Cheap Oil Isn't Coming Back

As the world urbanizes, demand for oil could outstrip many nations' abilities to get it out of the ground. Most new discoveries have been made in difficult territory, where the costs of extraction dwarf inexpensive Middle Eastern crude. Consumers may have to get used to high prices at the pump, with or without the threat of conflict between two of the world's largest producers. There's risk for some, but great opportunity for many, so read on to discover what's happening and who's poised to strike a gusher as oil prices continue to rise.

Hanging in the balance

Saudi Arabia is the world's most prolific oil-producing state, pumping 10.5 million barrels out of the sand every day last year. That figure has been stable for several years, but the Saudi people have actually been using more oil themselves, leading to stagnant to declining production surpluses.

Source: U.S. Energy Information Administration and author's calculations.

These are five of the world's six largest oil producing countries -- Russia is the other, holding steady with about 7 million barrels per day in surplus -- but none of the largest net exporters have substantially improved their balance in the past five years. New and expanded fields in Canada, the United States, Brazil, and other Latin American nations can inject more black gold into the world's veins, but it's unlikely that any can supplant the Saudis in terms of total output. If Saudi output were to decline, it could have dangerous consequences for global oil supplies. Even if Saudi output remains at the same level, it could be a big problem down the road as oil demand keeps increasing.

Fields of black gold

The crown jewel of Saudi oil production is the Ghawar field. The Saudi kingdom closely guards information on Ghawar, but many estimates place the super field's production in the range of 5 million barrels per day, roughly half the country's total output. Ghawar alone produces about as much oil as the nations of India, Oman, Colombia, Argentina, Malaysia, Egypt, and Australia together. It's also been at the epicenter of the peak oil debate for years, as research has uncovered increasing difficulty in getting oil out of Ghawar. Other Saudi fields have also been facing the same issues.

This is important because worldwide oil use has been growing steadily over the past 30 years without a commensurate increase in major new oil field discoveries. The Bakken shale formation, which became an exciting play because of new oil recovery technologies, only produces a tenth as much oil as Ghawar, and does so with greater difficulty. The Canadian oil sands produce about a fifth as much oil as Ghawar.

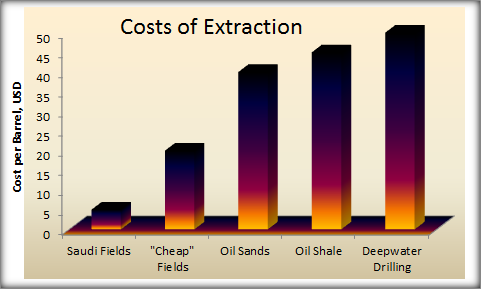

The harder it comes, the higher it costs

A major problem with most new oil fields is that extraction costs are much higher than they are in fields like Ghawar. Even cheap, easily accessible oil in other places is quite a bit more expensive to get out of the ground than Saudi oil. It's good to have a monopoly, as long as you can keep it running.

Source: News reports and government agency estimations.

The more the world relies on unconventional oil extraction, the less likely it is to ever see cheap oil again. The last substantial drop in prices came when everything else was crashing in 2008. Demand retreated in the midst of economic carnage, but it's a lot easier to manage reduced need than it is to cope with a need that simply can't be met.

Rise of the West

Cheap, easy oil is gone, but demand isn't going to go away. Alternative energy could become increasingly important, but it hasn't reached the point of fueling our transport system yet. Promising new oil fields are the best bet for the medium term and could offer substantial gains as production ramps up while the price of oil continues to appreciate. A number of major new oil projects (that we can invest in, anyway) have been in the Western Hemisphere, and many offer the promise of greater expansion. The Bakken shale area, for example, is hitting a wall not because of extraction difficulties, but because the transportation infrastructure isn't big enough.

Offshore discoveries are a bonanza for Brazil's Petroleo Brasiliero (NYS: PBR) , and for Seadrill (NYS: SDRL) , which is constructing several Brazilian deepwater rigs. ATP Oil and Gas (NAS: ATPG) also has numerous offshore operations, though the vast majority are in the Gulf of Mexico. Despite its solid presence, much of ATP's reserves remain undeveloped, so there's still opportunity for growth beyond the expectation of higher oil prices.

Canada's Athabasca oil sands have seen heavy development investment from Suncor Energy (NYS: SU) , and Penn West Petroleum (NYS: PWE) has fields in the Peace River sands. As a master limited partnership, Penn West offers higher yields than most and could be a good play for dividend-hungry energy investors. U.S. petroleum producers are varied, but one lesser-known company with the potential to perform is Samson Oil and Gas (ASE: SSN) , which has two Bakken-area holdings it has yet to fully develop. Another option might be SandRidge Energy (NYS: SD) , which operates in "easier" areas like Texas and the Midwest, and has been investing heavily in the infrastructure needed to ramp up its oil production.

If you'd like the inside scoop on some other excellent oil companies, check out The Motley Fool's analysis of three poised to profit from $100 oil. Find out more about them in this free special report before the rest of the world catches on.

At the time thisarticle was published Fool contributor Alex Planes holds no financial stake in any company mentioned here. Follow him on Google+ for more news, observations, and random attempts at wit.Motley Fool newsletter services have recommended buying shares of Petroleo Brasileiro. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.