Why I'm Holding This Volatile Company's Shares in 2012

I've been watching Travelzoo (NAS: TZOO) like a hawk since it popped on my radar back in April. There's a lot of risk involved in owning the company, but on the flip side, outsized rewards can be had as well. As a Travelzoo shareholder myself, I want to let you know exactly how I'll be approaching the company in the coming year.

Never heard of Travelzoo?

If you've never heard of Travelzoo before, or only vaguely know what it does, you're not alone. For well over a year, I saw the company repeatedly show up on my screens, and assumed it was a basic travel search engine, akin to Orbitz (NYS: OWW) , Expedia (NAS: EXPE) or even name-your-price specialist priceline.com (NAS: PCLN) .

In reality, nothing could be further from the truth. Instead, Travelzoo is a two-headed monster trying to conquer the complementary fields of global travel and local deals. At its roots, the company started out focusing on the former, working with travel companies since the late 1990s to put together tailored deals and then charging the companies for posting the deals on its website.

In August 2010, Travelzoo expanded into the latter field: local deals. You'd probably recognize the space as being dominated by recent IPOGroupon (NAS: GRPN) , and Amazon (NAS: AMZN) -backed LivingSocial. Where Travelzoo tries to differentiate itself from these two is by offering just two, high-quality local deals per market per week.

The bulls' case

The numbers that Travelzoo has been putting up since delving into local deals have been nothing short of fantastic. While the most recent earnings report showed impressive growth of both revenue and earnings per share -- which were up 40% and 62%, respectively -- it's the larger long-term trends that have me excited.

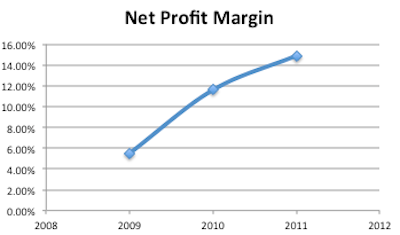

Since selling off its Asia/Pacific division in 2009, take a look at how net profit margins have been expanding.

Source: SEC filings. 2011 figures for the last nine months. 2011 results are normalized to exclude a one-time settlement with the State of Delaware for $20 million.

While Travelzoo was keeping less than $0.06 of every dollar it took in 2009, it's now retaining more than double that amount just two years later.

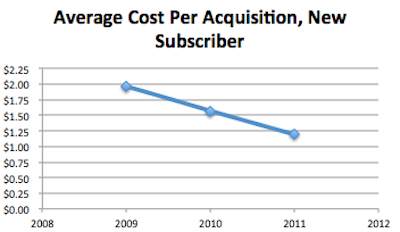

Furthermore, the company seems to be approaching a tipping point domestically, as word of mouth is fueling subscriber growth and as the costs to acquire new members shrinks.

Source: SEC filings. 2011 figures for the last nine months.

Furthermore, management has shown it knows how to enhance shareholder value wisely. Netflix (NAS: NFLX) could learn a thing or two from how Travelzoo chose to pursue its share buybacks.

While management was authorized to buy back up to 500,000 shares, it was slow to pull the trigger when the stock's price hovered around $100 and was able to buy them all for the much-more-reasonable price of about $30 per share.

With a forward price-to-earnings ratio of just 14.9, an investor could be forgiven for seeing nothing but upside at today's prices.

The bears' case

Despite the rosy outlook, things started going south with the announcement of second-quarter earnings this summer that missed expectations. And though Travelzoo has already seen its shares plunge once this year, short-sellers still think there's a ways to go, as the percentage of shares sold short is through the roof.

I would contend that the second-quarter miss was due to two things. First, the company was hiring record numbers of Local Deals employees who were still being trained when the quarter ended -- and thus, producing no revenue.

Furthermore, the new cost structure associated with Local Deals is different than the legacy travel business. With its travel program, Travelzoo was paid directly by travel companies. With Local Deals, Travelzoo takes payments directly from consumers, and there are a number of charges I believe analysts didn't factor in when setting their expectations, which helped push shares to nosebleed valuations.

But where the bears could really have a point is in questioning just how large the Local Deals market is and how large a moat Travelzoo could really have. Travelzoo claims that if it can tap into 200 local markets and offer two quality deals per week in those markets, it could represent a $780 million opportunity.

This is what causes me to pause. I go to the company's website a couple of times per week and check out all of the Local Deals pages. While I think it's more than reasonable to see the company hitting its goals in cities along the West Coast, in Florida, and in certain areas of the Northeast, I'm having trouble believing -- based on the frequency of deals being posted -- that there are really 100, let alone 200, markets out there for this business model.

2012 and beyond!

I'm willing to give Travelzoo time to prove me that I'm wrong. At today's prices, I think the risk/reward trade-off is more than fair, and I'll be holding my shares I bought this year and leaving the green-thumb open on my CAPS profile . If you haven't bought in yet and are interested, today's prices would be a good entry point.

In the meantime, I'll be searching in other places to find my top stock for 2012. One of my candidates is actually featured in our newest special free report: "The Motley Fool's Top Stock for 2012." Inside the report, our analysts detail a company being called the "Costco of Latin America." I encourage you to get a copy of the report today; it's absolutely free!

At the time thisarticle was published Fool contributor Brian Stoffel owns shares of Travelzoo, Netflix, and Amazon. You can follow him on Twitter at @TMFStoffel. Motley Fool newsletter services have recommended buying shares of Netflix, Travelzoo, priceline.com, and Amazon.com. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.