Lots of Worry, Even More Opportunity

A group of Motley Fool analysts once discussed what we learned from the 2008-2009 financial crisis. One noted the difference between thinking you're a contrarian, and actually being a contrarian. All of us agreed on the adage of being greedy when others are fearful. That was our philosophy, our goal. But come 2008, many of us, myself included, were as fearful as everyone else. It was a sober reminder that by definition, not everyone can be a contrarian. That's why the few who actually can move against the herd end up so successful.

In hindsight, markets usually move in the opposite direction of sentiment. When the masses are bullish, future returns will be relatively low. When the masses are fearful, future returns will be relatively high. You never know how high or how low sentiment might go, or exactly when it will turn, but in a broad sense, the correlation between sentiment and future returns is one of the market's most dependable links. Have a look:

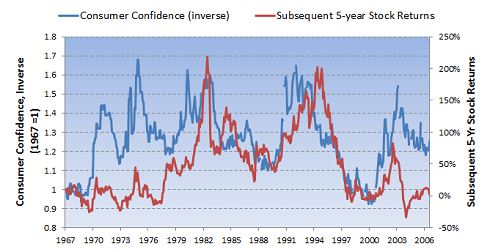

Sources: S&P Capital IQ, Yahoo! Finance, and author's calculations.

It may take a second to grasp what this chart shows, but bear with me. The blue line is the inverse of the Conference Board's consumer confidence index, so areas where the blue line is highest shows times when consumers were the glummest. The red line is subsequent five-year returns of the S&P 500 -- for example, the red line's value at the year 1970 is measuring stock returns from 1970-1975.

What this shows is fairly clear: When consumer confidence is low, ensuing stock returns are generally high, and vice versa. The correlation isn't perfect -- nothing is -- but it's strong given how random stock returns tend to be. Statistically, consumer confidence is actually a better predictor of future stock returns than the cyclically adjusted P/E ratio, or CAPE, championed by Yale economist Robert Shiller.

Keep that in mind, and consider a few headlines from the past two months:

"Consumer confidence hits 30-year low"

"US consumer confidence plunges to recession levels"

"Consumer confidence plunges as hope dims"

"Consumer confidence tumbles, home prices stagnate"

"Consumer confidence lowest since Great Recession"

Don't use this information alone to rush out and buy stocks. The standard caveats apply to the above chart: Correlation doesn't mean causation, no one knows how low consumer confidence might fall, and the future is still inherently unpredictable. As I showed earlier this week, retail investors by and large are not fleeing the market. But there's something to be said for the fact that, historically, it would be rare for consumer confidence to be this low and not see stocks rally strongly over the coming years.

And it's not just consumer confidence that's low. As Jason Zweig wrote in TheWall Street Journal, an investor survey conducted by a team of psychologists in August showed that "58% of investors ... believed that their future would be 'moderately' or 'greatly' limited, up from 56% in March 2009." Another survey released last week by Human Events found that "only 61% of respondents have at least 'some' confidence in the U.S. capital markets, compared with 68% in 2010 and 73% in 2009." For contrarians, these are some of the surest signs that stocks are poised to do well .

It's easy to spurn the idea that stocks' future might now be brighter than it's been in years. After all, unemployment is at a generational high, real wages are stagnant, budget deficits are spiraling, and America seems to be losing its edge on the global stage. But some version of those same fears were around in 1974, 1982, and 1991. All three periods were followed by hellacious rallies, not just because things did get better, but because expectations that things could get better were so low.

Think about a few of today's stocks. Apple (NAS: AAPL) is one of the most successful companies on the planet, yet it trades at just 10.5 times forward earnings. Intel (NAS: INTC) trades at less than 10 times earnings, and its dividend yield is 50% higher than the yield on 10-year Treasury bonds. 3M (NYS: MMM) sells for 12 times earnings. ArcelorMittal (NYS: MT) sells for about half of book value.

The message these companies' investors are sending is clear: ho-hum. They're nervous about the future. Their confidence is low.

Will their views be proven right?

As a group, have they ever been?

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.

At the time thisarticle was published Fool contributorMorgan Houseldoesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel.The Motley Fool owns shares of Apple and Intel. The Fool owns shares of and has bought calls on Intel. Motley Fool newsletter services have recommended buying shares of 3M, Apple, and Intel. Motley Fool newsletter services have also recommended creating a bull call spread position in Intel and Apple, as well as a diagonal call position in 3M. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.