A Brief History of Goldman Sachs' Returns

Despite constant attempts by analysts and the media to complicate the basics of investing, there are really only three ways a stock can create value for its shareholders:

Dividends.

Earnings growth.

Changes in valuation multiples.

In this series, we drill down on one company's returns to see how each of those three has played a role over the past decade. Step on up, Goldman Sachs (NYS: GS) .

Goldman shares returned 35% over the past decade. How'd they get there?

Dividends accounted for a decent part. Without dividends, shares returned 24% over the past 10 years.

Earnings growth was strong over the period. Goldman's normalized earnings per share grew by an average of 9% per year from 2001 until today. This might not be surprising to those who think of Goldman as the infamous "vampire squid wrapped around the face of humanity" capable of exploiting any and every economic condition, but it actually is surprising given the company's measly shareholder returns.

So if earnings were so strong, why were returns so low? This is why:

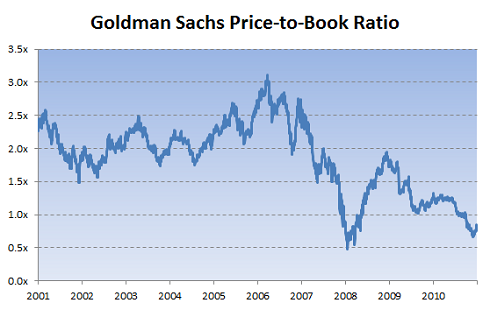

Source: S&P Capital IQ.

Goldman's price-to-book value has plunged over the past decade, and is now well below par.

Goldman isn't alone here. Other big banks like Bank of America (NYS: BAC) , Citigroup (NYS: C) , and Morgan Stanley (NYS: MS) all trade below book value as well. A lot of this can be blamed on ongoing woes in Europe -- after 2008, investors don't want to wait around to see who has the most toxic waste on their balance sheets, and so there's likely a "sell now, ask questions later" mentality in bank stocks that's hurting valuations. Once bitten, twice shy.

More broadly, I think there's a growing appreciation that the golden age in banking, which began in the early 1980s, may be coming to an end. Almost every global investment bank is laying off huge numbers of employees, trading revenues are dropping, returns on equity are falling, and regulations are rising. Valuations may be low for good reason.

Still, it's unlikely Goldman will trade below book value for long. Barring another global financial crisis or the need to raise capital (which can't be ruled out), shares will likely creep back above book value in the future. Don't expect shares to return to the glory days of trading at two or three times book value, but it's reasonable to expect expanding valuation multiples going forward -- the opposite of what shareholders have endured over the past decade.

Why is this stuff worth paying attention to? It's important to know not only how much a stock has returned, but where those returns came from. Sometimes earnings grow, but the market isn't willing to pay as much for those earnings. Sometimes earnings fall, but the market bids shares higher anyway. Sometimes both earnings and earnings multiples stay flat, but a company generates returns through dividends. Sometimes everything works together, and returns surge. Sometimes nothing works and they crash. All tell a different story about the state of a company. Not knowing why something happened can be just as dangerous as not knowing that something happened at all.

Add Goldman Sachs to My Watchlist.

At the time thisarticle was published

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.