Did Coca-Cola Just Disappoint?

In its third quarter results, Coca-Cola (NYS: KO) confirmed a few challenges that are providing some headwinds for the company right now.

Those challenges included commodity price levels, which the company is trying to deal with by carefully raising prices -- a move that we've seen at most other consumer packaged goods companies including archrival PepsiCo (NYS: PEP) , Procter & Gamble (NYS: PG) , and Kimberly-Clark (NYS: KMB) . As a global company, Coke also has to navigate the worldwide currency markets, which are all over the place thanks largely to the mess over in Europe. And of course there're the broad economic problems that are particularly noticeable in Coke's 1% organic growth in North America and the basically flat volume in Europe.

But this is still a well-run company with a fantastic brand that can pump out cash like it's nobody's business. So how should investors think about the results from the quarter?

Mind the big picture

From a high level, we really want to keep an eye on how much product Coke is selling and how much money it's able to make doing that.

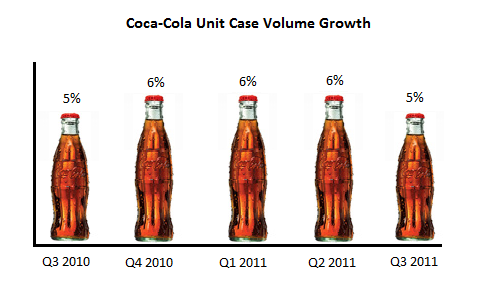

To check out how much Coke's actually been selling, let's take a look at the trend in total unit case volume growth.

Source: Company filings.

The 5% growth in the most recent quarter is obviously a downshift from the 6% growth the company was notching in the previous three quarters, but that hardly seems like a development that investors should get too worked up about. What we should watch for, though, is whether unit volume slips further in the quarters ahead.

Of course, growth in the amount of product that the company is selling is of less consequence if the company is making less profit on what it sells, so it's imperative to keep an eye on Coke's margins as well.

Source: Company filings.

What we see here is slightly more concerning. As far as profitability goes, the third quarter of 2010 isn't really comparable with the rest of the periods because Coca-Cola closed the acquisition of its bottler -- Coca-Cola Enterprises, which is a lower-margin business -- after that quarter closed. What we've seen since then, though, is a definite weakening in gross margins. This is largely the result of rising commodity prices that I mentioned above.

Looking ahead, investors will want to keep an eye on how both profit lines move, with particular attention on gross margins. A big part of the thesis behind investing in a company with massive brand power like Coke is that it can push rising input costs on to customers and maintain profitability even in an inflationary environment. If the company isn't able to do this, investors should be worried.

The results from this quarter don't reveal any reason for long-term owners of Coke to jump ship. However, savvy shareholders and potential owners will want to keep up to date on what's going on at the company, and they can do that by adding Coke to their Foolish watchlist. And the Coke fans that don't have watchlists set up yet can quickly and easily set one up for free by clicking here.

At the time thisarticle was published The Motley Fool owns shares of PepsiCo and Coca-Cola.Motley Fool newsletter serviceshave recommended buying shares of Procter & Gamble, Kimberly-Clark, PepsiCo, and Coca-Cola; and creating a diagonal call position in PepsiCo. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors.Fool contributorMatt Koppenhefferdoes not have a financial interest in any of the companies mentioned. You can check out what Matt is keeping an eye on by visiting hisCAPS portfolio, or you can follow Matt on Twitter@KoppTheFoolorFacebook. The Fool'sdisclosure policyprefers dividends over a sharp stick in the eye.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.