolio with dividend-paying companies with the idea of both stabilizing my high-beta portfolio and adding what is essentially free money to my bottom line. This is the year I keep my promise to invest in myself.

What are you doing to pay yourself back in 2012? Share your thoughts in the comments section below. Also, consider downloading a copy of our special report "11 Rock-Solid Dividend Stocks" in which our top-notch team of analysts has identified companies that could earn you money no matter which way the market heads in 2012. Best of all, this report is completely free, so don't miss out!

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. While this may not be the "Summer of George," it is the "year of the dividend." You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool owns shares of Teva Pharmaceutical, Annaly Capital Management, and Johnson & Johnson.Motley Fool newsletter serviceshave recommended buying shares of Alliance Resource Partners, Annaly Capital Management, Procter & Gamble, and Johnson & Johnson, as well as creating a diagonal call position in Johnson & Johnson. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policythat divvies out the truth daily.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.