Beware the Myths About Gold Hedges

With so many myths about gold still dissuading many investors from gaining exposure to the time-tested monetary metal, I have no intention of letting a new myth take hold.

A barrage of articles crossed the financial newswires Monday, attempting to portray increased gold hedging activity as an indication of miners' cooling outlooks on gold prices. Please join me in promptly burying that gross misperception before it becomes yet another unfounded rationale by which investors might steer clear of gold.

Headline headaches

For a moment there, I thought I was going to have to rebut several articles on the topic. But as it turns out, Monday's gold sector headlines were infiltrated by multiple iterations of essentially the same promotional content packaged under different headlines. This one proclaimed that miners are taking "a more conservative stance toward gold prices," while peddling some reports on Yamana Gold (NYS: AUY) and Paramount Gold & Silver (ASE: PZG) . This one plugged reports under a different brand name, but utilized essentially the very same content with an even bolder headline: "Gold Begins to Lose Luster -- Miners Boost Hedging." The problem I have with this practice is that when the content is deeply flawed -- as I will show it certainly was in this case -- the potential to spread misinformation among investors is amplified by the number of similar headlines that may appear to corroborate the "analysis."

The IBTimes posted a separate (but equally egregious) misinterpretation of gold hedging data on Friday, stating: "[A] growing number of gold mining companies seem to have become more cautious again in the second quarter of this year by hedging their future output against rising price fluctuations." In truth, however, the reported second-quarter increase in the global hedge book was miniscule in scale, and was undertaken by a very few junior resource companies for specific reasons that had nothing whatsoever to do with a "more cautious" outlook on gold prices.

Keeping the numbers in context

According to Thomson Reuters GFMS, the global hedge book for gold grew by 190,000 ounces, to 5.07 million ounces. That reported increase amounts to less than one-quarter of 1% of global gold production for 2010 (78.4 million ounces). Relative to total mine production for the second quarter of 2011, the reported increase still represents just 0.8%! Furthermore, taken in the context of a 95% reduction in the global hedge book from more than 100 million ounces over the past decade, a sequential increase of the sort hardly budges the needle. In other words, the miniscule rise is scarcely newsworthy, and miles away from being indicative of any shift in sentiment.

The authors of the underlying report could not have been clearer. They stated flat-out: "[It] would be wrong to assume ... that general attitudes to hedging among the major gold mining companies have changed." Only two years ago, the world's dominant producer -- Barrick Gold (NYS: ABX) -- unloaded its giant hedge book to heal one of the more epic self-inflicted wounds the industry had ever witnessed. The miner took a horrendous $5.6 billion charge in a single quarter, and diluted shareholders to raise billions more in order to cancel its underwater bets. AngloGold Ashanti (NYS: AU) followed a similar course on a somewhat smaller scale just last year. Gold investors and gold mining executives alike retain strong expectations for further gains from gold, and neither group is willing to bet against this powerful secular trend.

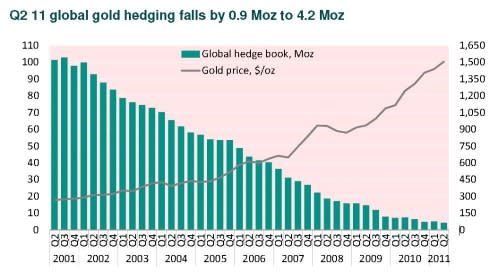

As a further caution against making too much of that small sequential rise, it's worth noting that another reliable industry source actually reported a reduction in the global hedge book for the second quarter of 2011. Metals consultancy VM Group, in coordination with ABN AMRO Bank, in August issued this report [opens PDF], which logged a 900,000-ounce contraction of the hedge book to reach 4.2 million ounces. The following chart from that report places the latest data within its proper context, and visually refutes any notion that miners are reversing their collective stance toward strategic gold hedges.

Source: VM Group; ABN AMRO Gold Hedging Report, August 2011.

What these gold hedges really reflect

Even if we were to adopt the GFMS data, including their forecast that the hedge book may expand by 1 million ounces during 2011, that still would not reflect a shift in sentiment toward forward gold prices. You see, the new gold hedges identified by GFMS during the second quarter were not born of a bearish outlook toward gold. To the contrary, bullish industry sentiment continues to fuel a race among junior miners to accelerate development timelines, and many are forced to rely upon bank debt to finance mine construction.

As a matter of course, banks routinely require miners to hedge a portion of forward production as a condition of debt issuance. According to George Gero, senior vice president for RBC Capital Markets Global Futures, "Junior miners have to hedge because they have to show the bank they have this much in production and this much in future sales, or they don't get the financing." Examining the two principal new hedges detailed by GFMS in its report, we find that both arrangements by a pair of Australian junior miners were indeed linked to debt facilities for financing mine construction.

As we have established above, the increase in the global hedge book reported by GFMS is truly miniscule in relative scale, and is furthermore contradicted by another professional assessment that reported a decline in net gold hedges nearly five times as large. What's more, because these new hedges are a precondition for access to needed development capital -- and not a product of strategic speculation of forward gold prices -- it is incorrect and improper to suggest that these hedges reflect any shift whatsoever in the outlook of gold mining executives toward the ongoing bull market.

GFMS itself made that point abundantly clear, but even that did not prevent a barrage of potentially misleading discussion from crossing the financial newswires. With this rebuttal, I hope to have corrected their collective error, and interrupted the process by which ill-informed analysis can transform into prevalent and unfortunate myths.

What the miners really expect

Now that we have established what is not true about miners' outlooks toward gold prices, let's review what we do know. We know that Newmont Mining (NYS: NEM) CEO Richard O'Brien believes gold will reach $2,300 per ounce next year. Kinross Gold (NYS: KGC) CEO Tye Burt believes that conditions for gold have "never been better," and adds: "Not only is it a safe haven for investors and offers a unique alternative to currencies, but the fundamentals of supply and demand are extremely strong." Barrick Gold CEO Aaron Regent recently stated: "Directionally, the factors that have basically caused the gold price to perform the way it has are still in place. If anything, they're intensifying."

I share their bullish outlook on gold, and anticipate powerful upside momentum for many quality gold producers over the coming years. I've identified a number of exciting prospects within the industry for my regular readers, and I invite you to keep track of my ongoing analysis by bookmarking my list of recent articles here. To get started, find out why I believe Primero Mining (NYS: PPP) is the greatest gold stock in the world.

Add Yamana Gold to My Watchlist.

Add Paramount Gold & Silver to My Watchlist.

Add Barrick Gold to My Watchlist.

Add Newmont Mining to My Watchlist.

Add Primero Mining to My Watchlist.

At the time thisarticle was published Fool contributorChristopher Barkercan be foundblogging activelyand acting Foolishly within the CAPS community under the usernameTMFSinchiruna. Hetweets. He owns shares of Paramount Gold & Silver, Primero Mining, and Yamana Gold. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool'sdisclosure policyis immune to the myriad myths about gold.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.