A Brief History of Hewlett-Packard's Returns

Despite constant attempts by analysts and the media to complicate the basics of investing, there are really only three ways a stock can create value for its shareholders:

Dividends.

Earnings growth.

Changes in valuation multiples.

In this series, we drill down on one company's returns to see how each of those three has played a role over the past decade. Step on up, Hewlett-Packard (NYS: HPQ) .

HP has returned 64% to shareholders over the past decade. How did it get there?

Dividends accounted for a decent chunk of it. Without dividends, HP shares returned about 45%.

Earnings growth over this period was phenomenal. HP's normalized earnings per share have grown at an average rate of over 18% per year for the past decade -- among the top tier of all large-cap companies during the period. A good amount of the growth can be attributed to repurchasing shares outstanding, which HP has done aggressively in recent years.

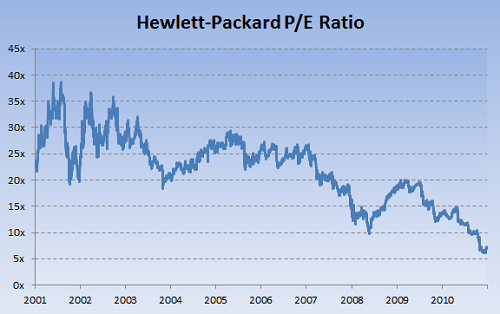

But here's what really sticks out -- the change in HP's P/E ratio:

Source: S&P Capital IQ.

This drop is astounding not just in scale -- falling some 70% over the past decade -- but the absolute value of the current multiple. At about six times earnings, the market isn't just pricing HP for no growth, but negative growth going forward.

The vast majority of HP's earnings growth over the past decade have been discounted by a compressed earnings multiple. Other tech companies like Microsoft (NAS: MSFT) and even Apple (NYS: AAPL) are in a similar boat, but nowhere near the degree of HP. Despite a recent history of being poorly managed, some investors are starting to warm up to the idea that HP is a value stock too cheap to ignore. Even if earnings stays tepid for the indefinite future, an expansion back to a reasonable earnings multiple could generate significant shareholder returns.

Why is this stuff worth paying attention to? It's important to know not only how much a stock has returned, but where those returns came from. Sometimes earnings grow, but the market isn't willing to pay as much for those earnings. Sometimes earnings fall, but the market bids shares higher anyway. Sometimes both earnings and earnings multiples stay flat, but a company generates returns through dividends. Sometimes everything works together, and returns surge. Sometimes nothing works and they crash. All tell a different story about the state of a company. Not knowing why something happened can be just as dangerous as not knowing that something happened at all.

Add Hewlett-Packard to My Watchlist.

At the time thisarticle was published Fool contributorMorgan Houselowns shares of Microsoft. Follow him on Twitter, where he goes by@TMFHousel. The Motley Fool owns shares of Microsoft and Apple. Motley Fool newsletter services have recommended buying shares of Microsoft and Apple. Motley Fool newsletter services have recommended creating a bull call spread position in Apple. Motley Fool newsletter services have recommended creating a bull call spread position in Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.