The Big Pay Raise You Didn't Know About

"Real Wages Haven't Grown for Over a Decade."

Some version of that headline has found its way to the top of thousands of articles over the past several months.

It's mostly true, particularly among certain groups. The average male earned a wage of $32,817 in 1990, and $32,137 in 2010, adjusted for inflation. He's gone slightly backward over the past 20 years. Some worry about the prospects of a lost decade. Plenty of Americans have already experienced a couple. Sad days, these.

But like so much else in the economy, the story is more complicated than it looks. Most people have actually been given a raise in recent decades. They just aren't looking in the right place.

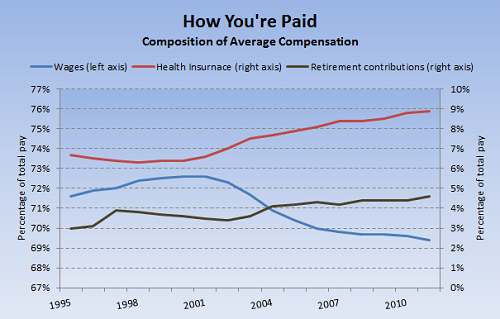

The Bureau of Labor Statistics keeps detailed historic records on not just the amount an average American is paid, but how they're paid. There are several different ways an employer can compensate a worker. The main one is with a paycheck. But there's also health insurance, paid time off, retirement contributions, and other fringe benefits. Drilling down on those last few is key to understanding why average wages have flatlined for at least two decades.

Interestingly, the total amount employers pay an average worker has gone up by more than 13% in inflation-adjusted terms over the past decade. That's an important point that rarely gets discussed -- average Americans are making more money today than they did 10 years ago.

What's changed is the composition of that pay. Wages have become a smaller part of the total compensation pot, while benefits -- particularly health insurance and retirement contributions -- have become more important:

Sources: Bureau of Labor Statistics.

Another way to look at it: Wages made up about 73% of total compensation in 2000. Today, it's 69.4%. Ten years ago, insurance made up 6.4% of total compensation. Today, it's nearly 9%. In 1995, employer-provided retirement contributions made up an average of 3% of compensation. Today, it's 4.6%.

Those may not seem like big changes, but they make a dent over time. If insurance and retirement contributions as a percentage of total compensation were the same today as they were in 2000, the average household's paycheck would be about $2,000 a year greater. You'd notice that.

This stuff is important for two reasons. One, it highlights how out of control health insurance growth has become. Health insurance premiums more than doubled over the past decade, growing more than twice as fast as the broader economy. Reforms waiting to be implemented as part of last year's health care act could slow that growth by about 1.5% annually. That's a good start, but not nearly enough. Growth in the cost of health insurance premiums would have to fall by roughly twice as much just to stay at a steady percentage of income. Until that happens, more of your work day is going to go toward health insurance, less toward a paycheck. Tough way to make a living.

Second, the disconnect between feeling like your pay hasn't gone up while total compensation has risen is a good example of what psychologists call "availability heuristic." This is the idea that people react to what they vividly remember, not the whole picture. In this case, people are vividly aware that their paychecks haven't gone anywhere in decades. They cash those checks every month. They see the numbers. It's tangible. Fringe benefits like employer-provided health insurance premiums are another story. They're out of sight, out of mind. Even though these benefits cost employers a lot of money, the employees they cover are often oblivious to the costs. This is particularly true at companies such as Microsoft (NAS: MSFT) , Whole Foods (NAS: WFM) , Rackspace (NYS: RAX) , and Qualcomm (NAS: QCOM) , where employees don't chip in a dime for health insurance premiums. Whether they realize it or not, these folks (and most Americans) are getting a big raise through employer-provided coverage of health insurance premiums that become relentlessly more expensive every year. Alas, many likely don't realize it. They focus on stagnant wages, and assume their pay is going nowhere. And the higher those health insurance premiums go, the less likely they are to get wage raises. It's a vicious cycle of ignorance.

I didn't think about this stuff until a small-business owner told me that he cut wages in order to afford burgeoning health insurance premiums for his employees. Those employees actually received a net raise, but they hardly knew it. In fact, they were furious. Easy solution: The owner offered drastically reduced health benefits in exchange for higher wages. Total compensation stayed the same, but employees were happier. They had a better understanding of how much they really earned.

Is more of this needed? I think so. Things work better when everyone knows what's going on. Right now, too many workers are blinded into believing compensation is flat and unaware of how intense the rise in health insurance premiums has become. Anything that shines more light on reality is a step in the right direction.

Check back every Tuesday and Friday for Morgan Housel's columns on finance and economics.

At the time thisarticle was published Fool contributor Morgan Housel owns shares of Microsoft. Follow him on Twitter @TMFHousel. The Motley Fool owns shares of Qualcomm, Microsoft, and Whole Foods Market. Motley Fool newsletter services have recommended buying shares of Rackspace Hosting, Microsoft, and Whole Foods Market. Motley Fool newsletter services have recommended creating a bull call spread position in Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.