Did Facebook's $100 Billion Dream Just Die?

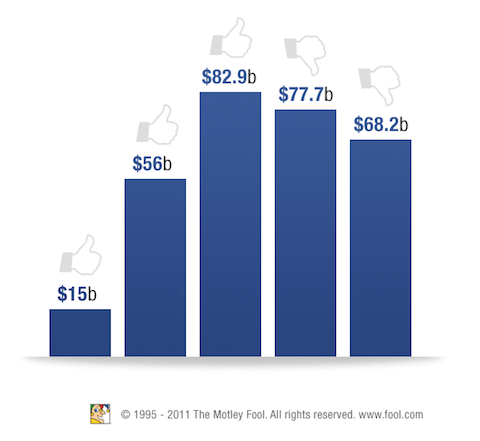

Once thought to be worth $100 billion or more, new data from private equity exchange SharesPost says Facebook is trading for an implied value of $68.2 billion.

Is this really as bad as it sounds? Yes, and no. Yes, because Facebook's value has long been driven by a feeding frenzy of demand. If demand has dried up in the wake of Google's (NAS: GOOG) introduction of Google+ and Apple's (NAS: AAPL) integration of Twitter into the iPhone, it means there's little chance that Facebook will reach the $150 billion highs one of my Foolish colleagues predicted earlier this year.

But also no, because SharesPost is an illiquid private exchange in which a small pool of Big Money investors moves shares more than they otherwise might if traded on a public exchange. More than anything, the drop-off means that those with deep pockets like other issues more.

Two issues, in particular, according to the SharesPost report I received earlier today. Social-gaming specialist Zynga now trades at an implied valuation just north of $12 billion, down from $20 billion this summer but up from $10 billion in February. Investors apparently believe the Facebook favorite is capable of competing or even beating console rivals Activision Blizzard (NAS: ATVI) and Electronic Arts (NAS: ERTS) .

SharesPost also singled out online dating specialist eHarmony, whose implied market value is up 10% to $611 million. Chinese dating site Jiayuan.com (NAS: DATE) commands just $210 million in market cap by comparison.

Interestingly, Facebook isn't the only one falling. Groupon has scaled back its implied valuation heading into an IPO roadshow. Fools may also remember that Google offered $10 billion for Twitter at one time. Now, SharesPost says, the microblogger's privately held shares are trading at an implied value of $6.9 billion -- a 31% haircut. Facebook, by contrast, is down 18% from its January high:

That's still meaningful. Mostly, it says private investors aren't as sure about paying a premium to own shares of the social network. Maybe that's due to competition. Or market mania. Or the early migration of sparrows to the American Midwest. Whatever the cause, Facebook is worth less today, which means investors betting on a $100 billion IPO next year are probably going to be disappointed.

Do you agree? Disagree? Please weigh in using the comments box below. And if you're looking for more IPO ideas, try this free report from my Foolish colleagues and I. In it you'll get all the details on a newly public company that's remaking the quick serve restaurant business in Latin America. You'll also get a closer look at 10 more IPOs with soaring potential -- including a wireless rebel singled out by yours truly. Get your copy of the report; it's 100% free.

At the time thisarticle was published Fool contributorTim Beyersis a member of theMotley Fool Rule Breakersstock-picking team. He owned shares of Apple and Google at the time of publication. Check out Tim'sportfolio holdingsandFoolish writings, or connect with him onGoogle+or Twitter, where he goes by@milehighfool. You can also get his insightsdelivered directly to your RSS reader.The Motley Fool owns shares of Google, Apple, Jiayuan.com International, and Activision Blizzard. TheMotley Fool newsletter serviceshave recommended buying shares of Jiayuan.com International, Apple, Activision Blizzard, and Google, creating a bull call spread position in Apple, and creating a synthetic long position in Activision Blizzard. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.