Natural Gas 301

Welcome to our Natural Gas series aimed at introducing investors to the fundamentals of the industry. We've already covered the production basics, and horizontal drilling and hydraulic fracturing, so today we dive into numbers -- introducing the metrics that can be important in evaluating individual companies and the industry at large.

Ratios

Though investors may certainly apply a slew of popular ratios (P/E, EPS, debt-equity, etc) to natural gas producers, the most relevant ones for the industry are unrelated to the balance sheet or income statement. A gas producer's primary assets are its reserves, and they aren't listed on the balance sheet.

Instead, investors should flip to the "Proved Reserves" table in the company's 10-K. We'll use Anadarko (NYSE: APC) for these exercises, its table is below:

Source: Annual report.

Now that we have our data, let's learn how to get it to say what we want to hear.

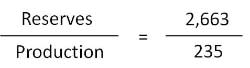

Reserve life index

The reserve life index, or the reserves-to-production ratio, measures how long reserves would last if there were no new discoveries or acquisitions.

Anadarko's reserve life index is 11 years. Intuitively, it is easy to assume that the higher the RLI the better. In reality though, a high RLI, say 25 years, could mean that a particular company is unable to develop its reserves which could illuminate a more serious problem (no money!).

It's also important to note, after a merger or acquisition it is possible for this number to be high simply because the parent company has not yet had the opportunity to develop those reserves.

Reserve replacement ratio

This is a simple ratio that indicates whether a company is replacing or depleting its reserves year over year.

Anadarko's reserve replacement ratio is 150%, which means the company does in fact replace reserves from year to year.

Gas companies can replace reserves in two ways. "Through the drill bit" refers to reserves replaced through exploration. "Bought" refers to increased reserves through acquisition. Through the drill bit is the preferred method because it implies firsthand knowledge of the new gas and reinforces a company's claim to technical prowess.

While these ratios seem pretty straight forward, this wouldn't be the natural gas industry - heck, this wouldn't be investing - without some sort of discrepancy in the way companies account for and report reserves.

The industry

In 2008, the SEC bowed to industry pressure and loosened the requirements for reporting reserve estimates; consequently, estimates increased and so did stock value. Natural gas has boomed since then and, depending on the crowd you run with, you have likely heard reserves described as "enough gas to last a century" or "Ponzi scheme".

Reserves are the major assets of any oil and gas company, but they only get paid for what they pull out of the ground and it's important to keep that in mind at all times.

Breaking even

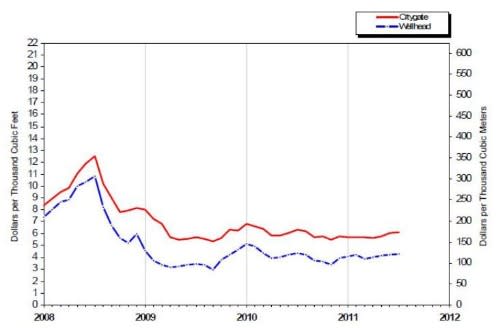

Another issue in the industry right now is the depressed price of natural gas in the U.S. Over the last three years production has boomed and the price has tanked.

Source: Energy Information Administration.

The domestic price of natural gas is now so low that companies are almost guaranteed to lose money if they don't operate efficiently. Here are the most recent break even points for ten natural gas producing companies:

Company | Break Even Price |

|---|---|

Southwestern Energy (NYSE: SWN) | $3.50 |

Range Resources (NYSE: RRC) | $5.00 |

EV Energy Partners (Nasdaq: EVEP) | $5.10 |

Quicksilver Resources (NYSE: KWK) | $6.01 |

Carrizo Oil & Gas (Nasdaq: CRZO) | $6.05 |

Chesapeake Energy (NYSE: CHK) | $6.10 |

PetroQuest Energy (NYSE: PQ) | $6.50 |

EXCO Resources (NYSE: XCO) | $6.95 |

Forest Oil (NYSE: FST) | $7.00 |

Continental Resources (NYSE: CLR) | $7.10 |

Source: Bank of America Merrill Lynch.

Though it seems that most of these companies are in terrible trouble with gas prices hovering around $4.00, there is another factor that comes into play here. First, natural gas liquids, or NGLs, track the West Texas Intermediate and generally sell for about 50% of the price of a barrel of oil. So, while production typically yields much more methane, often times there are enough NGLs in the mix to make drilling worthwhile. Additionally, companies may opt to pursue other gas plays that are rich in oil and NGLs, and avoid the areas that contain mostly dry gas.

For example, drillers have recently left the Barnett Shale to pursue other plays in Texas that are rich in oil and NGL. At the peak of 2008, there were 203 active drilling rigs in the Barnett. Now there are only 53, as companies have made of for the Permian basin and the Eagle Ford shale in search of the more lucrative commodities. It is the first time in 16 years that more rigs are drilling for oil than gas in the U.S. When the price of gas climbs again, the drillers will return to the Barnett.

Never stop learning

There is always plenty more to learn out there. For industry news and updates, load up My Watchlist with the energy companies above, and consider following trade publications like @plattsgas and amazing writers like @TMFDuffy on Twitter.

Can't get enough natural gas? Click here to check out the Motley Fool's special free report "One Stock to Own Before Nat Gas Act 2011 Becomes Law."