Just When You Thought It Was Safe to Go Back in the Water: An Update on Market Volatility

Volatility in the third quarter of 2011 tripled quarter-over-quarter as U.S. stock market investors were beset by a combination of darker economic circumstances and apparently shaky political leadership. For the quarter, the average daily change in the value of the S&P 500 (INDEX: ^GSPC) index was +/- 1.60%, as compared to +/- 0.54% in the second quarter, a huge increase of 196%.

I track market volatility because it is a reasonably reliable gauge of risk levels; 74% of the time from 1950 to 2011, when volatility in the S&P 500 goes up -- that is, the average annual daily change in the price of the index (up or down) is greater than it was in the prior year -- market performance declines. And when volatility declines year-over-year, market performance improves 55% of the time.

Normally, the market is remarkably stable. On average, the S&P 500 index rises or declines 0.62% each day the market is open. Actually, 52% of the time, the change in the value of the index rounds to 0% (that is, the change is less than one-half of 1%). Another 38% of the time, the change rounds to 1%. Here is an analysis of how much the value of the S&P 500 index has changed each trading day since March 1950 through September 2011:

Daily Change | Total Days | Total Days in % Terms |

|---|---|---|

0% | 7,187 | 52.14% |

1% | 5,217 | 37.85% |

2% | 1,037 | 7.52% |

3% | 220 | 1.60% |

4% | 68 | 0.49% |

5% | 30 | 0.22% |

6% | 9 | 0.07% |

7% to 9% | 14 | 0.10% |

10+% | 3 | 0.02% |

The biggest spike ever came in 2008. To put the extremeness of the volatility in 2008 in perspective, consider that in 60 years of data, there are only three days the market moved +/-10% -- and two of them were in 2008. There are only 14 days the market moved 7% to 9% in either direction; six of those were in 2008. And six of the nine 6% days we've experienced since 1950 were in 2008.

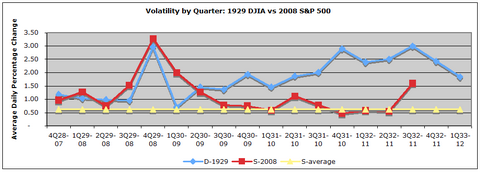

After the 2008 crash, many analysts wondered if we were in for a replay of the 1930s depression. 1929 was every bit as extreme for the Dow Jones Industrial Average (INDEX: ^DJIA) as 2008 was for the S&P 500 (which itself was not created until after World War II, which is why we rely on the Dow for the 1929 data).

Following the 1929 crash, volatility immediately declined sharply from the crash peak to a near-normal level in 1Q30, but then began a jig-jaggy climb that lasted through 1930 and 1931 and into 1932, peaking in the third quarter of 1932 at a level even higher than the fourth quarter of 1929 had reached. Up until now, the post-2008 pattern has been starkly -- and hearteningly -- different. Here is a chart that compares market volatility for the two crashes:

Measured in terms of volatility, the aftermath of the 2008 crash has looked little like post-1929. We broke below post-1929 volatility levels in 2Q09 and have remained there for the last 10 consecutive quarters, including 3Q11. (In 3Q32, the average daily change in the DJIA was a breathtaking +/-3.00%, and while we were up sharply to 158% above normal volatility in 3Q11, in 3Q32, the comparable figure was 384% above normal volatility ... we would have a long way to go to get back up there!)

And consistent with my findings that volatility levels have an inverse relationship with performance, the post-2008 market has been much friendlier than the post-1929 market was. So far:

DJIA ROI | S&P 500 ROI | ||

|---|---|---|---|

1929 | (16%) | 2008 | (38%) |

1930 | (34%) | 2009 | 23% |

1931 | (53%) | 2010 | 13% |

1932 | (23%) | *2011 | (10%) |

*Through Sept. 30, 2011.

Still, a 200% quarter-over-quarter spike in volatility and a 10% market decline have a way of grabbing one's attention.

Of course, volatility is not predictive. That is, frenetic trading does not generate a black swan event; it's the other way round. Clearly, the combination of increased longer-term risk in the U.S. -- as evidenced by the Treasuries rating downgrade and political turmoil over the raising of the debt ceiling -- and immediate dangers of sovereign debt default in Europe with the concomitant systemic risk of large bank failures is what drove the frenzied decline in 3Q11.

Should politicians in the U.S. seriously address our structural issues and/or politicians in Europe come up with a solution to the Greek crisis that persuasively addresses potential issues in Italy, Spain, etc. as well, then the storm clouds could rapidly dissipate and we could be back to boring sunny weather again.

But for now, things are uncommonly interesting on the volatility front and I will be watching the fourth quarter very closely.

If you want to hedge your bets as to how things will play out, you can effectively add the S&P 500 index to your portfolio with the SPDRs (NYS: SPY) exchange-traded fund (ETF), or short it with the ProShares Short S&P 500 (NYS: SH) . The Dow is tracked by the Diamonds Trust (NYS: DIA) ETF, or can be shorted with the ProShares Short Dow30 (NYS: DOG) ETF.

Past coverage of market volatility:

At the time thisarticle was published Guest contributor Brad Hessel currently owns ProShares SHORT S&P 500 but has no position in any of the other equities mentioned; however, Brad's clients may have such positions. The Fool's disclosure policy includes certain trading restrictions that apply to Brad. However, his clients are not subject to our disclosure policy, and thus are free to trade any such equities.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.