Accelerating Your Returns

"Any believable prediction will be wrong. Any correct prediction will be unbelievable. "

-- Kevin Kelly

In 1975, Intel's (NAS: INTC) founder and first chairman, Gordon Moore, proposed that computer chips would double their capabilities every two years. What he didn't realize was that these exponential improvements would also apply to nearly every technology we use today. In high-tech industries that sometimes seem to move at the speed of light, making sense of technology's accelerating pace can help you become a more intelligent investor.

Moore's Law writ large

Moore's Law implies exponential improvement. Within 30 generations, a chip that started with two transistors winds up with more than a billion. We can apply this to any automated process -- and the efficiency of its energy use -- because many technologies improve at similarly exponential rates. When one technology stagnates (and technologies inevitably do), it's quickly overtaken by newer ones still experiencing explosive growth. All together, this idea of technological progress is called the Law of Accelerating Returns.

Ray Kurzweil, who popularized this concept, says: "Today, we anticipate continuous technological progress and the social repercussions that follow. But the future will be far more surprising than most people realize, because ... the rate of change itself is accelerating." (Emphasis added.)

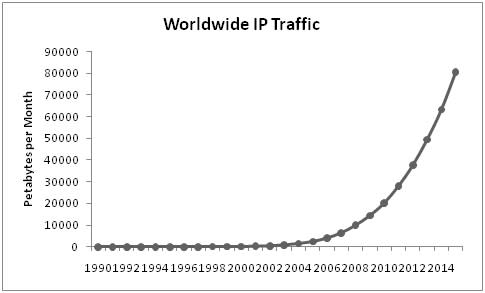

Transformative changes

You can visualize accelerating returns by looking at how technology has improved over many years. You can also find accelerating returns in the adoption and usage rates of decentralized innovations like the Internet. The growth of Internet traffic has kept an accelerating pace since its inception:

Source: Cisco Visual Networking Index.

Exponential growth would never have been possible if necessary technology (like Cisco's (NAS: CSCO) routers, switches, and other bandwidth-boosting devices) weren't installed at increasing rates. Greater bandwidth demands put more pressure on Cisco to create better technology, which was then deployed in ever greater numbers. This momentum drove Cisco's revenue from $2.3 billion in 1995 to nearly $25 billion in 2005. The company took in $40 billion in 2010 and could easily reach $50 billion by 2015.

Moore's Law was given a terminal limit, but this limit has been pushed back several times over the years by the development of better (and smaller) manufacturing technologies. It would be catastrophic for Intel, and for the rest of the vast high-tech industry, if this limit were ever reached with no superior technology set to replace it. Quantum computing is one futuristic possibility, and research has made real progress toward a quantum reality after silicon chips go the way of ENIAC.

Hardware, software, wetware

Technology suffers from massive deflationary pressures as a result of accelerating returns. An iPhone 4 is 1 million times faster than ENIAC yet costs 60,000 times less. Cost pressures forced IBM (NYS: IBM) out of its computer business and toward higher-margin consulting services. Apple (NAS: AAPL) has resisted deflationary pressure by offering a superior user experience, but the iPhone wouldn't be appealing to consumers if its components were years behind other smartphones.

Western Digital (NYS: WDC) and Seagate (NAS: STX) now control 90% of the hard disk drive industry, which once fielded more than 200 companies. Despite that consolidation, most hard drives will soon have 1 million times more capacity than they did in 1985. Technology-cost deflation is great for the end user, but it's good for manufacturers only if they can better take advantage of efficiencies of scale.

Software and services companies are influenced in different ways by accelerating returns, but their business models still ride on top of improvements to their supported technologies. Dropping technology costs are typically (though not always) much better for these companies than for manufacturers. A visionary leader -- like Intel's Moore, Apples Steve Jobs, or Microsoft's (NAS: MSFT) Bill Gates -- is invaluable in high-tech, charting a bold long-term path through uncertain possibilities. Gates announced the first Windows operating system when there were only 10 million computers in use in the United States. There have been more than 270 million computers sold this year alone, and Microsoft's operating systems are installed on at least 85% of those.

Knowledge is power

What can we do to make use of the assumptions of accelerating returns? When preparing to invest in a high-tech company, you should ask yourself these questions:

How does the company harness accelerating returns to manufacture better technology or provide superior service?

If the company provides services, is it deploying them in ways that keep pace with accelerating progress?

If the company manufactures technology, is there a point where it might stop undergoing accelerating returns?

How might falling technology costs affect the company's business? What strategies could the company use to take advantage of this issue?

Is the company working on new technologies or business models to deal with the possibility that accelerating returns will slow or stop in its core business?

Could the company lose its position because of accelerating returns in competing technologies? Does the company have a plan for this competition?

Is the company's investment in R&D stable or increasing as a percentage of total revenue?

These questions are only a starting point from which to dig deeper. Approach high-tech investing with the Law of Accelerating Returns as one of several guides to the future of your favorite companies. You won't always be right -- no one ever is -- but you should gain a clearer understanding of your chosen companies if you look at the long-term potential of the technologies that make their business possible.

Many companies take advantage of the Law of Accelerating Returns, but all businesses aren't created equal. That's why we've found one high-tech company that could make investors rich by harnessing the power of data analytics. The need for more (and better) data is increasing exponentially around the world, and you can find out how to profit in our free report!

At the time thisarticle was published Fool contributorAlex Planesholds no financial stake in any company mentioned here. Follow him onGoogle+-- he promises not to link any lolcats. The Motley Fool owns shares of IBM, Intel, Cisco Systems, Western Digital, and Apple, has created a bull call spread position on Cisco Systems, and has bought calls on Intel.Motley Fool newsletter serviceshave recommended buying shares of Intel, Cisco Systems, and Apple, creating a diagonal call position in Intel, and creating bull call spread positions in Apple and Microsoft. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.