Manitowoc's Dividend X-ray

Not all dividends are created equal. Here, we'll do a top-to-bottom analysis of a given company to understand the quality of its dividend and how that's changed over the past five years.

The company we're looking at today is Manitowoc (NYS: MTW) , which yields 0.8%.

Industry

Manitowoc is an equipment company that builds cranes and food service equipment. The large equipment industry has been firing on all cylinders recently, with Caterpillar (NYS: CAT) beating earnings estimates this past quarter and Terex's (NYS: TEX) cranes segment sales climbing 47.4% year over year. Longer-term, the industry is basically leveraged to the economy and went through a large bust in 2009 with the credit crisis. Only recently has demand from emerging markets pulled the company out.

Manitowoc Company Revenues TTM Chart by YCharts

Dividend

To evaluate the quality of a dividend, the first thing to consider is whether the company has paid a dividend consistently over the past five years, and if so, how much it has grown.

Manitowoc Company Dividend Chart by YCharts

Contrary to how it appears on the graph, Manitowoc's dividend has been flat since 2007. The company's dividend was $0.035 per quarter until 2007, when the company raised the dividend to $0.04 per quarter. Immediately after paying its only dividend of $0.04, the company split the shares 2:1. Starting in 2010, the company switched from quarterly dividends to an annual dividend of $0.08. The last was paid in December of last year, and the board recently declared the same dividend for this December.

Immediate safety

To understand how safe a dividend is, we use three crucial tools, the first of which is:

The interest coverage ratio or the number of times interest is earned, calculated by earnings before interest and taxes, divided by interest expense. The interest coverage ratio measures a company's ability to pay the interest on its debt. An interest coverage ratio less than 1.5 is questionable; a number less than 1 means that the company is not bringing in enough money to cover its interest expenses.

Manitowoc Company Times Interest Earned (TTM) Chart by YCharts

At 1.38, Manitowoc's interest coverage ratio is worrisome, though it has been rising steadily since mid-2010.

Sustainability

The other tools we use to evaluate how safe a dividend is:

The EPS payout ratio, or dividends per share divided by earnings per share. The EPS payout ratio measures the percentage of earnings that go toward paying the dividend. A ratio greater than 80% is worrisome.

The FCF payout ratio, or dividends per share divided by free cash flow per share. Earnings alone don't always paint a complete picture of a business's health. The FCF payout ratio measures the percent of free cash flow devoted toward paying the dividend. Again, a ratio greater than 80% could be a red flag.

Source: S&P Capital IQ.

Manitowoc has been unprofitable on an earnings basis since 2009, giving it a negative P/E payout ratio. During that time it has maintained positive free cash flow and a low free cash flow payout ratio, until the second quarter of this year when it began building inventory levels, reducing cash flow from operations.

Alternatives

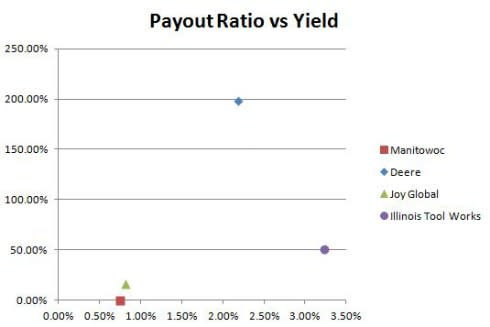

Source: S&P Capital IQ.

With negative payout ratios and a low yield, there are some alternatives out there in the industry. In the general equipment sector, Illinois Tool Works (NYS: ITW) has a yield of three times Manitowoc's at 3.25% and a payout ratio near 50%. Deere's (NYS: DE) yield is double Manitowoc's but its payout ratio is sky-high. Joy Global (NAS: JOYG) rounds out the list with a yield and payout ratio similar to Manitowoc's.

Another tool for better investing

Most investors don't keep tabs on their companies. That's a mistake. If you take the time to read past the headlines and crack a filing now and then, you're in a much better position to spot potential trouble early. We can help you keep tabs on your companies with My Watchlist, our free, personalized stock-tracking service.

Add Manitowoc to My Watchlist.

Add Deere to My Watchlist.

Add Joy Global to My Watchlist.

Add Illinois Tool Works to My Watchlist.

At the time thisarticle was published FollowDan Dzombakon Twitter at@DanDzombakto check out his musings and see what articles he finds interesting. The Motley Fool owns shares of Joy Global.Motley Fool newsletter serviceshave recommended buying shares of Illinois Tool Works. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.