The Race to the $1,000 Genome

Have you ever been introduced to the Law of Accelerating Returns? It's the reason your cell phone is cheaper, more powerful, and much smaller than the desktop computer you were using less than a decade ago. It's also the reason why many medical technologies are far more precise at lower cost than they were a decade ago. But what happens when progress is so rapid that the law gets left behind? For biotech investors (not to mention patients), the answer is more complex -- and potentially transformative -- than it may seem at first glance.

Genetic rocket

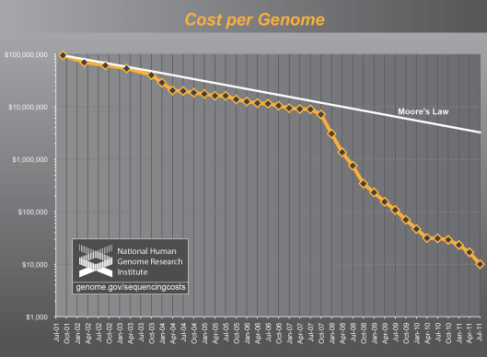

Genome sequencing capabilities have exceeded most researchers' wildest expectations. Just as the costs of processing power decrease at an exponential rate under the Law of Accelerating Returns, so too should the cost of genetic analysis continue to drop. After all, what is genetic analysis if not a unique application of computing power? However, scientists at the National Human Genome Research Institute found that genome sequencing costs began to decouple from the law in 2008:

Source: National Human Genome Research Institute.

Going to ludicrous speed

The exponential trend of Moore's Law (the Law of Accelerating Returns covers and expands on this law) would have offered genome sequencing for several million dollars this summer. Instead, costs have declined to $10,000 and show little signs of slowing.

At such a pace, $1,000 genomes could follow very closely on the heels of $1,000 exomes. If cost declines continue at their post-2008 pace, the data projects that costs will drop below $1,000 for full human genome sequencing at the start of 2013. A more conservative average of all progress since 2001 only pushes that milestone back by another year.

Squeezed at the margins?

It's incredible progress at an incredible pace, but does it mean great things for the companies driving this process? Possibly, but many may not make it. Most of the smaller players in genetic testing and analysis occupy niches that have yet to prove consistently -- or even potentially -- profitable. Genetic Technologies (NAS: GENE) is only marginally profitable after a decade of red ink, and Exact Sciences (NAS: EXAS) has a decade of development behind it that's yet to produce anything positive on the bottom line. When full-genome sequencing becomes a worthwhile option, it stands to reason that doctors and patients would opt for more information rather than isolated genetic markers.

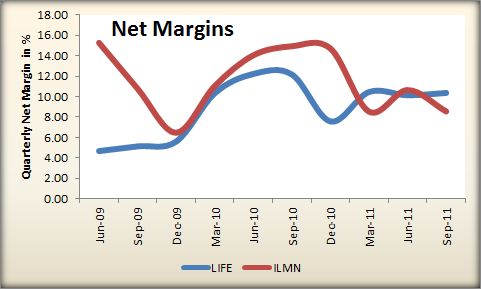

Life Technologies (NAS: LIFE) and Illumina (NAS: ILMN) , as two of the largest players in the genome-sequencing game, offer better alternatives for continued success:

Sources: Morningstar, corporate quarterly reports, and author's calculations.

Two worrisome trends lie in the sudden drop in Illumina's revenue growth and the virtual flatlining of Life Technologies' revenue over the past two years. Despite these drawbacks, Life Technologies appears to have a slight edge when both companies' profit margins are compared over the same period:

Sources: Morningstar, corporate quarterly reports, and author's calculations.

Illumina's erratic margin, while consistently positive, seems less reassuring than the more moderate -- but improving -- trend seen at Life Technologies. Illumina's lowered expectations for the upcoming year (and subsequent price drop) could herald further weakening, but it may also present an attractive purchase price should the company reach a much broader audience in coming years.

Cues from chipmakers

As with all technological manufacturing, economies of scale and sustained R&D spending can help build a long-term competitive advantage. A reasonable comparison might be the microprocessor industry. Intel has ruled that roost for years, in part by regularly spending as much on R&D as rival AMD earns in annual revenue.

That's a silver lining for Illumina, as it's managed to sustain an R&D ratio nearly twice as high as Life Technologies' while maintaining similar levels of profitability. Whether this will hold true two or three years from now is a matter of debate. A health-care market that offers regular genetic analysis will look quite a bit different than one in which the procedure is rare, which makes long-term projections nearly impossible. I do see promise in both companies and have bullish CAPScalls on both, which I hope to maintain beyond the dawn of $1,000 genomes.

A helping hand for niche drugmakers

Beneficiaries of affordable genome sequencing are certain to include patients of all shapes and sizes. Those with uncommon illnesses could benefit the most, as could the companies that develop cures for those illnesses.

Cancer, for example, is notoriously shifty and difficult to eradicate. What works for lung cancer may prove useless for prostate cancer, and the sum of these frustrating factors is often a costly drug that only works on specific forms of a disease. Dendreon (NAS: DNDN) and Ariad Pharmaceuticals (NAS: ARIA) each have a unique approach to cancer treatment -- Dendreon stimulates the immune system, and Ariad attacks aggressive cancers with small-molecule drugs.

Both companies show promise, but have been marked as risky investments in the recent past. Biotech Fool Brian Orelli dinged Dendreon for its high-cost treatment and reimbursement risks. Ariad's unproven drug portfolio and cash-burning ways got it poor marks from Fool contributor Sean Williams. However, both approaches could benefit from inexpensive genetic analysis, which ought to produce a more effective and more affordable treatment, not to mention a higher stock price.

The quest for knowledge

Without a deeper understanding of what the genome and its markers mean, no amount of cost reduction will make treatment more targeted or effective. Despite knowing many Alzheimer's biomarkers, scientists still struggle with effective diagnostics and treatments. That may be why Elan (NYS: ELN) sold off much of its stake in key Alzheimer's drugs this year. It retains much control over multiple sclerosis drug Tysabri, which makes sense in the short term as MS appears to be better-understood from a genetic standpoint.

Greater processing power will help scientists unlock the genome's secrets, but real breakthroughs are likely to come once truly effective analytical programs come online. Luckily, algorithms are also improving at radical speed, in many cases outpacing improvements in hardware over time. It might not be long before we finally master the genome. It might even happen by 2016, when full-genome sequencing costs could drop under an even more radical barrier -- $100.

If you're looking for a different play on this technological revolution, take a look at The Motley Fool's free report on one stock that's poised to profit from a worldwide flood of data. Understanding the genome and making drugs that work with it will take a huge amount of data analysis, and the company in our report knows the right way to do it. Thousands have discovered this secret, so get your free copy today.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter for more news and insights. The Motley Fool owns shares of Dendreon and Intel. The Fool owns shares of and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of Elan, Intel, and Illumina. Motley Fool newsletter services have recommended creating a bull call spread position in Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.