Earnings Season Preview: The Top Gambling Stocks to Watch This Earnings Season

Here at the Fool, we love our seasons: football season, flip-flop season, and our favorite -- earnings season. It's that wonderful time of year when we get to celebrate those picks that outperformed and be humbled by those that didn't.

Each quarter, we get to arm ourselves with a new set of expectations and estimates to better judge the economic landscape. We may not always nail our bets, but learning about the expectations for a given sector will place investors well ahead of many of their peers. Woody Allen put it best when he observed, "Eighty percent of success is showing up."

With that in mind, here is what you can expect to see out of some of the biggest names in gaming this earnings season just by showing up and staying engaged:

Source: S&P Capital IQ.

The consumer discretionary sector on a whole expects a 7.6% decrease over last quarter's performance, but a 12% increase over the same quarter last year. Considering the lingering sensitivity of consumer spending and the seemingly constant trend of economic fits and starts, this is a bold estimate. Then again, the sector as a whole has rebounded impressively from their consumer dog-day estimates from the last quarter of 2008 -- negative $0.37.

Let's see how some of the notable players in gambling are expected to perform and what to look for in these releases:

Company | Report Date | Estimated Earnings | Earnings Estimate 90 Days Ago | Year-Ago Earnings |

|---|---|---|---|---|

Wynn Resorts (NAS: WYNN) | Oct. 19 | 1.18 | 0.92 | 0.39 |

Boyd Gaming (NYS: BYD) | Oct. 25 | 0.02 | 0.01 | 0.02 |

Pinnacle Entertainment (NYS: PNK) | Oct. 27 | 0.16 | 0.12 | 0.10 |

Las Vegas Sands (NYS: LVS) | Oct. 28 | 0.52 | 0.45 | 0.34 |

MGM Resorts (NYS: MGM) | Nov. 3 | (0.15) | (0.13) | (0.21) |

Melco Crown (NAS: MPEL) | Nov. 23 | 0.11 | 0.05 | 0.03 |

Sources: S&P Capital IQ and Yahoo! Finance.

As you can see, analysts are largely optimistic about this earnings season for gaming stocks. Wynn and Melco are slated to rake in earnings more than 200% higher than what they reported last year. By contrast, MGM is expected to continue its streak of losing quarters, with analysts predicting a $0.15 loss per share. What's behind these strikingly different tones?

Winners and losers

There are a lot of reasons to be bearish on MGM. It is overexposed to Las Vegas, particularly through its CityCenter project, but the city as a whole has had a choppy recovery and is on very shaky ground. MGM has an enormous amount of debt, $12.6 billion at last count, and doesn't have any promising growth on the horizon. Our gaming expert, Travis Hoium, covers these factors in better detail in his recent article.

By contrast, Las Vegas Sands is sitting pretty. Its brilliantly designed Marina Bay Casino is one of two allowed to operate in Singapore, which is quickly becoming one of the hottest gaming corners of the world. Singapore's two resorts are projected to take in $6.4 billion combined this year -- not far behind the Las Vegas Strip's $6.8 billion peak in 2007 -- and ahead of their current year projection of $6.2 billion. Furthermore, Las Vegas Sands owns the only new casino set to hit Macau in the foreseeable future, the Sands Cotai Central.

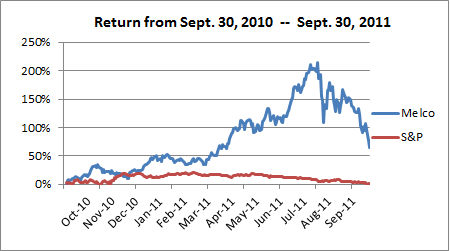

Melco is flying high on gaming expectations in Macau, the only market it operates in. And being a pure play in the largest gambling market in the world can be nice. Just recently Macau reported September revenue 39% higher than the same time last year. An investment in Melco at the end of September 2010 until September 2011 would have yielded 63%, compared with the S&P's less than 1%.

Source: S&P Capital IQ.

As you can see, Melco's return is something akin to a roller coaster ride, while the S&P is more like a wheelchair ramp. Depending solely on one market for growth can result in wild swings if anything in that market changes. As evidence, consider the recent speculation of a Chinese economic slowdown that sent Melco's stock tumbling.

When the chips are down

How should investors carry this information with them to earnings season? Personally, I'm going to be focusing on casino diversification by operators, specifically Las Vegas Sands. Operators that rely heavily on one market can see their fortunes change quickly, leaving them holding the bill on massively expensive properties. I'm going to be reading through the gaming industry's earnings to see which operators (if any) have plans to expand by putting up casinos in new markets. Rumor has it that Las Vegas Sands is looking at Miami for future growth.

With any luck, these companies will drop gems on investors by discussing their intentions for new opportunities. If you're looking for other gems be sure to consult this special free report from our Hidden Gems gurus: "Too Small to Fail: Two Small Caps the Government Won't Let Go Broke." These are the same analysts who identified Chipotle as a win in early 2009 and have rode it to more than 400% returns today. Fool on!

At the time thisarticle was published Austin Smithholds no positions in any of the companies mentioned in this article. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.