Don't Ignore This Warning Signal, Growth Investors

When cable broadband equipment provider Arris Group (NAS: ARRS) purchased BigBand Networks (NAS: BBND) for $2.24 a share, it looked like a rescue. And why not? Arris is spending just $53 million in cash after factoring in the value of BigBand's liquid assets.

That may as well be bankruptcy pricing. Consider: According to S&P Capital IQ, BigBand was worth $1.66 a share in tangible book value following last quarter's report, a figure that doesn't include BigBand's patents, which Arris referred to as "valuable" in a statement explaining the rationale for the deal.

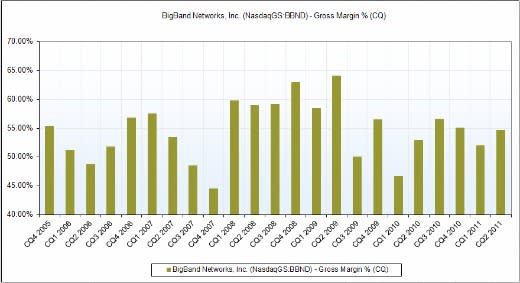

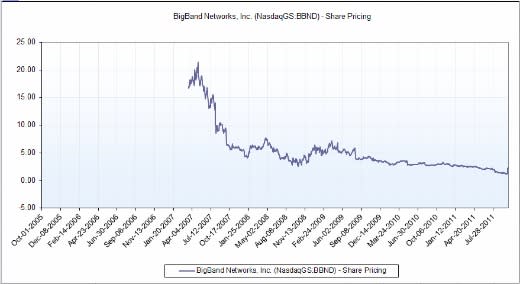

Whether or not Arris can make good on BigBand's technology for distributing digital video across networks remains to be seen. The lesson I draw from this buyout as an investor is that margins still matter. Have a look at how BigBand's gross margin -- otherwise known as the profit left after subtracting direct production costs -- deteriorated in the quarters after going public in 2007:

BigBand Networks' Gross Margin History

Source: S&P Capital IQ.

Source: S&P Capital IQ.

Notice how the share price tracked lower as BigBand's margin fell nearly 10 percentage points in its first year as a public company. Management reversed the trend for a time, but by mid-2008 it was already too late -- investors weren't interested anymore. And by mid-2009, the pricing pressure that had plagued BigBand early on reappeared. That the company has survived as an independent entity this long is a credit to CEO and co-founder Amir Bassan-Eskenazi.

Unfortunately, BigBand isn't the only tech company to suffer the indignity of margin compression:

Longtime Internet service provider United Online (NAS: UNTD) saw year-over-year gross margin dip four percentage points in the latest quarter. And that's just the latest downdraft. United's 77% gross margin from 2006 and 2007 is a distant memory, replaced with a 52% clip over the trailing 12 months.

Sonus Networks (NAS: SONS) , which competes with Acme Packet (NAS: APKT) in selling infrastructure for transmitting voice and data over networks, saw a drastic decline in gross margin in the March quarter -- down more than 20 percentage points -- and then further compression in Q2. Not surprisingly, the stock is off more than 14% year to date.

And these are just two examples. Be careful, tech investors. Revenue growth is good. Accelerating revenue growth is better. But revenue growth derived from deep cuts in gross margin is almost never worth the price. Just ask the poor souls who've held shares of BigBand Networks since the IPO.

On the other hand, Arris was our top 2011 pick in this special free report. Download it now to find out why the company is riding a trend that will see the rate of Internet traffic quadruple by 2015. Intrigued? Just click here to get started.

At the time thisarticle was published Fool contributorTim Beyersis a member of theMotley Fool Rule Breakersstock-picking team. He didn't own shares in any of the companies mentioned in this article at the time of publication. Check out Tim'sportfolio holdingsandFoolish writings, or connect with him onGoogle+or Twitter, where he goes by@milehighfool. You can also get his insightsdelivered directly to your RSS reader.Motley Fool newsletter serviceshave recommended buying shares of Acme Packet. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.