Buy Corning's Share Buyback

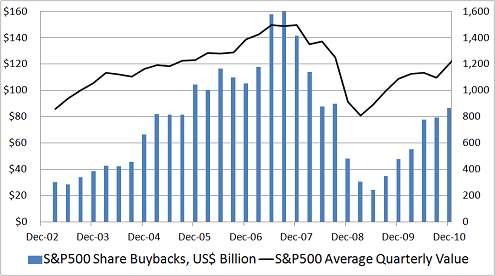

I'm highly skeptical about the economic value of most share-repurchase programs. To see why, look at the graph of the total buyback dollar amount for the companies in the S&P 500, compared with the average price of the index on a quarterly basis.

Source: Standard & Poor's.

Share buybacks for the S&P 500 accelerated in the second half of 2004, culminating in a sharp spike during the first two quarters of 2007 -- just as the stock market was peaking. Conversely, when stocks traded at bargain prices during the worst of the crisis, share buybacks dried up. Then, as stocks became more expensive during the rally that began in March 2009, companies once more became happy to step up the dollar amounts spent on share repurchases.

Still, not all buyback programs hurt shareholders. To praise smart capital allocators and shame those who fritter away shareholder capital, I've begun to track individual share-repurchase programs. Today, I'm looking at the new program established by specialty glass products manufacturer Corning (NYS: GLW) .

How much, for how long?

Corning is initiating a $1.5 billion share-repurchase program that expires at the end of 2013. There are no other restrictions on when the company will buy shares, or in what amounts.

Does this buyback add up?

Corning's announcement is the model for an intelligent, shareholder-oriented buyback. As Wendell Weeks, chairman, CEO, and president of the company, explains:

The board's decision to repurchase shares reflects our belief that the long-term value of our businesses is substantially greater than our current share price. ... The board's actions are consistent with the company's financial priorities that we outlined for investors in 2006. The first priority is always to protect the corporation. The second priority is to invest in our growth opportunities, internally and externally, to deliver shareholder value. The third priority is to return money to shareholders either as dividends or through share repurchases, to enhance shareholder returns.

That statement is perfectly consistent with the share-repurchase guidelines Warren Buffett outlined in Berkshire Hathaway's (NYS: BRK.B) 1999 shareholder letter:

There is only one combination of facts that makes it advisable for a company to repurchase its shares: First, the company has available funds -- cash plus sensible borrowing capacity -- beyond the near-term needs of the business and, second, [it] finds its stock selling in the market below its intrinsic value, conservatively calculated.... The business "needs" that I speak of are of two kinds: first, expenditures that a company must make to maintain its competitive position (e.g., the remodeling of stores at Helzberg's) and, second, optional outlays, aimed at business growth, that management expects will produce more than a dollar of value for each dollar spent (R.C. Willey's expansion into Idaho).

How cheap is the stock?

Corning management clearly understands that the relationship between price paid and intrinsic value determines whether share repurchases are compounding or destroying shareholder wealth. Just how cheap (or expensive) are the shares right now? Based on its price-to-earnings multiple, Corning trades in the bottom half of a group of its competitors:

Company | Forward P/E |

|---|---|

Becton, Dickinson (NYS: BDX) | 12.1 |

3M (NYS: MMM) | 11.5 |

Corning | 7.6 |

Alcatel-Lucent (NYS: ALU) | 7.6 |

Source: S&P Capital IQ.

You should be following Corning (and its peers)

Corning's price-to-earnings multiple is in the bottom half of the range relative to the company's industry peers and in the bottom quintile compared with the companies in the S&P 500 and to its own five-year history. With shares changing hands at 7.6 times next 12 months' estimated earnings, the buyback program looks like a good use of shareholder capital at current prices; in fact, the entire group of stocks in the table looks attractive right now. You can start to track them with our free application, My Watchlist.

Add 3M to My Watchlist.

Add Corning to My Watchlist.

Add Becton to My Watchlist.

Add Alcatel-Lucent to My Watchlist.

Add all of these companies to My Watchlist.

At the time thisarticle was published Fool contributorAlex Dumortierholds no position in any company mentioned. Check out hisholdings and a short bio. You can follow himon Twitter. The Motley Fool owns shares of Berkshire Hathaway.Motley Fool newsletter serviceshave recommended buying shares of Corning, Becton, Berkshire Hathaway, and 3M. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.