3 Stocks Near 52-Week Lows Worth Buying

Just as we examine companies each week that may be rising past their fair value, we can also find companies potentially trading at a bargain price. While many investors would rather have nothing to do with companies tipping the scales at 52-week lows, I think it makes a lot of sense to determine whether the market has overreacted to the downside, just as we often do to the upside.

Here's a look at three fallen angels trading near their 52-week lows that could be worth buying.

Relax, it's a Maytag

Just as Whirlpool (NYS: WHR) attempts to provide peace of mind for consumers purchasing its appliances, investors need to simply relax following a worse-than-anticipated earnings report. It's really not a surprise that Whirlpool's guidance stunk, especially considering that consumer sentiment figures are lower than they've been in two-and-a-half years and big-ticket items aren't moving well anywhere. But the world's biggest appliance maker still has plenty to offer investors.

Despite the 14% haircut on Friday, Whirlpool will remain strongly profitable. The company's revised forecast, though lower, still calls for $4.75-$5.25 in EPS this year and will extend its streak of profitable years to nine. If the housing market is as bad as KB Home's (NYS: KBH) results indicate, and Whirlpool can still crank out approximately $5 in EPS, just imagine how strong Whirlpool's bottom-line growth will be when the housing market does finally stabilize. At less than seven times next year's earnings estimates and sporting a dividend nearing 4%, you'd be crazy to ignore the strong historical results of Whirlpool.

Be SMART, don't be stupid

Shareholders of SMART Technologies (NAS: SMT) probably aren't feeling too intelligent lately -- especially since their stock has lost 62% of its value year-to-date. The maker of erasable interactive whiteboard technology has found the going tough with the spending outlook on the education sector hazy at best. Still, SMART Technologies may be able to wipe away its poor performance with a few more profitable quarters.

Traditional for-profit educators like DeVry (NYS: DV) and Apollo Group (NAS: APOL) are significantly at risk of a revenue hit because the funding required to facilitate student loans could be at risk with more budget cuts still looming in Congress. SMART Technologies, on the other hand, is only marginally affected by for-profit education's woes, as it has a wide array of customers in the educational, business, and government markets.

In August, SMART reported a tripling in its first-quarter profit despite an 8% decline in revenue. SMART is able to grow profits so rapidly because it keeps a close eye on margins; gross margins are now around 50%. Perhaps the ultimate value in the education sector, SMART is trading at less than five times forward earnings and recently authorized a share repurchase program which allows the company the option to buy up to four million shares on the open market as it sees fit. So I'm once again appealing to investors: Be SMART, not stupid!

The numbers game

The stock market is a numbers game -- and the numbers don't always add up. Take Agnico-Eagle Mines (NYS: AEM) , which has plunged 23% since announcing it would shut down its Goldex Mine in Val d'Or, Quebec, indefinitely because of water inflow and ground instability issues. I'm not going to in any way try to spin the shutting down of one of the company's lowest-cost mines into a positive, because it's not. But things are not nearly as bad as they appear on the surface.

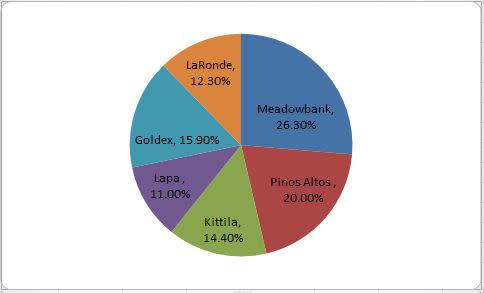

Estimated production estimates for the Goldex Mine in 2012 vary somewhat, with a Dahlman Rose analyst claiming it would comprise 14% of all gold output next year, while the Fool's own Travis Hoium pegs the figure closer to 17%. However, either way you look at it, 14% or 17% doesn't exactly equal 23%. Here's a quick glance at the year-to-date gold output breakdown for Agnico-Eagle across its six mines:

Source: CNW Group. Numbers add up to less than 100% due to rounding.

Even with the $260 million third-quarter charge, Agnico-Eagle managed a record quarter in terms of cash production ($198 million) and kept costs at its Pinos Altos mine to a ridiculously low $295 per ounce. Agnico-Eagle will remain solidly profitable despite the Goldex mine closure, and it has a mixture of higher realized selling prices of gold and increasing volume at its other mines to thank for that. Agnico-Eagle is valued at only 11 times forward earnings. Now compare this to rival New Gold (ASE: NGD) , which trades at 18 times forward earnings, and we once again come to the conclusion that the numbers simply don't add up. That's the great thing about gold -- despite the scratches and temporary loss of luster, it only takes one quick polish to bring back its shine. Consider this dip a major buying opportunity in Agnico-Eagle and enjoy the 1.5% dividend yield as an added bonus.

Foolish roundup

Even after a violent move higher in the indexes over the past month, there are still values left to be found. With valuations that can only be described as staggeringly cheap relative to their sector, these three stocks represent the true essence of "bottom fishing."

What's your take on these three stocks? Are they worth their weight in gold and then some, or should we toss them back from whence they came? Share your thoughts in the comments section below and consider adding Whirlpool, SMART Technologies, and Agnico-Eagle Mines to your free and personalized watchlist to keep up on the latest news with each company.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong and on Twitter, where he goes by the handle @TMFUltraLong. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that's always on the lookout for a good deal.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.