There's More to GE's Earnings Than Meets the Eye

It's another quarter in the books for General Electric (NYS: GE) , the Dow Jones Industrial Average's (Index: ^DJI) oldest member, and based on its third-quarter results Wall Street didn't seem all too thrilled, sending the stock down 2% on Friday.

Before the credit crisis in 2008, GE was practically unstoppable. If you had asked me five years ago I'd have placed the company next to death and taxes as possibly the only other thing on Earth you could count on. Well, the credit crisis in 2008 proved that theory of mine dead wrong, and GE's crippled financial arm showed that this conglomerate is just as fallible as any other company.

But Wall Street may have overlooked some key points to last week's earnings report, which wasn't nearly as bad as GE's 2% drop on Friday would indicate.

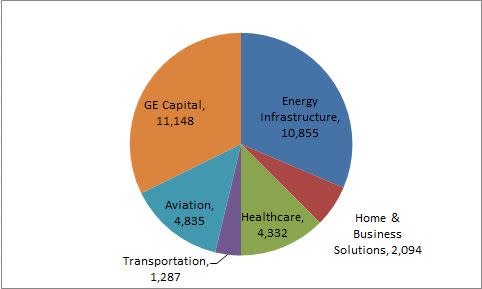

For starters, GE's bread-and-butter segments, energy and GE capital, both appear on track to contribute solid results for the company. GE relies heavily on its energy innovations and its financial arm to deliver to its bottom line:

Source: PR Newswire, all figures in billions of U.S. dollars.

With revenue for its lending division flat year-over-year, you might anticipate that growth there has stalled -- but it's actually quite the opposite. Major corporations are taking advantage of historically low lending rates, which has boosted GE's lending business and helped crank up third-quarter profits by 79% because of more beneficial net interest margin spreads. The lending segment's tier-one capital ratio is also up to 11%, signaling that the company is well-capitalized. This is important because just a few years ago, this same lending segment cost the company upwards of $1 billion in writedowns.

GE's energy infrastructure segment experienced an impressive 30% jump in revenue over the year-ago period, with the strongest growth coming from the BRIC countries, as well as Canada, Mexico, and the Middle East. This marked the third consecutive quarter of at least 9% revenue growth for this division. Although energy and infrastructure profits fell by 9% because of lower wind margins, GE appears significantly more diversified than its solar counterparts like First Solar (NAS: FSLR) and SunPower (NAS: SPWRA) (NAS: SPWRB) , which have been crushed by falling prices for solar panels. As solar companies struggle to stay afloat, GE's alternative energies are charging ahead and putting profits in the books.

GE's other segments weren't slouches, either. The company's aviation and health-care segment provided steady revenue growth of 10% and 9%, respectively, while the transportation sector kicked in a 94% jump in overall profits.

Now keep in mind, Wall Street didn't like this report much. I, however, think this is another step closer for GE to getting back to its roots -- namely, lending and energy innovations. The company has been able to generate $6.5 billion in cash from industrial operations over the past nine months, which facilitated the purchase of $1 billion worth of shares during the third quarter. With GE having ended the quarter with $91 billion in consolidated cash and sporting a dividend yield of 3.7%, I really don't see what Wall Street is pouting about.

GE looks well on its way to reclaiming its spot among Wall Street's dividend elites -- but don't stop there. Reserve your copy of our latest free report which can help you "Secure Your Future With 11 Rock-Solid Dividend Stocks."

What's your take on General Electric's quarterly results? Sound off in the comments section below, and consider adding this Dow Jones favorite to your free and personalized watchlist to keep up on the latest news with the company.

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. He wonders if he mentioned that he liked unicorns in this sentence if anyone would even notice. You can follow him on CAPS under the screen nameTMFUltraLongand on Twitter, where he goes by the handle@TMFUltraLong. The Motley Fool owns shares of First Solar.Motley Fool newsletter serviceshave recommended buying shares of First Solar. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.