A Brief History of UnitedHealth's Returns

Despite constant attempts by analysts and the media to complicate the basics of investing, there are really only three ways a stock can create value for its shareholders:

Dividends.

Earnings growth.

Changes in valuation multiples.

In this series, we drill down on one company's returns to see how each of those three has played a role over the past decade. Step on up, UnitedHealth (NYS: UNH) .

UnitedHealth shares returned 200% over the past decade. How'd they get there?

Dividends provided a small boost. Without dividends, shares returned 192% over the past ten years.

Earnings growth over the period was incredibly strong. UnitedHealth's normalized earnings per share grew at an average rate of 24% a year for the past ten years. That's among the best results you can find among large-cap companies. Of course, it also highlights what has become a touchy public-relations issue -- that surging health care costs are padding the bottom line of insurance companies.

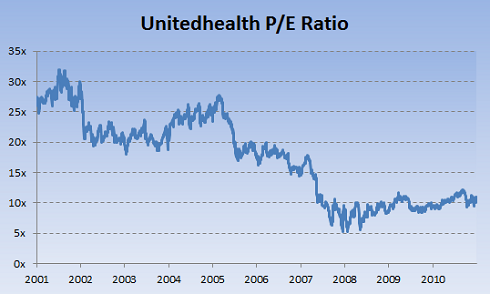

Leave that issue aside for now. UnitedHealth's stock has been a strong performer, but not as strong as it should have been given 24% annual earnings growth. Why? This chart explains it:

Source: S&P Capital IQ.

UnitedHealth's valuation multiple has utterly collapsed -- from 27 ten years ago to 11 today. That's prevented a lot of the earnings growth from showing up in shareholder returns. The same has been true for competitors WellPoint (NYS: WLP) and Aetna (NYS: AET) ; compressing valuation multiples have put the lid on shareholder returns.

The reason for the valuation fall is twofold. One, shares were likely overvalued ten years ago. The fall over the past decade has been a reversion to normal. Two, the 2010 health care reform bill adds multiple layers of uncertainty that the market hasn't -- more than a year later -- gotten comfortable with.

That uncertainty could indeed impact future earnings. But the good news is that, at 11 times earnings, shares are already pricing in a lot of bad news. While shareholders suffered through a valuation contraction over the past decade, the coming one could very well reward them with valuation expansion.

Why is this stuff worth paying attention to? It's important to know not only how much a stock has returned, but where those returns came from. Sometimes earnings grow, but the market isn't willing to pay as much for those earnings. Sometimes earnings fall, but the market bids shares higher anyway. Sometimes both earnings and earnings multiples stay flat, but a company generates returns through dividends. Sometimes everything works together, and returns surge. Sometimes nothing works and they crash. All tell a different story about the state of a company. Not knowing why something happened can be just as dangerous as not knowing that something happened at all.

Add UnitedHealth to My Watchlist.

At the time thisarticle was published

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.