3 Bargain Dividends Investors Should Buy Today

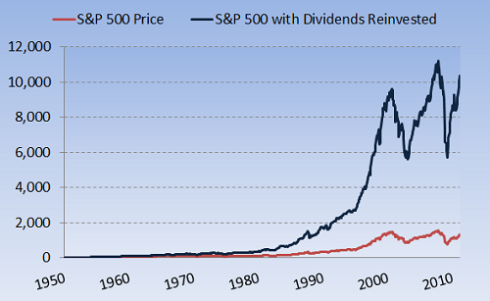

Investors should love dividends. I've applauded their value in the past, but rather than dive into why, this one simple graph should illustrate the key takeaway: Dividends are a catalyst for long-term wealth-building.

Source: Motley Fool staff's calculations.

Given how powerful dividends can be, picking up a high-yielding stock at a bargain is akin to finding an oilfield in your backyard, making you rich for years to come. Even after yesterday's nearly 3% run-up, the Dow Jones Industrial Average (INDEX: ^DJI) is still down almost 6% over the past month and more than 7% for the past six months.

Even the best stocks get dragged down in large market moves, so it's drops like this that get me excited about picking up high yielders on the cheap. But it's not just high yields that matter; otherwise, we'd all run out and buy Annaly Capital (NYS: NLY) , but since it's down more than 12% for the year, there must be more to it than that.

Health-care rock star

My first pick for a high-yield dividend bargain is Johnson & Johnson (NYS: JNJ) . The health-care giant yields an impressive 3.7%, well above the market average of 2%. You might be saying: "But aren't there cheaper stocks? What about the string of recent recalls? Aren't there better yields in this sector?" You'd be correct, somewhat. It's true that companies such as Abbott Labs and Merck edge out JNJ for dividend yield, but their P/E ratios are also higher. Eli Lilly is both cheaper and yields more, but it also has to worry about a looming patent cliff.

Instead, I like Johnson & Johnson because it's a model of stable shareholder returns. It has increased dividends consistently for 49 years, beating all but two companies in the Dow. And its recent Tylenol and Eprex recalls give investors a chance to benefit from others' overreaction. What's more, although consumers may know J&J as the maker of Tylenol and Band-Aids, the majority of its revenue comes from medical devices and diagnostics, meaning market reactions to consumer-facing products like this are usually overstated in terms of impact to the company. Johnson & Johnson also controls either the No. 1 or No. 2 spot for 70% of its products. That is brand strength you can bank on.

Furthermore, this product diversity helps insulate J&J from the depths of the patent cliff that threatens many of its competitors that rely on one or two blockbuster drugs. With a payout ratio at 54% (below the industry average of 69%), this $170 billion behemoth is likely to keep on rewarding shareholders above market rates for years to come.

Nerds rule

Have you heard the expression "Be nice to nerds, because one day you'll work for them"? That's not far from the truth, and Intel's (NAS: INTC) position of dominance shows why. Intel has consistently out-innovated smaller rival AMD (NYS: AMD) , effectively neutralizing most of its competition right there. As the world's largest semiconductor company, it has the money -- $15 billion in cash and short-term investments alone -- to continue delivering knock-out blows to the competition.

Compared with other chip makers such as NVIDIA (NAS: NVDA) , trading at a P/E of 14.1, Intel's 10.1 P/E is pretty darn cheap. And how about that dividend? Well, it pays out a hearty 3.7%, has a highly sustainable payout ratio of 32%, and has been raised pretty regularly. Quarterly payments are now $0.21 a share, up from their humble beginnings of $0.003 per share at the end of 1992.

Some people are quick to discount Intel as the phrase "death of the PC" becomes more popular. Although Intel has admittedly been absent in the mobile revolution, its processors are still in need in developing economies such as China, Indonesia, and India, where PC sales are still growing.

The Marlboro Man comes bearing gifts

A lot of people don't like to invest in "sin stocks" -- I understand that. If that's the case, take these previous two recs and forget this last one. For those of you who savor the consistent high yield, though, there is no better industry than tobacco. And inside this sector, there is no better play than Philip Morris (NYS: PM) . The cigarette maker, spun off from Altria (NYS: MO) in 2008, yields a solid 4.2% and has the ingredients of a long-term winner.

Despite the recent spinoff, this stock has been litmus-tested. Between 1957 and 2007, the company was the highest-returning stock in the United States. Had you invested $1,000 in Philip Morris in 1957, it would have been worth $5.8 million in mid-2008. With a payout ratio of 54.5%, Philip Morris also has the most conservative payout ratio of its tobacco peer group.

OK, so it's done well in the past, but what about going forward? Well, with the spinoff three years ago, Philip Morris now focuses internationally, while Altria has taken the domestic business. This international focus brings an unbelievable opportunity with a combination of lower litigation risk and higher smoking rates. Combine that with the Marlboro brand's strength, and you've got a winner.

The stock may not seem cheap, with its P/E of 15, but it's priced lower than other cigarette manufacturers (with the exception of Lorillard). A sector like this that throws off high dividends and is relatively recession-resistant rarely can be picked up any cheaper than this. It's also important to remember that with PM you're buying future growth, and with a five-year PEG ratio of 1.13, it leads the industry in affordability.

Takeaway

There you have it -- three great dividend stocks across three industries that are trading at relative bargains. Of course, there are other amazing dividend opportunities out there as well. If you're interested in discovering more, I invite you to take a look at The Motley Fool's special free report: "Secure Your Future With 11 Rock-Solid Dividend Stocks." In it you'll find 11 unbeatable dividends (including one listed here), and another throwing off an impressive 9% yield. The report is free, and you can access it now.

At the time thisarticle was published Austin Smith owns no shares of companies mentioned here The Motley Fool owns shares of Abbott Laboratories, Johnson & Johnson, Intel, Annaly Capital Management, Philip Morris International, and Altria Group and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of Philip Morris International, Johnson & Johnson, Intel, NVIDIA, and Abbott Laboratories, creating a bull call spread position in Intel, writing puts in NVIDIA, and creating a diagonal call position in Johnson & Johnson. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insightsmakes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.