Will EU Taxes Send Machines After Your Stocks?

The EU's crusade against high-frequency trading continues apace. Austrian, Spanish, and Belgian finance ministers are increasingly agitating for a eurozone financial transactions tax. The tax, also favored by EU heavyweights France and Germany, proposes to tax stock and bond trades at a 0.1% rate. American politicians are getting in on the action as well, with two Democrats introducing a bill to tax financial transactions at a 0.03% rate.

The EU proposal stands a greater chance of passing, even considering the fragmented nature of its fragile political alliance. Proponents say it might raise up to $79 billion in new revenue each year, but the greatest flaw of this idea is its supporters' failure to understand that HFT trading systems have no need for national boundaries. Restrictive taxes in one region would only serve to concentrate HFT in more amenable markets, particularly U.S. exchanges.

Numbers don't lie

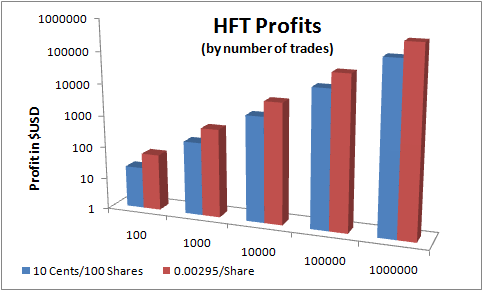

In order to find out how HFT endeavors might lose out under the new tax code, it's first necessary to pin down HFT's potential profits. The taxes proposed would be levied based on the value of the assets, so a transaction tax would come down on anyone buying or selling at the cost of the equities. But most HFT profits typically aren't calculated in terms of equity value; rather, they're based on sheer transaction volume. Both NYSE Euronext (NYS: NYX) and Nasdaq OMX (NAS: NDAQ) offer rebates for HFT activity, amounting to fractions of a cent per share moved, and other estimates of profitability are also available. With these numbers, we can begin to get a view of how HFT works.

Sources: Nasdaq OMX, The Wall Street Journal, and author's calculations. All trades are round trips (one buy plus one sell) and are assumed to be 100-share blocks.

Stock price doesn't matter in this chart. The trades could be done with penny stocks like Sirius XM (NAS: SIRI) or high-priced megacaps like Apple. Both companies have the characteristic heavy volume that can reveal stocks with high HFT activity, and as long as the HFT trader can cover the financing costs of its microsecond-length transactions, it makes about the same amount of profit whether each block of 100 shares is worth $175 or $40,000.

The hammer drops

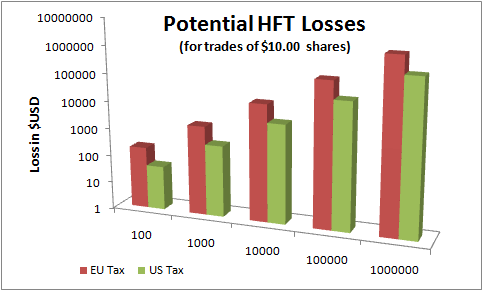

Here's where it gets interesting. The transaction tax, as previously mentioned, is levied on the value of the assets. As the calculation increases it becomes quite apparent that the more restrictive EU taxes would chase HFT out of the eurozone:

Sources: Nasdaq OMX, The Wall Street Journal, news reports, and author's calculations. All trades are round trips (one buy plus one sell) and are assumed to be 100-share blocks, and taxes are netted against $0.10/100 share profits.

These losses were calculated based on rebates at $0.10 per 100 shares. However, basing estimates on a $0.00295-per-share rebate also resulted in losses, although these were somewhat smaller.

Both tax laws, if implemented, would force HFT systems to operate in a narrow band of penny stocks. Even with the most generous per-share trade rebate, the EU tax would block any profit past the $3-per-share range, and U.S. proposals would cut off HFT around $10 per share. This is essentially the same as cutting off HFT entirely -- by my calculations, only the shares of Sirius XM, Sprint Nextel (NYS: S) , Alcatel-Lucent (NYS: ALU) , Chimera Investment (NYS: CIM) , Regions Financial (NYS: RF) , and few others would have the combination of volume and low price that would allow effective HFT operation.

Machinations against machines

But how likely is it that either will be implemented? American politics increasingly resembles a boxing match between armless participants, and any form of tax increase is likely to be rejected by the Republican-controlled House. If such a bill miraculously makes it to the White House, it's likely to be vetoed. President Obama favors a financial crisis responsibility fee, intended to zero out TARP losses by extracting payments from Wall Street firms at the heart of the crisis.

That leaves the EU. While Britain isn't likely to go along with such a tax, its refusal to participate in the euro means that its influence will be weak at best. The EU proposal will be debated next week in Brussels at a meeting of finance and economic ministers, many of whom have come out with public support for the plan. The Italian debt crisis isn't likely to sway regulators away -- the desperate need for cash is likely to add pressure to pass revenue-raising legislation.

A fool's (not a Fool's) errand

$79 billion in new tax revenue? Try zero. The only thing keeping HFT from leaving would be the ideal locations of companies' server farms, and equipment can always be shipped elsewhere. American exchanges have been aggressive in courting HFT operators with rebate schemes. This could result in American shores being invaded by hordes of machines, all hell-bent on one thing: squeezing every last fraction of a penny they possibly can out of the market.

If volatility keeps you up at night, it could get worse. And it could start making even less sense. Let's hope European regulators wake up and realize that taxes on globally active systems will only send those systems elsewhere, to everyone's detriment.

If you're looking for opportunities to escape machine manipulation, take a look at the Motley Fool's free special report on two small caps the government won't let fail. Get security through obscurity with government-supported companies that fly under the radar of most HFT systems. The report's only available for a short while, so get your copy today.

At the time thisarticle was published Fool contributor Alex Planes holds no stake in any company mentioned here. Add him on Google+ or follow him on Twitter for more insights and the occasional random link. The Motley Fool owns shares of Apple and Chimera Investment. Motley Fool newsletter services have recommended buying shares of Apple and NYSE Euronext, as well as creating a bull call spread position in Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.