State Street's Business Is Dull Compared to Other Banks, and That's Good

State Street Corp. (NYS: STT) emerged from Standard & Poor's recent round of bank downgrades as the smart kid who blew the curve, the only one of the big banks to maintain its credit rating (A+) under the agency's new formula. It probably won't be the last time State Street stands out as class pet in coming months.

The Boston-based holding company is expected to fly by the new stress tests regulators will use to evaluate bank health next year. That's a particularly important qualifier for investors because only the banks that ace the test will be allowed to raise dividends and initiate share buyback programs.

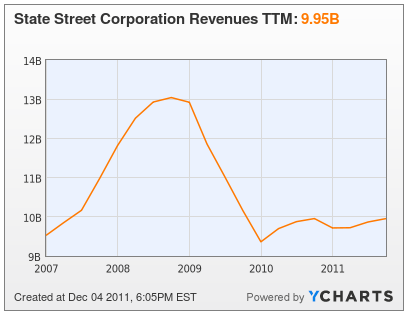

State Street also is forecast to show healthy gains in fee revenues as other banks outsource certain services to cut costs. As a custodian bank as well as traditional, State Street gets fees from other financial institutions and asset managers to manage investments and to perform back-office tasks. That income is particularly helpful in times like now when low interest rates -- the effective federal funds rate is at close to zero -- and low loan growth make profit growth from standard banking difficult. At Sept. 30, State Street had $22 trillion in assets under custody and administration and $1.9 trillion in assets under management. The company's fee revenues in the third quarter were up about 18% over the same period a year ago.

State Street Corporation Revenues TTM Chart by YCharts

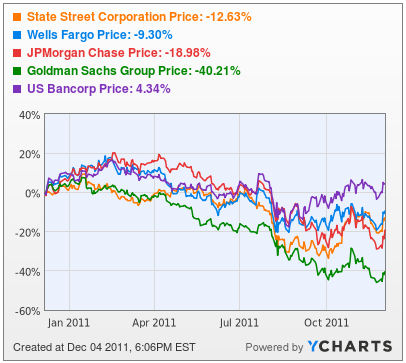

State Street's third-quarter results reignited investor interest in the company's shares, which had underperformed rivals in the sector for much of the past year. Here's a look at State Street shares next to those of a few stable competitors. (We've left out the more issue-ridden Bank of America (NYS: BAC) and Citigroup (NYS: C) on purpose.)

State Street Corporation Stock Chart by YCharts

Late November, downgrades on State Street shares by Morgan Stanley (NYS: MS) and SunTrust (NYS: STI) may yet affect its share price. Analysts at both companies cited concerns about State Street's net interest margins, a key measure of profitability for banks. That margin has been shrinking largely because State Street customers, like those of other banks, have been depositing money faster than the bank is lending it out. Lousy equity and bond markets also make investors worried about State Street earnings.

But State Street shares, like the shares of many banks these days, still look terribly cheap on traditional measures. State Street shares are selling for about 1.80 times its tangible book value, which is lower than they sold for during the worst of the recession. On a price-earnings basis, they're about the cost of a Wal-Mart (NYS: WMT) share.

State Street Corporation Price / Tangible Book Value Chart by YCharts

This for a 200-year-old company still paying a dividend with a current yield of 2%. YCharts Pro gives State Street strong marks for both fundamentals and share price value.

To be certain, market instability and economic uncertainty don't bode well for the share price of State Street or any other bank in the near future. But the problems seem survivable for a well-capitalized company turning out ample profits. When the market turns gloomy again, as it surely will at some point in coming months, it might be a good time to consider what State Street could be worth when the sun does shine again.

Dee Gill is an editor for the YCharts Pro Investor Service, which includes professional stock charts, stock ratings and portfolio strategies.

At the time thisarticle was published The Motley Fool owns shares of Citigroup, Wal-Mart Stores, and Bank of America. Motley Fool newsletter services have recommended buying shares of Wal-Mart Stores. Motley Fool newsletter services have recommended creating a diagonal call position in Wal-Mart Stores. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.