Xerox's Dividend X-ray

Not all dividends are created equal. Here, we'll do a top-to-bottom analysis of a given company to understand the quality of its dividend and how that's changed over the past five years.

The company we're looking at today is Xerox (NYS: XRX) , which yields 0.8%.

Industry

While Xerox is still known as a hardware company that competes with Eastman Kodak (NYS: EK) in printers, the company has been transitioning to a document services and processing company, which is the realm of Accenture and Genpact. The services business is more specialized than printers and, as such, has higher margins. This shift from hardware to services is similar to Dell's (NAS: DELL) move after founder Michael Dell returned to the company.

Xerox Corporation Total Return Price Chart by YCharts.

Dividend

To evaluate the quality of a dividend, the first thing to consider is whether the company has paid a dividend consistently over the past five years, and, if so, how much has it grown.

Xerox Corporation Dividend Chart by YCharts.

Xerox's dividend has remained flat at $0.04 per quarter since it was first initiated at the end of 2007.

Immediate safety

To understand how safe a dividend is, we use three crucial tools, the first of which is:

The interest coverage ratio, or the number of times interest is earned, which is calculated by earnings before interest and taxes, divided by interest expense. The interest coverage ratio measures a company's ability to pay the interest on its debt. A ratio less than 1.5 is questionable; a number less than 1 means the company is not bringing in enough money to cover its interest expenses.

Xerox Corporation Times Interest Earned TTM Chart by YCharts.

Xerox covers every $1 in interest expense with $9 in operating earnings.

Sustainability

The other tools we use to evaluate how safe a dividend is are:

The EPS payout ratio, or dividends per share divided by earnings per share. The EPS payout ratio measures the percentage of earnings that go toward paying the dividend. A ratio greater than 80% is worrisome.

The FCF payout ratio, or dividends per share divided by free cash flow per share. Earnings alone don't always paint a complete picture of a business's health. The FCF payout ratio measures the percent of free cash flow devoted toward paying the dividend. Again, a ratio greater than 80% could be a red flag.

Source: S&P Capital IQ.

Xerox has historically had low payout ratios, and they have recently been trending even lower.

Alternatives

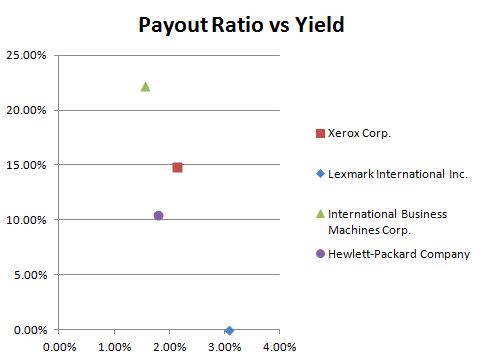

Source: S&P Capital IQ.

There are some alternatives out there in the industry. Of Xerox's peers, Lexmark (NYS: LXK) has the highest yield at 3.1%; however, it has a negative free cash flow payout ratio. IBM (NYS: IBM) has a slightly lower yield than Xerox at 1.6% and comes with a high payout ratio. Hewlett-Packard (NYS: HP) has a 1.8% yield and a 10% payout ratio

Another tool for better investing

Most investors don't keep tabs on their companies. That's a mistake. If you take the time to read past the headlines and crack a filing now and then, you're in a much better position to spot potential trouble early. We can help you keep tabs on your companies with My Watchlist, our free, personalized stock-tracking service.

Add Xerox to My Watchlist.

For more dividend stock ideas, click here to get The Motley Fool's free report: "11 Rock-Solid Dividend Stocks."

At the time thisarticle was published Follow Dan Dzombak on Twitter at @DanDzombak to check out his musings and see what articles he finds interesting. The Motley Fool owns shares of International Business Machines. Motley Fool newsletter services have recommended buying shares of Accenture and Dell. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.