Is ConocoPhillips' Business Creating Value?

Investors expect good returns. The more cash you get back for the amount you invested, the better your investment is. Same is true for the company you invest in. So, how do we find out whether a business is capable of generating superior returns?

The metric that matters: Return on invested capital

Growing bottom lines do not always guarantee good returns. More than earnings growth itself, it pays to find out how much has been invested into the business in order to generate that growth. This is where return on invested capital comes into play.

ROIC looks at earnings power relative to how much capital is tied up in a business. While a company's earnings may register growth, the return on invested capital might be declining. In other words, for every dollar of income generated, the company has to plough in more and more cash into the business over time. This is a warning sign. Unfortunately, investors fall into the trap of putting cash into companies that venture into less profitable projects. The result: It requires more cash for the company to generate the same returns.

Oil and gas companies have been through some tough times in the last five years. Volatility in energy prices has played a role in causing fluctuating bottom lines. But the fact is that these companies have sunk a lot of cash into investments by raising debt and by raising equity. Therefore, it makes more economic sense to find out whether these investments are generating returns that investors expect. Today, we will see how ConocoPhillips (NYS: COP) stacks up.

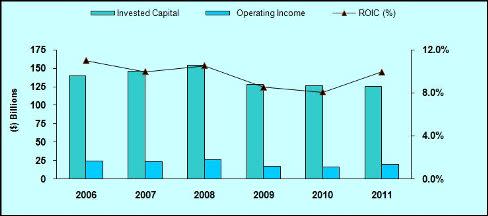

This is how invested capital, operating income and ROIC stack up for the past six years:

Source: S&P Capital IQ. ROIC is author's calculation. All data presented here is for a 12-month period, ending June 30 of the corresponding year.

Invested capital has been pretty much steady in the last five years except for a spike in 2008, while ROIC have been fluctuating. However, since 2010, returns have been encouraging with ROIC moving up to 9.9% from 8.1%. Projects are seeing returns.

Still, I'd keep my fingers crossed about what the outcome would be post spin-off of the refining arm next year. This could briefly push down returns, though in the long run, things should look good.

In terms of competition, this is how Conoco stacks up:

Company | Return on Invested Capital (TTM) | Return on Equity (TTM) |

|---|---|---|

ConocoPhillips | 9.9% | 17.0% |

(NYS: OXY) | 14.5% | 17.1% |

(NYS: CVX) | 13.4% | 21.3% |

(NYS: MRO) | 12.7% | 11.8% |

Source: S&P Capital IQ; ROIC is author's calculation; TTM = trailing 12 months.

Compared with its peers, Conoco's returns don't look too impressive. While the values aren't too bad, management could work harder to increase shareholder value.

What's the return compared to the cost?

Unfortunately, ROIC alone can't tell you how well a company is operating. Invested capital comes at a cost. Investors should check whether returns on invested capital exceed that cost. The weighted average cost of capital tells us exactly that since both debt and equity are used for financing operations. Debt-to-equity currently stands at 39.5%.

Conoco's after-tax interest expense, or cost of debt, stands at $654 million for the trailing-12-month period, which is a little more than 2% of its total debt. Expecting a 12% return from equity (beating the S&P 500's average 10% average historical return) is a fair expectation for this company given the risks involved in the shale plays and the natural gas market.

Using this data, WACC adds up to 9.3%. This is less than the ROIC of 9.9%, which is what I'm looking for. Conoco has been able to build on shareholder value. The company has been able to build on shareholder value by investing in projects whose current returns are higher than the rate investors expect.

Foolish bottom line

Exploration and production companies have sunk a lot of cash into investments during the past few years on which they are yet to fully realize gains. Still, investors can avoid possible pitfalls by finding out whether the company is capable of growing economically.

Add ConocoPhillips to My Watchlist.

At the time thisarticle was published Fool contributor Isac Simon does not own shares of any of the companies mentioned in this article. Motley Fool newsletter services have recommended buying shares of Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.