Our Top 5 Energy Stocks For 2012: Ultra Petroleum

This article is part of Our Top 5 Energy Stocks for 2012 series.

Earlier this year I revealed my secret to commodities investing:

The time to own commodities is when they are down, when everybody has lost money in them, and when they trade below the cost of production.

When a commodity is unprofitable for the companies that make it, high-cost producers die off or halt operations. The industry shrinks, leaving only the most efficient firms. This time is marked by large amounts of turmoil, falling stock prices, and occasionally bankruptcies before supplies decline and prices rise again.

Where's the opportunity now?

Natural gas.

And what's the best natural gas stock for 2012?

Ultra Petroleum (NYS: UPL) . Read on and I'll explain why.

NatGas!

In the past few years, new technologies and cheaper costs have allowed producers to access gas trapped in parts of the U.S. previously considered unreachable. As more companies have tapped these unconventional plays, U.S. natural gas production has risen just over 20% in the past five years, to 79 billion cubic feet per day. Experts expect production to keep rising over the next 25 years, to 113 Bcfd by 2035.

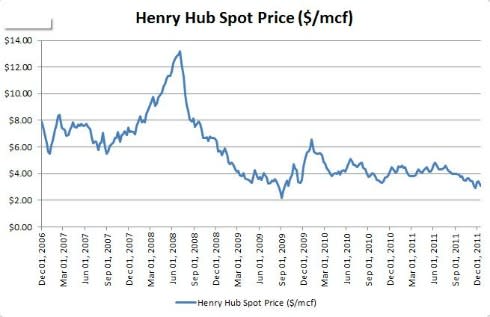

Prices continuing to sink

The quickly increasing production with slowly increasing demand has pushed down prices to near-record lows. With the industry average production cost at $5 to $6 per mcf, producers are getting crushed.

Source: EIA.

At current prices of just over $3 per mcf, high-cost producers are going to have trouble staying in the game. Ultra Petroleum, however, is one of the lowest-cost producers there is.

Low-cost producer

Ultra has operations in Wyoming's Green River Basin and Pennsylvania's Marcellus Shale. The company has so far only developed 6% of its proven reserves and yet it produced a record 63.4 billion cubic feet equivalent of natural gas in the third quarter, a 14% increase in production year over year.

While the industry's average costs are $5-$6 per mcf, in the most recent quarter Ultra's costs were $2.78 per mcf, and over the past nine months the company's costs were $2.82 per mcf. Even with the low prices of the past few months, due to hedging and its low costs, Ultra reported in its most recent quarter $150 million in earnings, a 74% cash flow margin, 32% return on equity, and a 14% return on capital. The company has hedged out roughly 50% of its production for 2012, so the positive results should continue for next year, especially with the company's low costs.

At a market cap of $4.5 billion, you're getting the company for roughly 10 times last year's earnings. Assuming a price of $4, the PV-10 of its proved reserves was $5 billion; at $5, it's $8.7 billion; and at $6, it's $11.6 billion. So for Ultra to be a big winner, the price of natural gas needs to turn around or the company needs to be bought out. I think prices will turn around, and here's why.

Production will slow

If something is unsustainable, it will stop. With the price of natural gas where it is and the level of production in the U.S. where it is, it is unsustainable. Research from ARC Financial shows that the top publicly traded producers of natural gas need approximately $22 billion per quarter to maintain their current capital expenditure levels. The problem, however, is that the industry currently only produces roughly $12 billion in cash flow from their production. That means $10 billion per quarter has to come from outside the industry.

Chesapeake Energy (NYS: CHK) is one of the firms that has been using creative financing, joint ventures, and asset sales to fund its capital needs. SandRidge is following a similar strategy with its spinoffs of royalty trusts SandRidge Mississippian Trust (NYS: SDT) and SandRidge Permian Trust (NYS: PER) . This can only go on for so long, however. While large producers have the assets to do such things, smaller producers aren't in such a good position. Natural gas production will have to slow at some point soon.

Demand will rise

The other part of the picture is demand. Natural gas and oil are equivalent on roughly a 6 to 1 ratio, meaning 6 mcf of gas per barrel of oil. In a perfect world, oil and natural gas would trade on a 6 to 1 ratio, however the historical ratio is closer to 10 to 1. Currently, the ratio is just over 30 to 1! The low price of natural gas relative to oil in the U.S. is a huge incentive for companies to switch their feedstocks to natural gas.

Until projects like Cheniere Energy's (NYS: LNG) Sabine Pass export terminal are completed in 2015, natural gas produced in North America has to be used in North America. Even when the terminal and others like it are completed, only a small percent of natural gas in North America can be exported.

Many companies see opportunity with low natural gas prices and plentiful supply. Clean Energy Fuels (NAS: CLNE) , with support from Chesapeake Energy, is building out a network of natural gas fueling stations across the country for trucks. Westport Innovations (NAS: WPRT) manufactures natural gas engines for trucks and other large vehicles. Besides a joint venture with Cummins, the company has been striking partnerships with major companies such as Caterpillar and General Motors to incorporate its technology into vehicles they are developing. As demand for gas among industrial users rises, the price of natural gas should also rise.

Foolish bottom line

When looking to invest in a commodity, you are best off investing in the lowest-cost producer. Focus on commodities trading below the cost of production, and over time you should be duly rewarded.

I think Ultra Petroleum is a great pick for the future, but our analysts have selected a different stock that they believe is poised for tremendous growth in 2012. Find out which company in our new free report: "The Motley Fool's Top Stock for 2012." Thousands have already requested access and it'll only be available for a limited time. Simply click here --it's free.

At the time thisarticle was published

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.