Don't Tune Out Netflix Yet

You're probably wondering whether Netflix (NAS: NFLX) has a future or if you should just write it off right now. It's been a stomach-turning descent, taking investors into the red for the year. Buy-and-hold investors can live through a precipitous drop as long as they believe the company can succeed on a longer timeline, but it looks like a lot fewer people believe in Netflix's long-term prospects now. I don't think you can count the company out just yet. If it can keep growing, this might turn out to be one of the most attractive times for prospective buyers in years.

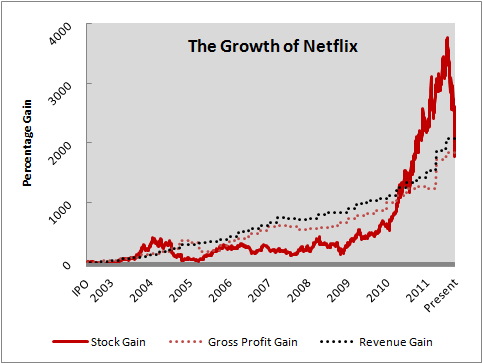

Growth, growth, growth

Everyone's familiar with the growth of the company's stock price, but how many people have taken the time to look at other kinds of growth? For a long time, Netflix's growth in revenue and gross profit actually surpassed the rise of its stock price:

Source: Yahoo! Finance and SEC filings.

The stock price went parabolic at the start of 2010, leaving the steadily impressive rise in Netflix's financial health in the dust. You could call it the Netflix bubble. The pinprick that let all the air out was a rate increase, and it just got worse and worse after that. Its guidance disappointed. It lost Starz (NAS: LSTZA) . It lost a million subscribers. It's splitting the services. On and on.

Fly the red and white flag of war

But here's the thing. Will Netflix stop growing? By all accounts it's bleeding subscribers, having cut third-quarter expectations to 24 million after finishing the second quarter with 25.6 million subscribers. That's a lot of subscribers, even if it is only 6.7% of its total. If you believe the company's guidance, it might even make more from less -- assuming it's right, Netflix could make over $40 million more in revenue per month based on current assumptions, and that would put its gross profit and revenue gains well above its current stock price gain.

But wait, there's more! A small-scale survey of 1,100 Netflix subscribers found that 22% planned to cancel their service and use Coinstar's (NAS: CSTR) Redbox or Amazon's (NAS: AMZN) competing streaming service. The same assumptions I used earlier, with 78% of 24 million subscribers, earn Netflix $43 million less per month than it earns under its current plans. That's slightly more quarterly revenue lost than the company gained from the first to the second quarter, but don't forget that it costs a lot less to stream movies than it does to ship them through the post office. Rate increases might hurt in the short term, but Netflix has plans for world domination. Smart expansion can pave over the potholes of this rough road.

Turn on, tune in, pay up

The biggest obstacle for any would-be entertainment king is content, content, content. Netflix's focus on streaming has gotten a lot of people wondering if Netflix is filling in its own moat, but it's still stocked with more content than any competitors. Amazon has far fewer titles in its streaming service. DISH Network (NAS: DISH) , for all the Blockbuster-based streaming rights it might own, still has far fewer potential titles available on fewer potential devices. Wal-Mart's (NYS: WMT) Vudu service offers the advantage of earlier availability, but there's no word on how many titles it actually offers. Want to watch Game of Thrones on Time Warner's (NYS: TWX) HBO Go streaming service? You can't even purchase it independently of your TV subscription.

The roof isn't on fire (yet)

Netflix has a host of problems, but it also has an enviable array of answers. There's a real risk of continued subscriber loss, but if the numbers add up, they've already priced it in. It's going to take a lot of work, and a lot of money, for any competitor to overcome its content depth. For now, Netflix is still the top dog in the yard. If (or when) the stock drops further, it'll be well under the company's growth pace, which should be attractive for anyone looking for a Rule Breaker at a discount.

Keep your eye on Netflix by adding it to your watchlist. It's not the only company cashing in on the broadband revolution, and The Motley Fool has the inside scoop on a little company that could ride the streaming wave to big gains. Find out more in our free report!

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. The Motley Fool owns shares of Wal-Mart Stores. Motley Fool newsletter services have recommended buying shares of Netflix, Wal-Mart Stores, and Amazon.com. Motley Fool newsletter services have recommended creating a bear put spread position in Netflix. Motley Fool newsletter services have recommended creating a diagonal call position in Wal-Mart Stores. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2011 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.