Gold's Duck Test

Investors love to debate whether the current price of gold is indicative of an asset bubble. I believe the question can be resolved using good old-fashioned common sense. If it looks like a bubble, acts like a bubble, and quacks like a bubble, then it's probably a bubble. So does the recent and precipitous fall in its price settle the matter by proving the elusive bubble has burst? I think it may.

What exactly is a bubble?

Before delving into such a contentious subject, it's important we're on the same page about what exactly an asset bubble is. Quite simply, it's a surge in the price of an asset or asset class that is then followed by a rapid price deflation.

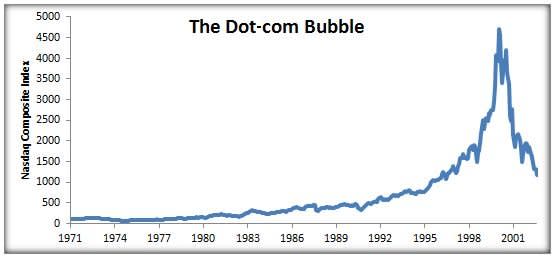

The surge and subsequent deflation of technology stocks in the 1990s provides a textbook example of this. The Nasdaq Composite Index began its dramatic assent in 1998 only to fall just as dramatically in 2000. And even after 10 years, a company as veritable as Microsoft has yet to see its share price reclaim its high at the time.

Source: Yahoo! Finance.

Not long after the dot-com bubble burst, moreover, a housing bubble began to form, only to then burst in 2008, creating the increasingly identifiable bubble shape that a graph reveals.

Source: Standard & Poor's, Case-Shiller Home Price Indices.

A bubble's characteristics

There are two particularly notable characteristics of an asset bubble. The first is that it's fueled by the way in which market participants allocate resources. Investors right now, for example, are fleeing stocks in favor of things like U.S. Treasury bonds. This trend has decreased the price of the S&P 500 while increasing the price of Treasuries, symbolized by historically low government-bond yields.

The second is that these allocation decisions don't reflect the fundamentals of supply and demand. For example, while the world's consumption of oil has risen steadily from 60 million to 85 million barrels a day over the past 30 years, its price started surging in 2001 only to dramatically deflate seven years later, evidencing a complete detachment from economic reality. And although the chart doesn't depict it, the price has since rocketed back up to $116 a barrel in April of this year only to settle back down to $82 per barrel today.

Source: Indexmundi.com.

So is gold a bubble?

The question of whether gold is following a similar track is hotly debated, even amongst investors here at the Fool. And like many debates, both sides skillfully marshal statistics to support their positions.

Those opposed to the notion that gold prices indicate a bubble rely largely on the "dollar decline theory." This theory, favored by the CEO of Barrick Gold (NYS: ABX) , holds that the price of gold has steadily tracked the amount of money in circulation over the past decade. Its price has only gone up, in turn, because the value of the dollar has gone down.

My colleague Christopher Barker recently advanced another popular theory for current gold prices favored by hedge-fund manager Eric Sprott of Sprott Physical Gold Trust. The idea here is that the portion of the world's wealth that is held in gold today is markedly lower than at any time over the past 100 years. As a result, it purportedly follows that there couldn't be a bubble because investors are allocating away from gold, as opposed to toward it.

On the other side of the argument are Fools like Morgan Housel and Matt Koppenheffer. In a recent column, for example, Morgan refuted the dollar-decline theory by noting that it focuses on the wrong measure of money in circulation and that when the right measure is used, it actually supports the notion of a gold bubble. And in a similarly provocative column, Matt demonstrated that the increase in the price of gold has markedly outpaced the increase in the price of other commodities, including cotton, pork, milk, and coffee.

If it quacks like a bubble

I respect all of these opinions, but I believe the question can be resolved using good old-fashioned common sense. If it looks like a bubble, acts like a bubble, and quacks like a bubble, then it's probably a bubble.

Source: Indexmundi.com.

Of course, this doesn't mean you should immediately sell your stock in companies such as Yamana Gold (NYS: AUY) or Christopher Barker's top gold pick for 2011, AuRico Gold (NYS: AUQ) , which he picked the year after his wild success with Silver Wheaton (NYS: SLW) .

What it does mean, however, is that you need to start balancing your portfolio with stable, well-diversified companies such as Procter & Gamble (NYS: PG) and Johnson & Johnson (NYS: JNJ) in preparation for the fall. One place to start is a free report by our top equity analysts that profiles five companies they hand-selected for our own portfolio here at The Motley Fool. Grab this report while it's free and still available.

At the time thisarticle was published Fool contributor John Maxfield has no financial position in any of the securities mentioned here. The Motley Fool owns shares of Microsoft and Johnson & Johnson.Motley Fool newsletter serviceshave recommended buying shares of Johnson & Johnson, Procter & Gamble, and Microsoft, creating a bull call spread position in Microsoft, and creating a diagonal call position in Johnson & Johnson. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.