2 Bold Predictions for 2012

Around this time of the year, predictions are a dime a dozen. Everyone has their best stock pick of the year lined up and thinks they have uncovered the next get-rich-quick scheme that will lead them to the promised land.

Fortunately for you, I've never been good at taking the easy route. Instead, I'm going to look at two completely outside-the-box predictions that I feel very confident about heading into 2012. I'm fully ready to accept my lashings on Dec. 31 if these turn out to be wrong, but let's just say that the odds aren't in my favor from the start.

Prediction 1: Large-cap stocks will outperform small-cap stocks

You might be thinking, "So what, this isn't exactly what I'd call a bold prediction!" I assure you, given that small caps have outperformed large-cap stocks in nine of the past 11 years, this is a prediction in which the odds are clearly not in my favor.

Small-cap companies hold an edge over their larger counterparts because they often boast much faster growth rates and can double their revenue a whole lot easier than a large-cap company can. They also act as a psychological lure to investors since many are drawn to the trend of past returns -- and in this case it's a rich history of small caps outperforming large caps. But that trend looks to change in 2012 by my estimation.

For starters, large-cap companies are significantly cheaper on an earnings basis than their usually faster-growing small-cap counterparts. Normally, pundits would compare the S&P 500 to the Russell 2000 to get a gauge of price-to-earnings ratios. As for me, I prefer to use the Vanguard Large-Cap ETF (NYS: VV) , which attempts to mirror the MSCI U.S. Prime Market 750 Index of primarily large-cap companies, and the Vanguard Small-Cap ETF, which attempts to track the returns of the MSCI U.S. Small-Cap 1750 Index. On a trailing-12-month basis, the large-cap ETF boasts a P/E of 12 versus the small-cap ETF at 14.

An even bigger difference from a percentage basis is seen when comparing the yields of these two ETFs. As should be no surprise, small-cap companies have less capital to work with since they're constantly reinvesting their capital into their business. Less cash on hand often means little chance for a dividend. Large caps, on the other hand, have well-established businesses and often lure investors into purchasing their stock by sporting stable, yet high-powered, dividends. Once again, using our Vanguard example, the large-cap ETF boasts a 1.90% to 1.20% yield edge over the small-cap ETF.

With many expecting volatility to continue in 2012, low-beta, high-yielding large caps are likely going to be where investors park their money.

Prediction 2: U.S. money center banks will be the best performing sector in 2012

Yes, even with Europe near a complete debt meltdown, China's growth showing visible signs of slowing, and the U.S. economy sputtering in neutral, I'm choosing financials -- predominantly U.S. money center banks -- as the best performing sector in 2012.

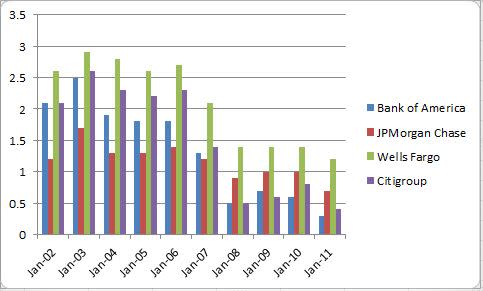

This time I will beat the dead horse and point out that relative to book value, U.S. money center banks Bank of America (NYS: BAC) , Wells Fargo (NYS: WFC) , JPMorgan Chase (NYS: JPM) , and Citigroup (NYS: C) are trading at their lowest valuations in a decade.

Source: Morningstar.

Not even during the heights of the credit crisis did banking stocks see their valuations dip as much as they have in recent years -- yet oddly enough, bank liquidity is at its highest levels in near-term memory. Bank of America sold off much of its stake in China Construction Bank in order to boost its tier-1 common equity ratio to 8.65%. Its peers boast even higher tier-1 common ratios. JPMorgan Chase at 9.9% and Wells Fargo at 9.35% are so well-capitalized that both boosted their dividends earlier in the year. Citigroup is actually the best capitalized of the bunch with a tier-1 common equity ratio of 11.7%.

Another common misconception is that U.S. banks wouldn't be able to stand up to the shock of a European meltdown. Bank of America withstood a huge $8.8 billion loss in 2011 related to legal settlements in its mortgage division -- chances are it would survive the $1.5 billion it currently has in exposure to Italy. JPMorgan Chase is in considerably better financial shape than Bank of America and even it, on a comparative basis, is only claiming $6.3 billion in exposure to Italy.

Fear-mongering can be a scary thing, and it ran full force throughout the banking sector in 2011. With these four banks now trading at minuscule forward P/E ratios ranging from six to nine, there is very little worry left to squeeze out of this sector. You know the old phrase "You can't get blood from a turnip"? Well this is it in action. Mark my words, U.S. money center banks will be the best performing sector come year end.

Foolish roundup

There you have it, folks -- two calls that will either make me look like a prince or a pauper. The odds are already stacked against me, so I'm going to need calmer heads to prevail and a little bit of luck to be correct.

What's your take on my two predictions? Share your thoughts in the comments section below.

Also, if you're looking for one more great prediction heading into 2012, consider downloading your copy of our latest special report, "The Motley Fool's Top Stocks for 2012," in which our chief investment officer reveals his top play which has been dubbed the "Costco of Latin America."

At the time thisarticle was published Fool contributor Sean Williams owns shares of Bank of America, but has no material interest in any other companies mentioned in this article. He absolutely loves betting on an underdog. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Citigroup, Bank of America, Wells Fargo, and JPMorgan Chase, and has created a covered strangle position on Wells Fargo. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that'll make you a winner whether heads or tails comes up.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.