This Stock Is Guaranteed to Bring Joy to Your Portfolio

Click here to follow Jason on Twitter.

The headlines today all read that commodities are in a crunch. Copper is getting killed, oil is as low as it's been in more than a year, and with threats of global recession, what are we going to do? I tell you what I'm gonna do: I'm adding Joy Global (NAS: JOYG) to my Rising Star portfolio.

The company

Joy Global was technically founded in 1884 as Harnischfeger Industries. However, when Harnischfeger filed for bankruptcy in 1999, Joy Global emerged as the direct successor company with a global focus on underground mining and surface mining equipment. Today the company operates in two segments: P&H Mining Equipment (surface mining equipment) and Joy Mining Machinery (underground mining machinery).

P&H is the world's largest producer of electric mining shovels, and Joy Mining is the world's largest producer of underground mining machinery for the extraction of coal and other materials. While the company's products are used for mining a number of materials, more than two-thirds of revenues come from their coal-mining customers. Given that more than 40% of total revenue comes from outside the U.S. and Europe, I smell an opportunity of global proportions.

Oh the Joy!

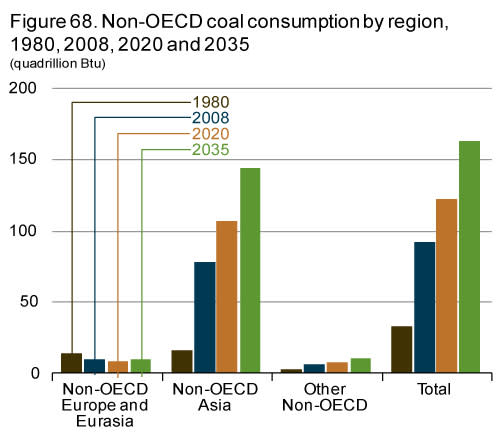

The International Energy Outlook 2011 predicts that through 2035, coal consumption for Organization for Economic Co-operation and Development nations will remain essentially flat. However, non-OECD nations (like China and India) are another story; projections there are for coal consumption growth of 76%. Furthermore, from 2008 to 2035, coal is projected to account for more than one-third of total non-OECD energy consumption. Below is a graph charting estimates for non-OECD consumption by region:

India and China both continue to import more thermal and metallurgical coal as well thanks to continued development and significant infrastructure programs in both countries' next five-year plans.

Joy's recent acquisition of LeTourneau from Rowan Cos. (NYS: RDC) along with additional market share gains from the strategic investment in International Mining Machinery Holdings in China should also add some fuel to the fire.

Just as emerging economies are stoking demand for coal, copper is another commodity that plays a big part in energy and infrastructure upgrades. While copper plays a smaller role in Joy's overall revenue (to the tune of about 15% annually) management believes it will continue to see double-digit growth in the near term as mining companies are realizing strong demand and prices. The table below represents the capital expenditure trends for three global mining operations over the past three years. It is also worth noting that all three have guided for increased capital expenditure spending going forward as well:

Freeport-McMoRan (NYS: FCX) | $1,917.0 | $1,412.0 | $1,587.0 |

BHP Billiton (NYS: BHP) | $12,387.0 | $10,656.0 | $10,735.0 |

Rio Tinto (NYS: RIO) | $7,908.0 | $4,591.0 | $5,388.0 |

Why there would be no joy in Foolville

It's plain to see that there are plenty of risks inherent with investing in a company like Joy Global and there a few things we'll need to keep our eyes on:

What recovery?: As the global economy continues to teeter on the edge of recession, the rest of the world remains inextricably tied to the fate of countries such as Greece, Spain, and Italy. While I like Joy's exposure to non-OECD countries, the tangential effects of any kind of meltdown will play out in the commodities market and more than likely crimp Joy's backlog for the short term.

More specifically: One of Joy's strengths could also be a weakness if global demand for coal fails to materialize. Any significant drop in demand or uptick in environmental issues could leave a black mark that may be tough to get rid of.

Big dog (or Cat): Joy has a tremendous global reach and a balance sheet that affords some genuine opportunities like the LeTourneau and IMM deals. However, Caterpillar (NYS: CAT) is a major player in this area as well, and given the size advantage it could pose some pricing problems for Joy down the road.

Diamonds in disguise?

Joy has grown top-line revenue at 12% annually over the past decade, and as it continues to leverage costs, operating margins should continue to average above 20%. Granted the business is susceptible to overall global conditions, but I think the long-term picture is still attractive and if it is able to grow the top line at around 7% or so over the next decade we're looking at a stock that is worth closer to $80 than the $58 it trades for today. The market is pricing in a pretty dismal scenario, and that may be fair for the short term. As a long-term holding though I think we're getting a real winner (and a market-spanker over the last five years) at an excellent price, and I'm willing to wait out the storm.

My Foolish bottom line

This market has everybody spooked and there's no telling what's around the corner. What's the next shoe to drop? True to my Foolish ways, I gotta keep investing in good times and in bad. And while Joy Global may very well fall further in the volatility that is the market these days, I've deemed it worthy of a 6% ($1,000) position in my portfolio today. Make sure to drop on by my discussion board and let me know what you think.

At the time thisarticle was published Stock Advisor analyst Jason Moser owns no shares of companies mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.