5 More Startling Figures That Should Have You Worried About Italy

Earlier, I started looking at 10 figures that investors should be taking note of in Italy. As we continue, we can note that lending rates have improved modestly from their multidecade highs last week, yet Italy is in no way out of the woods -- at least if these five remaining figures are any indication.

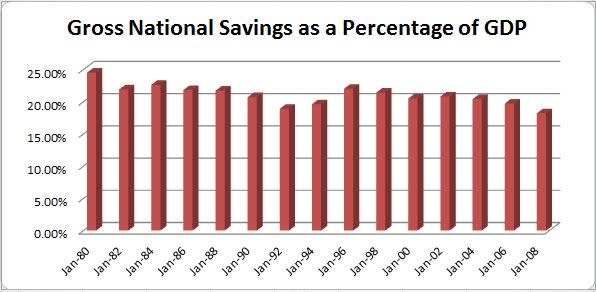

18.2%: Relative to the United States, Italy has always been heralded for the its citizens' ability to save money. Even though public debt has remained high for years, it was high personal savings rates that were expected to continue Italy's success and provide the fallback just in case things went sour. Unfortunately for Italy, its savings rate as a percentage of GDP has been dropping precipitously, from 24.5% in 1980 to 18.2%, -- a 40-plus-year low.

Sources: TradingEconomics, World Bank.

Lower savings rates aren't an issue as long as consumers are spending and the economy is booming. Italy, however, is anything but a booming economy, with GDP growth currently around 1%. The government's recent approval of stricter austerity measures is sure to put a crimp on both workers' wages and GDP, making the drop in the national savings rate even more precarious.

29,066: No, this isn't the amount of times that former Italian Prime Minister Silvio Berlusconi has been accused of committing a crime or undergone a vote of confidence - that figure is coming later. This ominous figure is how many points Italy's version of the Dow has dropped since peaking in May 2007 at 44,364. Since then, Italy's primary stock index has lost 29,066 points, or 66% of its value. This figure goes hand in hand with the one regarding national savings and illustrates just how quickly billions of dollars in wealth have been destroyed with the credit crisis in 2008 and now the continuing sovereign-debt crisis in Europe. According to my calculations, Italians have $7.5 billion less in savings now than they did in 2007.

20%: Relative to the EU at an average of 50% of GDP, Italy's mortgage-lending market is minuscule at just 20% of GDP. But just because Italian banks have been frugal with their spending, that doesn't exactly mean the lending sector is free of risk. Between the banks' lending practices and restrictions imposed by Italy's constitution, the housing market looks like a pending disaster. Banks are reluctant to lend because, in the case of a default on the homeowner, it can take five to seven years before the bank legally takes possession of the property. "Why not rent?" you ask. Well, I mentioned Italy's constitution, which has strict rental controls in place that allow landlords to move rents higher by no more than 75% of the cost of living (i.e., the inflation rate) for up to eight years. It's no wonder that Unicredit, Italy's largest bank, announced this week that it's laying off 5,200 people by 2015.

7.9%: When talking about the health of a bank in the United States, you often hear about the tier 1 capital ratio, which measures how much core capital each bank has relative to its risk-weighted assets. In the United States, it's fairly common for banks to have double-digit tier 1 ratios. Barring a global meltdown, banks such as State Street (NYS: STT) , Bank of New York Mellon (NYS: BK) , First Republic Bank (NYS: FRC) , and Citigroup (NYS: C) -- with tier 1 capital ratios of 16%, 12.5%, 13.4%, and 11.7%, respectively -- would be just fine. Italy's banks, however, with their current 7.9% bank capital-to-assets ratio, may not fare as well. Although significantly improved from the less than 5% tier 1 capital Italian banks reported in 2007, non-performing loans relative to the total amount of outstanding loans are still hovering dangerously close to 5%. Even the worst U.S. banks rarely have non-performing assets as high as 5% of their loan portfolios. If Europe is relying on Italy's banking sector to support the crushing weight of the country's public debt, then they have placed their bets on the wrong horse.

54: Although this isn't directly tied to the economy, this is one of those figures that just makes you want to bang your head against the wall in disbelief. The now-former prime minister of Italy, Silvio Berlusconi, has faced 54, that's fifty-four, votes of confidence in Parliament just since 2008! Berlusconi single-handedly put laws in place granting himself immunity from concurrent court cases that alleged him of wrongdoing in 2008 and again faced private-life scandals this past February. How someone so controversial could have remained in power for so long without any repercussions is beyond my comprehension. This is the final straw when it comes to Italy. Even though Berlusconi is gone now, the damage caused by his abuses of power lives on.

Well, there you have it, folks -- 10 figures that will certainly should make you think twice before throwing any of your hard-earned money Italy's way.

What's your take on Italy's precarious downfall? Is this simply a crisis of confidence, or do these figures tell a tale of woe that could affect all of Europe? Share your thoughts in the comments section below, and consider picking up your copy of our latest free report, "11 Rock-Solid Dividend Stocks," which may help shore up your portfolio in light of uncertain financial times.

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. He loves pizza but wants no part of the Italian pie that Europe's currently being served. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool owns shares of Citigroup.Motley Fool newsletter serviceshave recommended buying shares of Jeffries Group. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policythat's never afraid to give Italy the boot.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.