Seeds of a New Boom for Stocks?

Floyd Norris of TheNew York Times has an interesting article out this week detailing a clear cycle in the history of our stock market. Normally, assuming market cycles are meaningful or predictive of the future is a fool's game -- most of what we think are patterns are just coincidences of randomness. This one, however, makes sense, and investors should pay attention to it.

As Norris explains, for the past half-century the market has moved in 15-year cycles where returns swing from spectacular to near-zero. In 1964, the average real return over the preceding 15 years was a stellar 15.6% a year. Then it flipped. By 1979, the previous 15 years produced a negative real return. Then it flipped again. By the late 1990s, 15-year average returns were near record highs. And again: As of the end of last year, stocks returned a measly 3% a year over the last 15 years.

The trend is clear: After booms come busts, and after busts come booms. And that doesn't happen overnight. These cycles tend to last over a decade.

That bodes ill for stocks, Norris writes. "If past is prologue, the 15-year return is likely to continue to decline and to turn negative in about four years. That does not necessarily imply that stocks will fall during that period, since that could happen with small gains over the period."

That's one way to look at it. Another is the realization that, after more than a decade of negative real returns, there's a decent chance that we're fairly close to the beginning of a new bull cycle.

Sound crazy? It sounded crazy in the early 1980s, too. So did the notion 10 years ago that we were about to face a decade of stagnation. So did the idea in 2006 that home prices were about to fall by half. As did the idea in 2009 that stocks were about to double.

That's always how these things work. The tide turns when everyone least expects it. The more obvious the market's direction seems, the greater the odds that you're wrong.

One thing is certain: We are exactly 10 years closer to the next bull market today than we were 10 years ago.

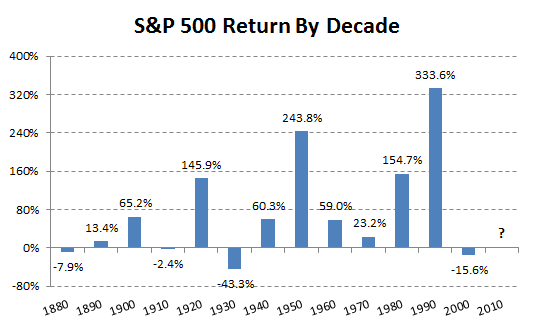

Here's how this looks historically:

Sources: Yale University and author's calculations.

After booms come busts, and after busts come booms. Happens over and over.

Going back to 1820, stocks have never produced two consecutive decades of real losses. After a decade of losses (like we just experienced), the worst subsequent 10-year return we've seen is about 12% a year. That's a hefty return by any measure.

Of course, history isn't guaranteed to repeat itself. And what drives stocks to a decade of low or high returns isn't the calendar; it's valuations. Stocks do well after they're cheap, and poorly after they're expensive. So the real question shouldn't be how long stocks have been stagnant, but whether they're cheap.

That's a matter of constant debate. I recently interviewed two heavyweights in the finance field: Wharton professor Jeremy Siegel and Yale professor Robert Shiller. Siegel thinks stocks are undervalued by as much as 25%, and priced to set investors up for a boom going forward. He cites below-average P/E ratios, low interest rates, and an economy that's stronger than most give credit. Fears that corporate earnings are in danger of falling are overblown, he says. The fact that U.S. corporations do more of their business overseas lowers the odds of a lasting earnings bust -- business is more diverse than it was in the past.

"I think stocks are going to beat their historical average" going forward, Siegel told me. "Their historical average returns are between 6% and 7% per year after inflation. I think we are looking actually at probably 8% to 9% per year after inflation over the next five years, 10 years."

Robert Shiller isn't so sure. His metric, a P/E ratio using an average of 10 years' earnings, show stocks might be a little overvalued. Earnings also look unsustainably high in his view, though he's somewhat sympathetic to the idea that investors are suffering from pessimism. "I would say in some senses we do have too much pessimism right now; in other senses, no. I mean, the stock market only briefly in 2009 got below its historical average price/earnings ratio. Now it's kind of high," he said.

But when I asked Shiller about another topic -- gold -- he mentioned something that seems particularly relevant to the stock market today: "I think when you look at history and a broad set of facts to make judgments about speculative assets, you also have to correct for your natural biases. You have to think that I am likely to overreact to a decade of price increases and become too optimistic."

And concurrently, you have to think that you're likely to react to a decade of price decreases in the stock market and become too pessimistic.

Whether stocks will have a great decade, no one knows. Anything could happen. I happen to think the odds are decent that they will; others think the opposite. That's what makes a market.

What about you?

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.

At the time thisarticle was published

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.